The case for gold in the era of financial virtual reality

-- Published: Wednesday, 2 May 2018 | Print | Disqus

On the holodeck the markets are telling us something but we know not what

By Michael J. Kosares

"John Locke, the British philosopher whose ideas fuelled the American Revolution, had a theory of knowledge and perception, which I always found annoying. Asked if we have an idea of the substance behind our perceptions, he said we had 'no such clear idea at all, and therefore signify nothing by the word substance but only an uncertain supposition of we know not what'. The philosophical debate has moved on in the centuries since Locke wrote. But his idea captures well the uneasy state of the world's financial markets. They are driven in the short run by perceptions, not reality. If many have the wrong impression, markets will move on that. But in the long run, markets move on matters of substance. And at present the economic substance is a 'something we know not what.'" - John Authers, Financial Times

"Many Wall Street traders are concerned about being replaced by machines in the future, but at one Goldman Sachs Group Inc. unit its already happened. 'Equity trading: 15-20 years ago we had 500 people making markets in stocks. Today we have three,' Goldman Sachs President David Solomon said Monday at the Milken Institute Global Conference in Beverly Hills, California. Solomon said the introduction of more technology into the trading business has made it more efficient for clients, while also introducing new risks. For Goldman Sachs, it has changed the mix of its workforce, as the bank has 9,000 engineers on staff and more employees are focused on regulation." Sonali Basak and Christopher Palmeri, Bloomberg

Editor's note: So how has gold performed in this financial virtual reality? The short answer is surprising well. The seven charts below provide a picture of its performance over the past few years as computer-based systems have taken on an increasingly important role in the pricing of assets. They also offer an inkling how gold might perform in the future should the holodeck suddenly shut down and substance once again trump perception.

In what has become an often confusing and somewhat frightening investment market governed by silicon-based machines, gold remains the most concrete of assets. It is a real-world island in a sea of algorithms, artificial intelligence, big data and high-frequency trading. If you are like me and do not trust that world instinctively, you will likely find safe harbor in 'old reliable' gold coins and bullion stored safely nearby. Gold, in the end, remains the most effective hedge against the excesses and unpredictability of the new financial virtual reality . . .and what could go wrong with it.

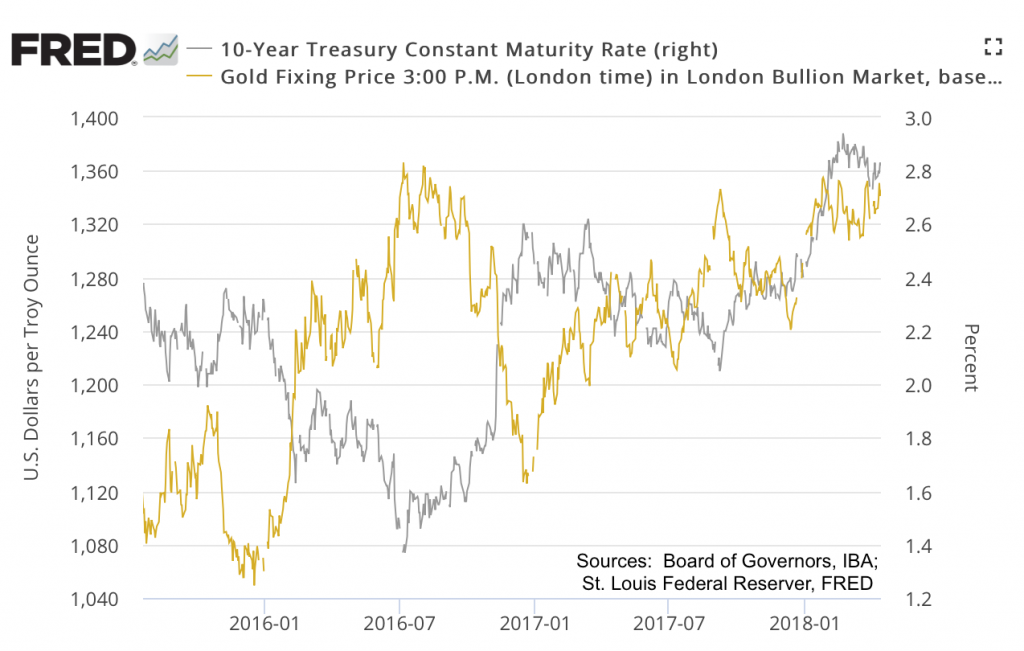

Holodeck #1: Gold and rising interest rates Contrary to popular opinion gold is rising, not falling, as interest rates track higher

