Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

-- Published: Monday, 9 April 2018 | Print | Disqus

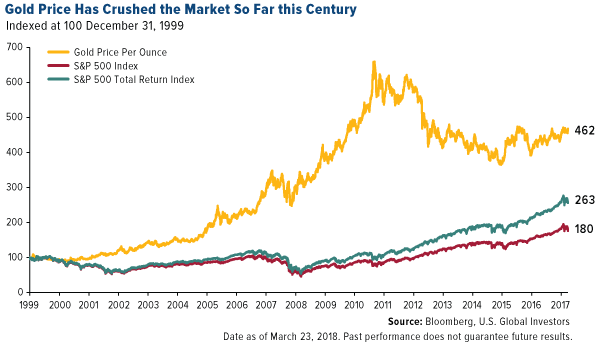

Gold outperforming stocks in 2018 and this century (see chart) Gold up close to 2% in 2018 while S&P 500 is down 2% Trump trade wars and Kudlow as Trump chief economic advisor is gold bullish Given golds performance, Kudlows dismissal of gold as end of the world insurance is irrational Market volatility could drive gold to $1,500/oz in 2018 Holmes

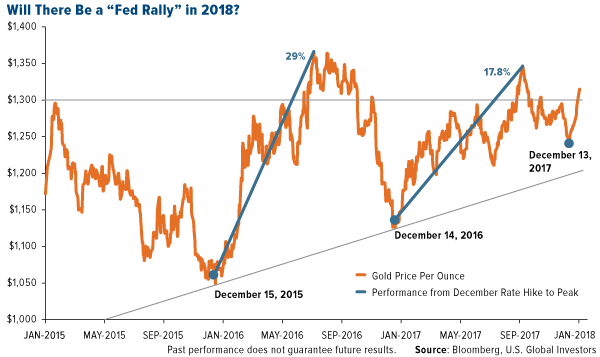

In a January post, I showed how the price of gold rallied in the months following the 2015 and 2016 December interest rate hikesas much as 29 percent in the former cycle, 17.8 percent in the latter. Gold ended 2017 up double digits, despite pressure from skyrocketing stocks and massive cryptocurrency speculation.

I forecast then that we could see another Fed rally this year following the rate hike in December 2017. Hypothetically, if gold took a similar trajectory as the past two cycles, its price could climb as high as $1,500 this year.

As I told Kitco News Daniela Cambone last week, I stand by the $1,500 forecast. Before last week, investors might have been slightly disappointed by golds mostly sideways performance so far this year. But now, in response to a number of factors, its up close to 3 percent in 2018, compared to the S&P 500 Index, down 2.4 percent.

Living with Volatility

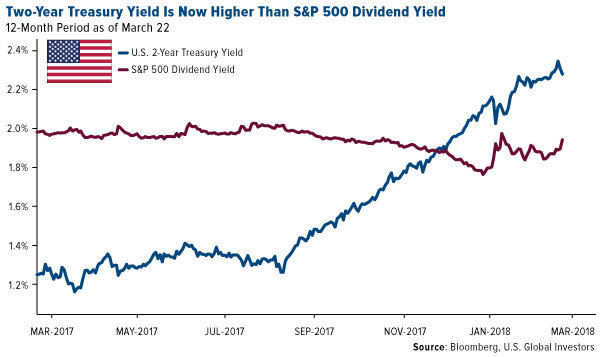

While Im on the topic of equities, the S&P 500 dividend yield, for the first time in nearly a decade, is now below the yield on the two-year Treasury. Historically, the economy has slowed around six months after dividends stopped paying as much as short-dated government paper.

This could spur some stock investors to trim their exposure and rotate into other asset classes, including not just bonds but also precious metals, which I believe might help gold revisit resistance from its 2016 high of $1,374 an ounce.

