Peter Cook is the author of the Is That True? series of articles, which help explain the many statements and theories circulating in the mainstream financial media often presented as truths. The motives and psychology of market participants, which drives the difference between truth and partial-truth, are explored.

Most people are aware that GDP growth has been lower than expected in the aftermath of the Global Financial Crisis of 2008 (GFC). For example, real GDP growth for the past decade has been closer to 1.5% than the 3% experienced in the 50 years prior to 2008. As a result of the combination of slow economic growth and deficit spending, most people are also aware that the debt/GDP ratio has been rising.

However, what most people dont know is that, over the past ten years, the dollar amount of cumulative government deficit spending exceeded the dollar amount of GDP growth. Put another way, in the absence of deficit spending, GDP growth would have been less than zero for the past decade. Could that be true?

Lets begin with a shocking chart that confirms the statements above, and begins to answer the question. The black line shows the difference between quarterly GDP growth and the quarterly increase in Treasury debt outstanding (TDO). When the black line is above zero (red dotted line), the dollar amount is GDP is growing faster than the increase in TDO. From 1971 to 2008, the amount of GDP typically grew at a faster rate than the increase in TDO, which is why the black line is generally above the red dotted line.

Chart 1

During the 1971-2008 period, inflation, budget deficits, and trade deficits varied widely, meaning that the relationship between GDP growth and TDO was stable even in the face of changes in other economic variables. Regardless of those changing economic variables, the US economy tended to grow at a pace faster than TDO for four decades. The only interruptions to the pattern occurred during recessions of the early 1980s, early 1990s, and early 2000s when GDP fell while budget deficits did not.

The pattern of GDP growth exceeding TDO changed after 2008, which is why the black line is consistently below the red dotted line after 2008. A change in a previously-stable relationship is known as a regime change. Focusing first on 2008-2012, the increase in TDO far exceeded GDP growth, due to an unprecedented amount of deficit spending compared to historical norms. Focusing next on 2013-2017, the blue line has been closer to the red dotted line, meaning that the dollar amount of GDP growth was roughly equal to TDO.

If the pattern of the past was in effect, the black line should have been far above the red dotted line for most of the entire period of 2009-2017, because it would be expected that a recovering economy would have produced an excess of GDP growth over TDO. But that didnt happen. This article will not speculate on why there was a regime change. Instead, this article is focused strictly on identifying that a regime change occurred, and that few people recognize the importance of the regime change, which is probably why it persists.

Taking a quick detour into the simple math of GDP accounting, the level of GDP is calculated by adding up all forms of spending:

GDP = C + I + G + X

In the equation above, C is consumer spending; I is investment spending by corporations; G is government spending; and X is net exports (because the US has become such a heavy net importer, X has been a subtraction from GDP since 2000).

For context, at the end of 2017, the level of US GDP was $19.74 trillion, per the Bureau of Economic Analysis (BEA). Of that $19.74 trillion, the Congressional Budget Office (CBO) calculated that the US government spent $3.98 trillion, all of which counts toward GDP. In 2017 the government borrowed $516 billion, meaning that the government spent more than it received via taxes and other sources. The main insight in understanding how the government calculates GDP is that all government spending counts as a positive for GDP, regardless of whether that spending is financed by tax collections or issuing debt.

Because deficit spending is additive in the calculation of GDP, it makes sense to compare the amount of deficit spending to the amount of GDP growth produced each year. The first four columns in the table below show the annual GDP, the annual dollar change of GDP, the total amount of Treasury debt outstanding (TDO) and the annual dollar change of TDO. Comparing the second and fourth columns, it is easy to see that the annual increases in TDO regularly exceed the increases in GDP.

Chart 2

The final column to the right shows the increase in TDO as a percentage of the annual change in GDP growth. When the ratio is greater than 100%, the increase in TDO is responsible for more than 100% of annual GDP growth. Reinforcing the message of Chart 1, the annual increase in TDO exceeded annual GDP growth in each of the years from 2008-2016. The only year in which annual GDP growth was greater than the increase in TDO was in 2017, possibly due to the debt ceiling caps, which have now been lifted.

The cumulative figures are even more disturbing. From 2008-2017, GDP grew by $5.051 trillion, from $14.55 trillion to $19.74 trillion. During that same period, the increase in TDO totaled $11.26 trillion. In other words, for each dollar of deficit spending, the economy grew by less than 50 cents. Or, put another way, had the federal government not borrowed and spent the $11.263 trillion, GDP today would be significantly smaller than it is.