Too often gold's critics make the claim that gold reacts unfavorably to rising interest rates. That claim is not borne out by the record. To the contrary, since the Fed began raising interest rates in 2016 the price of gold has tracked higher, as the chart above amply illustrates. "While popular opinion is that interest rate hikes have a bearish effect on gold prices," says Investopedia, "the effect that an interest rate increase has on gold, if any, is unknown, since there is actually little solid correlation between interest rates and gold prices. Rising interest rates may even have a bullish effect on gold prices."

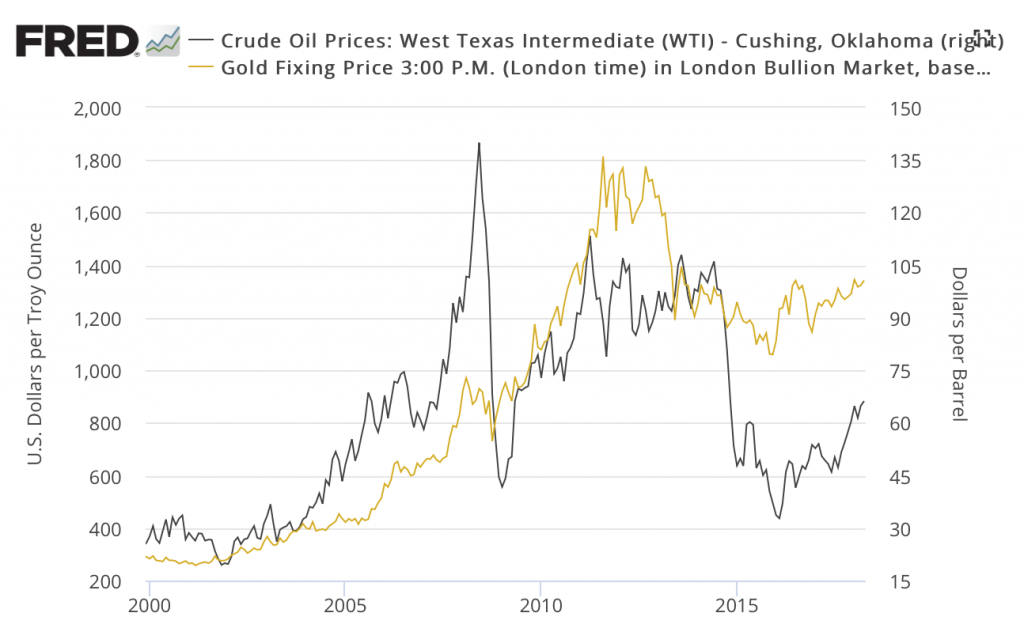

Holodeck #2: Gold and rising oil prices Since 2000, gold and oil have been travelling companions though not in lock-step

Rising oil prices are once again in the headlines and becoming a sensitive matter among consumers. President Trump recently put the blame on OPEC for higher prices thus diverting attention away from his own hardened stance on Iran. A disruption in oil supplies from Iran would have a major impact on prices in Europe and the Far East where much of its oil is exported. The effect on prices, however, will be global. As we move into the summer travel months and the all-important mid-term elections, oil and gasoline prices could become a major issue, thus some say the president's tweet on oil.

Though oil production in the Permian Basin has upped global supplies, logistical problems have kept it from filling the supply gap elsewhere left by OPEC cutbacks. Black gold, in short, could become a juggernaut difficult to slow down and is likely to carry the commodity complex and yellow gold in its tow. In at least a generalized sense oil and gold have been traveling companions since 2000, as shown in the chart above, though not in lock-step. Gold has held up better than oil in the down times oil being the more volatile of the two. We should not forget, too, that oil prices are important in the context of overall inflation. Almost everything produced or manufactured in the United States and elsewhere has an oil component in the pricing equation, including gold.