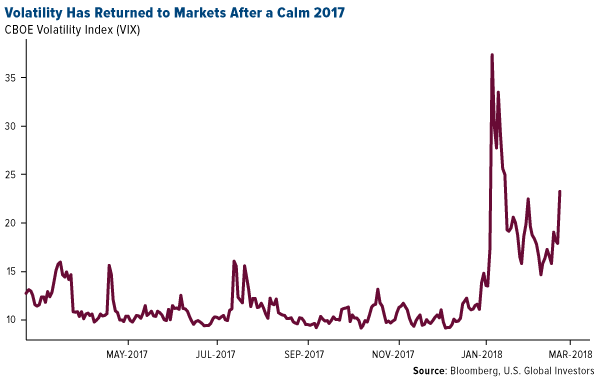

Volatility has also crept back into markets. It began with the positive wage growth report in February, implying the possibility of faster inflation. More recently, the CBOE Volatility Index (VIX), or fear gauge, has surged on the departures of Gary Cohn as chief economic advisor and Rex Tillerson as secretary of state, as well as the application of tariffs on steel and aluminum imports.

Last week, President Donald Trump ordered tariffs on at least $50 billion of Chinese goods, stoking new fears of a U.S.-China trade war. In response, the Asian giant proposed fresh duties on as much as $3 billion of U.S. products, including wine, fruits, nuts, ethanol and steel pipes.

As I see it, there could be other contributing factors pushing up the price of gold. A good place to start is with Trumps recent appointment of former CNBC star Larry Kudlow as White House chief economic advisor.

Kudlows Kerfuffle Over Gold

Between 2001 and 2007, I appeared on Kudlows various CNBC shows a number of times, and though he always struck me as highly intelligent, informed and accomplishedhe served as Bear Stearns chief economist and even advised President Ronald Reaganit was clear he had a strong bias against gold. This was the case even as the price of the yellow metal was on a tear, rising from $270 in 2001 to more than $830 an ounce by the end of 2007.