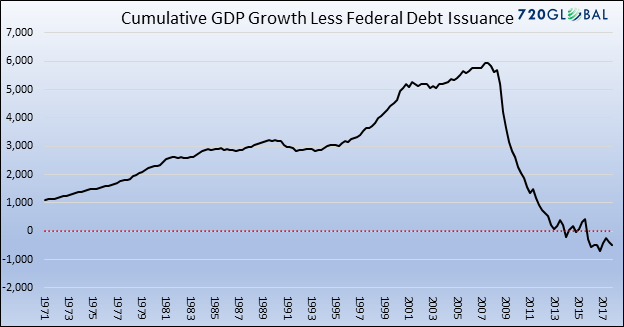

It is possible to transform Chart 1, which shows annual changes in TDO and GDP from 1970-2017, into Chart 3 below, which shows the cumulative difference between the growth of TDO and GDP over the entire period from 1970-2017. The graph below clearly shows the abrupt regime change that occurred in the aftermath of the GFC. A period in which growth in GDP growth exceeded increases in TDO has been replaced by a period in which increases in TDO exceeded GDP growth.

Chart 3

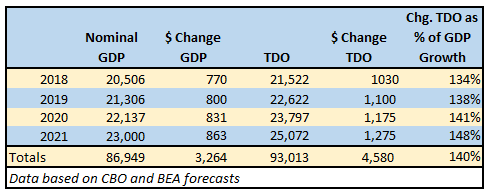

Unfortunately, extending the analysis forward tells us the problem will only get worse.

Chart 4

Over the entire period from 2008 to 2021, the increase in TDO will exceed GDP growth by $7.531 trillion ($15.843 trillion of TDO compared to $8.312 trillion of GDP growth). While most people would accept that deficit spending is required for short periods to offset economic disturbances, even John Maynard Keynes wouldnt expect it to become the norm. Nor would he expect that a dollar of deficit spending would produce less than a dollar of GDP growth.

Investment and Policy Implications

The purpose of this article is to clarify the changing relationship between the dollar amounts of GDP growth and budget deficits, which are funded by TDO. If indeed GDP growth has become reliant on budget deficits post-2008, there are many implications for investment policies across all asset classes. For example, might poor organic growth in the private sector explain the unexpectedly-low inflation environment and historically-low capital investment? If so, what are the implications for stocks and bonds?

Also, government policy should acknowledge the regime change and adapt policies accordingly. If massive deficit spending is required to produce a positive sign for GDP growth, is it possible that the private sector of the economy is not growing but shrinking? Is the private sectors health now completely reliant on continued government deficits? If so, is there a limit to the governments ability to run deficits by issuing bonds? If a dollar of increase in debt leads to less than a dollar of GDP growth, should the US continue to borrow? Should the Fed raise rates because of increased fiscal stimulus if the link between deficit spending, GDP growth, and inflation has experienced a regime change? Can any economic theory explain what is going on?

These questions will be addressed in upcoming articles.

Conclusions

- All government spending boosts GDP calculations, regardless of whether government spending is financed by tax collections or deficits financed by debt issuance.

- Isolating the interaction between increases in TDO and the dollar amount of GDP growth, the data show a regime change post-2008 compared to the period 1971-2007.

- In the period 1971-2007, the dollar amount of GDP growth exceeded increases in TDO except in years in which the economy was in recession.

- In the period 2008-2017, annual increases in TDO regularly exceeded the dollar amount of GDP growth, which remarkably occurred during years that GDP was calculated to be growing.

- In the period 2008-2017, the cumulative increase in TDO was a multiple of cumulative GDP growth. The dollar amount of GDP growth was completely dependent on deficit spending.

- The efficiency of each dollar of deficit spending is declining, because the dollar amount of TDO is greater than the dollar amount of GDP growth.

- In the period 2018-2021, the increase in TDO will continue to exceed GDP growth, per forecasts made by the BEA and CBO. That is, GDP growth will be dependent on continued deficit spending.

- Importantly, if the economy slips into recession, it is possible TDO will grow at well over $2 trillion per year, meaning that the gap between TDO and GDP will get much larger.

{kind=link}

{kind=link}

{kind=link}

{kind=link}