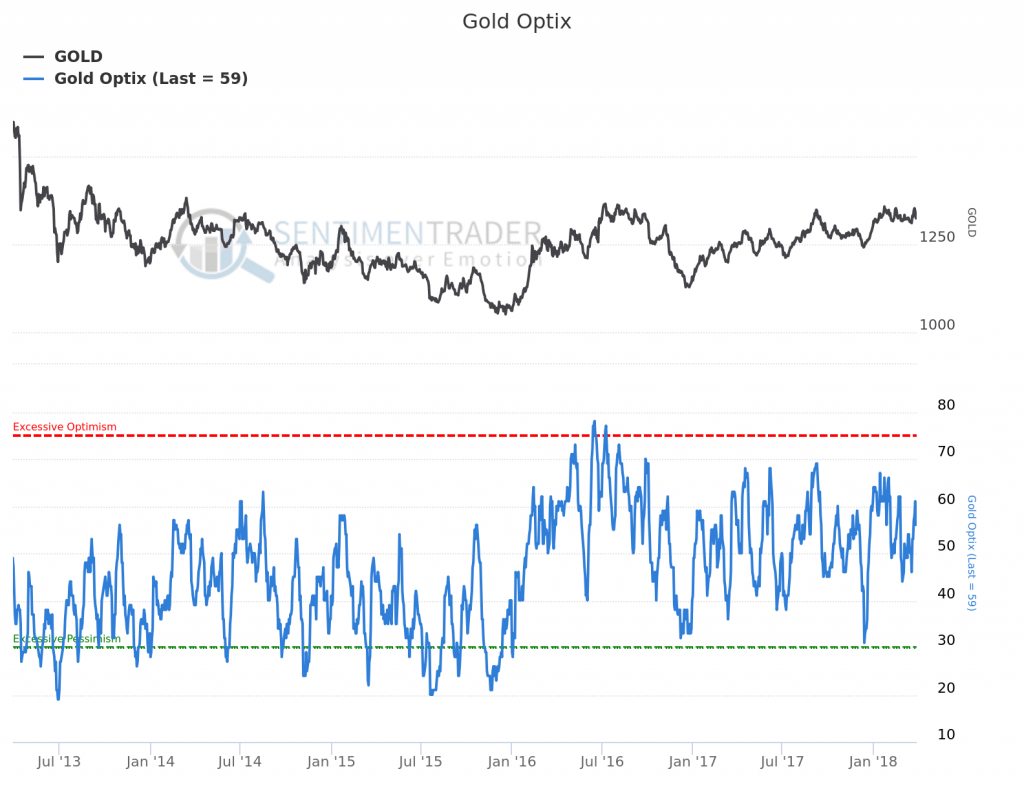

Holodeck #3: Sentiment is swinging toward gold and away from stocks Despite constant media attacks, investor sentiment in gold remains strong, but not too strong

In January I made an out-on-the-limb prediction that gold would trade at $1550 sometime in 2018 and the upside would come the result of a shift in market sentiment. In keeping with that prediction, I thought a closer look at gold sentiment at this juncture would be in order. Gold market sentiment switched gears dramatically at the beginning of 2016 and has remained strong to the present despite the price ups and downs of recent months. Sentiment, as shown above, has renewed its upswing after a couple months of weakness.

I asked Sentiment Trader's Jason Goepfert, the developer of this chart, if he agreed with my assessment that gold sentiment signalled strength building in the gold market something also reflected in a technical analysis of the gold chart (see below). Here is his reply:

"I would agree. Typically when the Optimism Index stays above 50, and rarely goes below 40 during bottoming processes, it's a sign of a solid up trend. Vice-versa for bear markets (stays below 50, with readings above 60 preceding peaks). So the past year or so has been constructive in that regard and I'd rate it as a positive for gold. I'd get nervous if it becomes too optimistic, above 70, or drops below 40 and gold can't rally. So far, no signs of either."