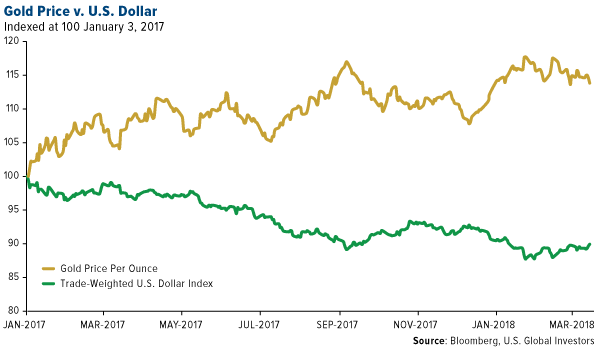

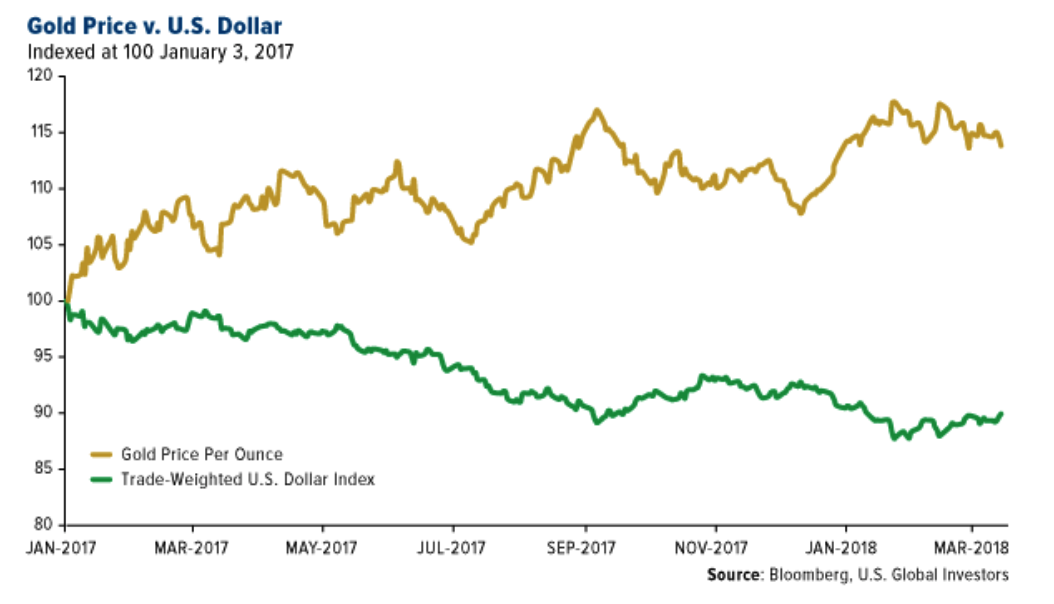

Kudlow showed his true colors toward gold as recently as this month, telling viewers: I would buy King Dollar and I would sell gold. As you can see below, this hast been a prudent trade for more than a year now.

Earlier this month, Kudlow wrote that falling gold is good, as it bodes well for the future economy. He said he agreed with a friend, who called the metal an end-of-the-world insurance contract.

While there are those who would agree with him, its important to remember that gold is used for much more than as a portfolio diversifier, and its price is driven by a number of factors. These include Fear Trade factors, from inflation to negative real interest rates, and Love Trade factors such as gift-giving during cultural and religious festivals. The precious metal has important industrial applications as well.

And since I first went on Kudlows program, gold has outperformed the S&P 500s price action nearly two-to-one, as I showed you back in December. Even with dividends reinvested, the market is still trailing the yellow metal.

So its fine if gold isnt your favorite asset, but to dismiss it wholesale as Kudlow has again and again is, with all due respect, irrational.

Its Not About Steel, Its About Stealing

Kudlow isnt just anti-gold, however.

Hes also anti-China, and even though hes traditionally opposed tariffs in general, he supports Trumps efforts to levy taxes on Chinese imports. Specifically, the duties are designed to offset the cost of intellectual property allegedly stolen by the Chinese over the past several years.

Chinas J-31 fighter jet, for example, is believed to be a knockoff of Lockheed Martins F-35, the most expensive piece of U.S. military equipment. Its for this reason that Lockheeds CEO, Marillyn Hewson, was present when Trump signed the authorization to impose new tariffs.

Our intellectual property is hugely important to the U.S. economy. As important as steel and aluminum are, they account for only 2 percent of world trade, and in the U.S., its even less than a percent of gross domestic product (GDP). Technology exports, on the other hand, represent about 17 percent of U.S. GDP.

That said, the implications of a trade war with the worlds second-largest economy certainly have many investors concernedall the more reason to consider adding to your gold allocation at this time. As always, I recommend a 10 percent weighting, with 5 percent in gold bullion, 5 percent in high-quality gold mining stocks and ETFs.

Is Trump Betting on the Wrong Guy?

On a final note, we were pleased to have an old friend visit our office last week. Michael Ding, a veteran of the U.S. Global investments team, joined us to share some laughs and his thoughts on whats happening in Asian markets right now.

Specifically, Michael said that Ray Dalio, founder of mammoth investment firm Bridgewater Associates, which manages around $160 billion, has become something of an economic guru for members of the Chinese ruling partys highest-ranking members, including Premier Li Keqiang.

Daliowhose most recent book, Principles, nowtops Chinas bestseller listis reportedly advising the countrys top bankers and economists on how to deleverage safely without triggering a so-called hard landing.

A trade war between the U.S. and China, Ray Dalio said recently, would be a tragedy.

So to put it in perspective: Whereas Trump has just now brought on Kudlow, the Chinese are leaning on a fellow American, Dalio, one of the smartest, most gifted money managers in the worldnot just of our time but of all time.

Did Trump make the right call? Which player would you want on your team: Kudlow or Dalio? For my money, I would pick Dalio.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.