MK's Short & Sweet A live daily newsletter on the gold and silver market Be informed. Stay informed. Expert analysis, news & opinion. Today's full roster of posts ____________________________________________________________________

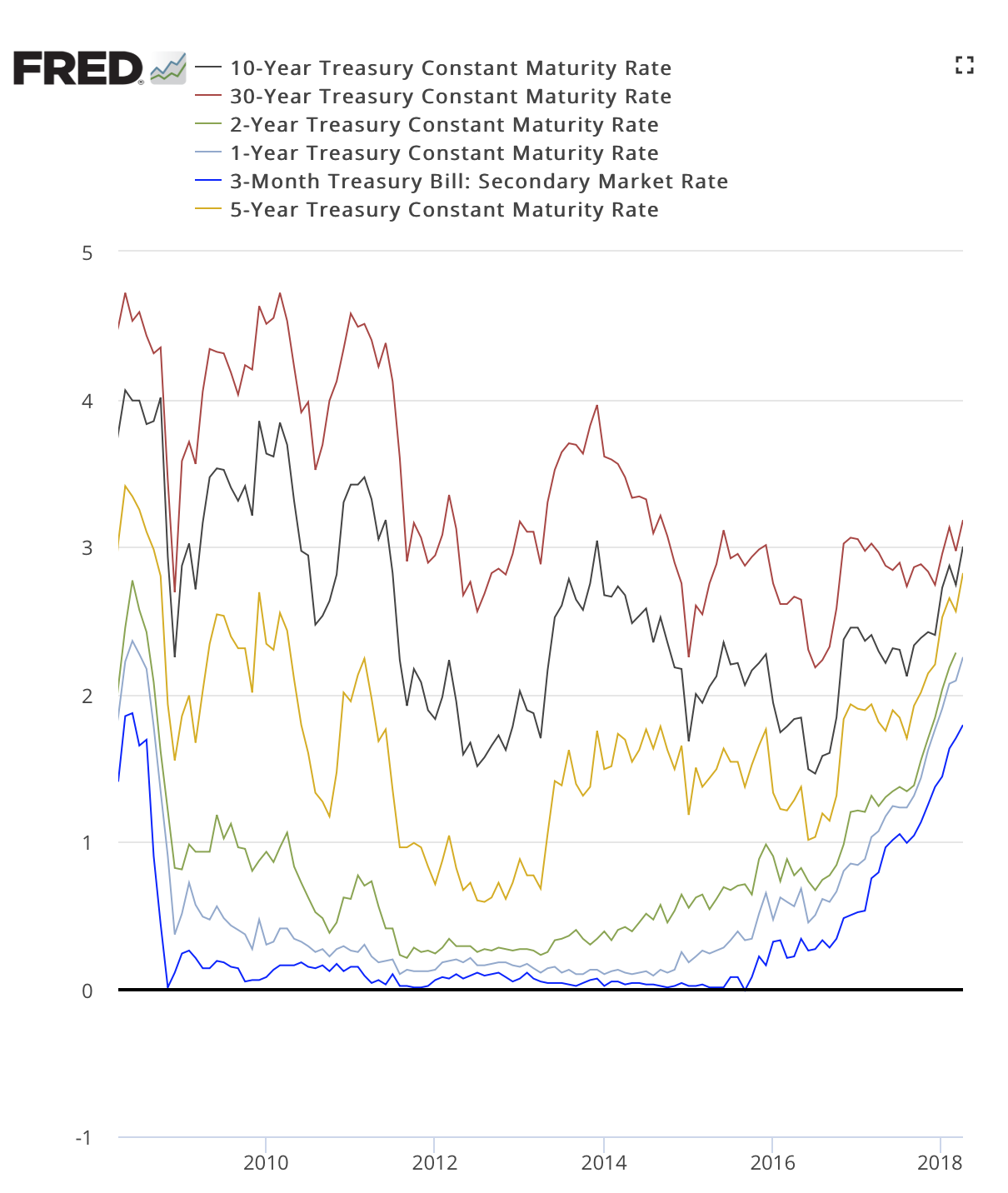

Holodeck #4: Gold and the flattening yield curve Nothing reflects the mysteries of virtual reality like the bond market

The flattening yield curve has garnered considerable attention both from the perspective of investor returns on money and with respect to what it might tell us about the future. We will add one more: What it might mean for the price of gold. One look at the colorful chart above tells us that something is going on, but what something might remains one of the more perplexing mysteries of modern finance. Nothing, in my view, illustrates the perplexing state of finances, i.e., the mysteries John Authers describes above, like this chart. Let me elaborate briefly.

There has been considerable speculation on why the yield curve is flattening, but the one explanation that makes the most sense is that the market is experiencing a unique form of financial schizophrenia. One manifestation is a Dr. Jekyll who believes that higher rates are in the beginnings of a long-term secular up trend in interest rates. He is a buyer of shorter-term securities. The other is a Mr. Hyde believe that the Fed will be forced to throw in the towel and reverse its policy of gradual hikes (and perhaps even being forced to launch another round of rate hikes). He is a buyer of the longer-term securities. As such, the bond market is held in a precarious state of animated suspension.

Gold in this uncertain scenario finds itself in familiar surroundings in a position to play the portfolio safe haven role no matter which way the water runs off this financial divide. One direction would mean inflation. The other would mean disinflation, perhaps even deflation. In either case, gold would succeed where other assets fail.

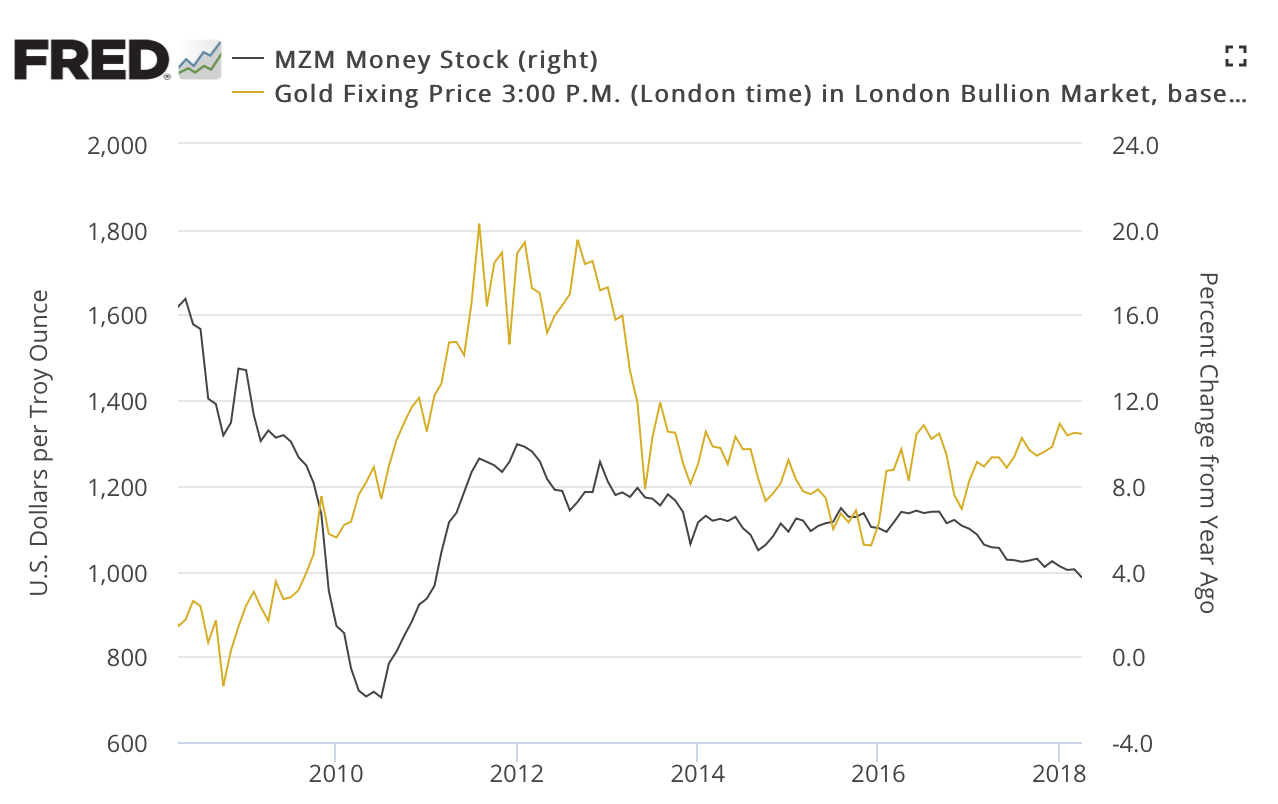

Holodeck #5: Gold and the absence of monetary inflation Inflation's phantom. The Fed turns down the thermostat in an already cold room.

MZM (Money Zero Maturity) is the preferred money supply measure with contemporary economists "because it better represents money readily available within the economy for spending and consumption," according to Investopedia. We hear much about the impending return of inflation these days, but this chart shows no signs of it in monetary growth, the precursor to price inflation. In fact, it shows the complete opposite and trending down not up. The scenario depicted might not be so troubling were it not for the fact that the Federal Reserve created trillions of dollars through its quantitative easing program that somehow, as this chart clearly shows, never made it to the general economy.

Is the Fed, then, turning down the heat in an already cold room as it did in the late 1920s just before the stock market crash of 1929? Such questions raise the prospect of the Fed reacting to a virtual reality a phantom of inflation not its reality. As for gold, it is doing something few would have predicted ten or twenty years ago. It is proving itself an efficient hedge in the current reality against disinflation and the systemic risks it imposes.

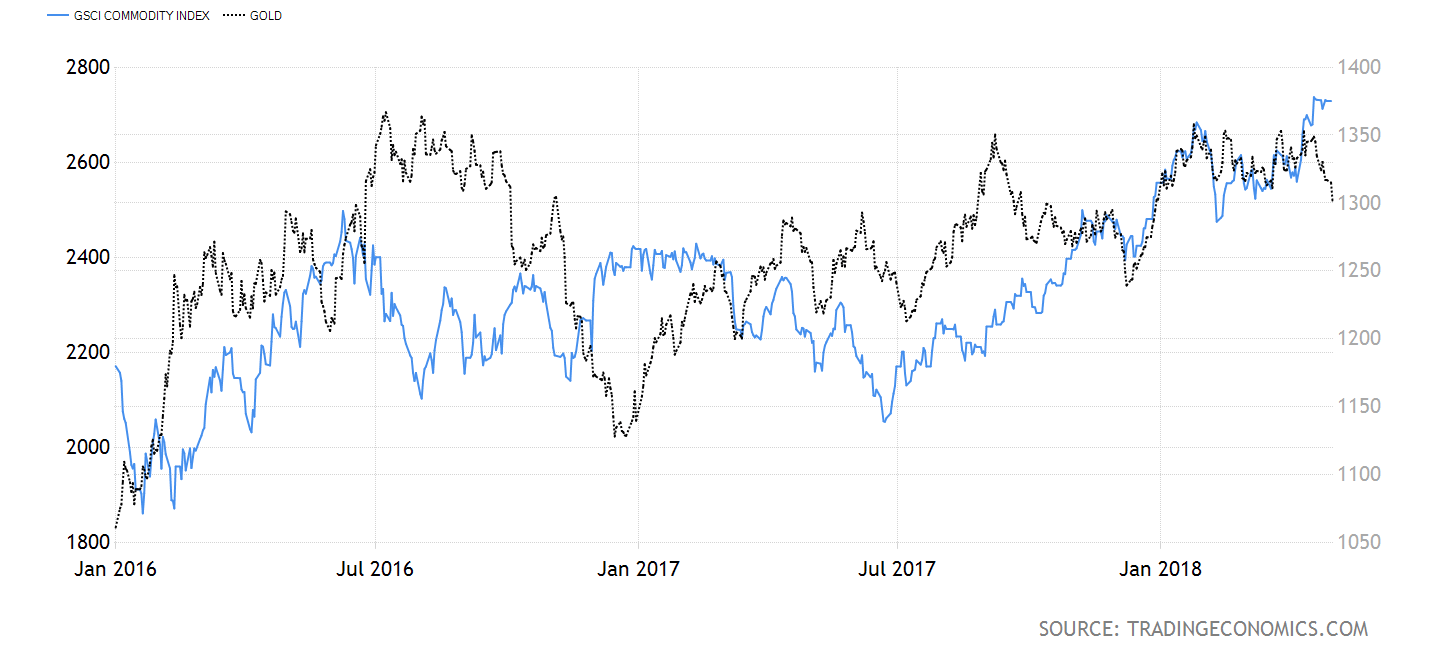

Holodeck #6: Gold and rising commodity prices Here is the rest of the anti-virtual reality story the strengthening commodities complex

One of the pleasant and overlooked surprises for 2018 has been the strength in the commodities complex a development that has spilled over to the gold market. This chart shows the relationship between the two since the beginning of 2016 as reflected in the Standard & Poor's Goldman Sachs Commodities Index. Commodities are up over 21% over the past twelve months as measured by the Goldman Sachs Commodity Index shown in blue in the chart above. Jeff Currie, commodity strategist at Goldman Sachs, recently stated that "the strategic case for owning commodities has rarely been stronger." Gold, at times, has led the index over the past two years, even out-performed it in a couple of instances. Over the past year commodities have played catch-up. Perhaps it is time for gold to jump out and take the lead again. As go commodities, so goes gold.

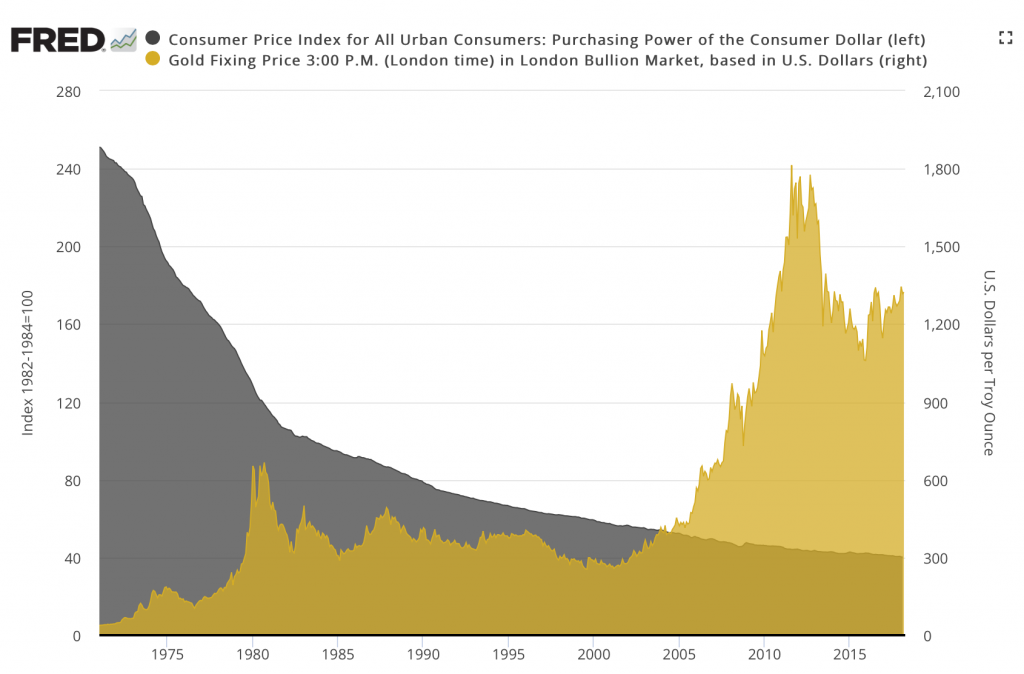

Holodeck #7: Gold and the weakening dollar In financial virtual reality, the dollar is pronounced king and gold a pretender. It is the other way around.

One of the first statements Larry Kudlow made upon assuming the mantle of economic advisor to the president was to reiterate the decades-old strong dollar mantra. He even went so far as to say he would "Buy king dollar and sell gold." This chart (above) illustrates where that "trade" would have gotten the investor since 1970 when the United States severed the link between the dollar and gold and allowed each to float free of each other in the open market.

The dollar over that period, indexed to 100 in 1970, lost 84.3% of its purchasing while gold simultaneously gained in value by 3775% (from $35 in 1970 to yesterday's FOREX close of $1321.00). Since 1995, the year President Bill Clinton's Treasury Secretary, Robert Rubin, first publicly expressed the concept of a strong dollar policy, the greenback has lost 39.2% of its purchasing power. And that occurred during a period of relatively benign price inflation. Gold over the same period gained 377.5% based (from $374.90 in 1995). Rhetoric aside, for the long-term value-oriented investor the real winning trade has been to buy king gold and sell the dollar.

Disclaimer - Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset-preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes and, as such, USAGOLD does not warrant or guarantee the the accuracy, timeliness or completeness of the information found here. (Please see our Risk Disclosure here.)

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.