-- Published: Sunday, 17 June 2018 | Print | Disqus

By John Mauldin

Demographics and Destiny

Triple Threat

Assumed Disaster

St. Louis and Trying to Stay Home

In describing various economic train wrecks these last few weeks, I may have given the wrong impression about trains. I love riding the train on the East Coast or in Europe. Theyre usually a safe and efficient way to travel. And I can sit and read and work, plus not deal with airport security. But in this series, Im concerned about economic train wrecks, of which I foresee many coming before The Big One which I call The Great Reset, where all the debt, all over the world, will have to be rationalized. That probably wont happen until the middle or end of the next decade. We have some time to plan, which is good because its all but inevitable now, without massive political will. And I dont see that anywhere.

Unlike actual trains, we as individuals dont have the option of choosing a different economy. Were stuck with the one we have, and its barreling forward in a decidedly unsafe manner, on tracks designed and built a century ago. Today, well review yet another way this train will probably veer off the tracks as we discuss the numerous public pension defaults I think are coming.

Last week, I described the massive global debt problem. As you read on, remember promises are a kind of debt, too. Public worker pension plans are massive promises. They dont always show up on the state and local balance sheets correctly (or directly!), but they have a similar effect. Governments worldwide promised to pay certain workers certain benefits at certain times. That is debt, for all practical purposes.

If its debt, who are the lenders? The workers. They extended credit with their labor. The agreed-upon pension benefits are the interest they rightly expect to receive for lending years of their lives. Some were perhaps unwise loans (particularly from the taxpayers perspective), but theyre not illegitimate. As with any other debt, the borrower is obligated to pay. What if the borrower simply cant repay? Then the choices narrow to default and bankruptcy.

Todays letter is chapter 6 in my Train Wreck series. If youre just joining us, here are links to help you catch up.

As you will see below, the pension crisis alone has catastrophic potential damage, let alone all the other debt problems were discussing in this series. You are sadly mistaken if you think it will end in anything other than a train wreck. The only questions are how serious the damage will be, and who will pick up the bill.

Its been a busy news year, but one under-the-radar story was a wave of public school teacher strikes around the US. It started in West Virginia and spread to Kentucky, Oklahoma, Arizona, and elsewhere. Pensions have been an issue in all of them.

An interesting aspect of this is that many younger teachers, who are a long way from retirement age, are very engaged in preserving their long-term futures. This disproves the belief that Millennial-generation Americans think only of the present. From one perspective, its nice to see, but they are unfortunately right to worry. Demographic and economic reality says they wont get anything like the benefits they see current retirees receiving. And its not just teachers. The same is true for police, firefighters, and all other public-sector workers.

Thinking through this challenge, Im struck by how many of our economic problems result from the steady aging of the worlds population. We are right now living through a combination unprecedented in human history.

- Birth rates have plunged to near or below replacement level, and

- Average life spans have increased to 80 and beyond.

Neither of these happened naturally. The first followed improvements in artificial birth control, and the second came from better nutrition and health care. Each is beneficial in its own way, but together they have serious consequences.

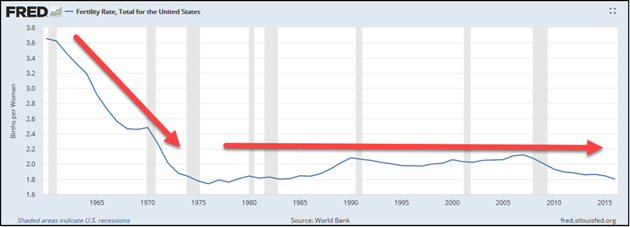

This happened quickly, as historic changes go. Here is the US fertility rate going back to 1960.

Source: St. Louis Fed

As you can see, in just 16 years (19601976), fertility in the US dropped from 3.65 births per woman to only 1.76. Its gone sideways since then. This appears to be a permanent change. Its even more pronounced in some other countries, but no one has figured out a way to reverse it.

Again, Im not saying this is bad. Im happy young women were freed to have careers if they wished. Im also aware (though I disagree) that some think the planet has too many people anyway. If thats your worry, then congratulations, because new-human production is set to fall pretty much everywhere, although at varying rates.

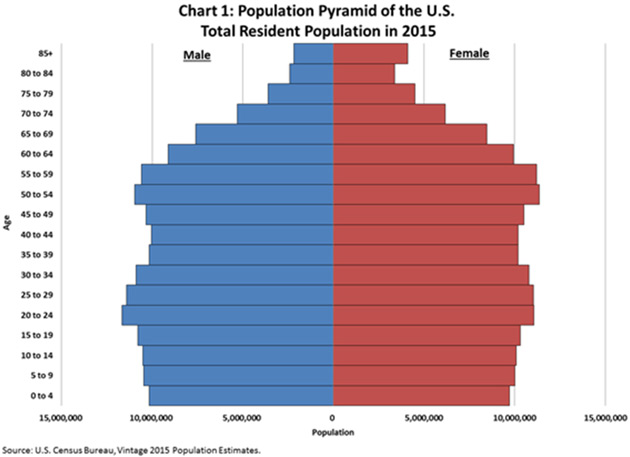

Breaking down the US population by age, heres how it looked in 2015.

Source: US Census Bureau

Think of this as a python swallowing a pig. Those wider bars in the 5054 and 5559 zones are Baby Boomers who are moving upward and not dying as early as previous generations did. Meanwhile, birth rates remain low, so as time progresses, the top of the pyramid will get wider and the bottom narrower. (You can watch a good animation of the process here.)

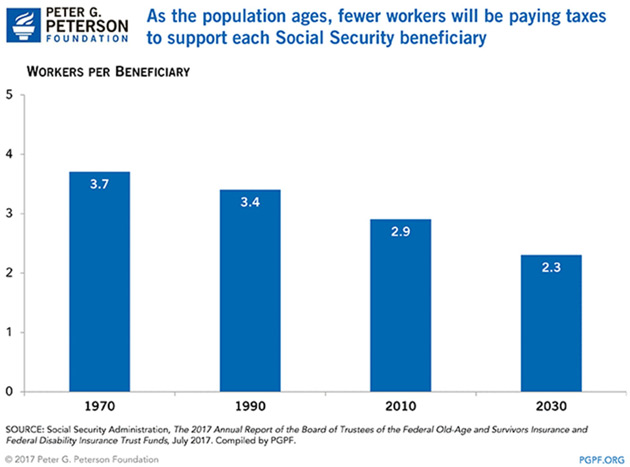

This is the base challenge: How can a shrinking group of working-age people support a growing number of retirement-age people? The easy and quick illustration to this question is to talk about the number of workers supporting each Social Security recipient. In 1940, it was 160. By 1950 it was 16.5. By 1960 it was 5.1. I think you can see a trend here. As the chart below shows, it will be 2.3 by 2030.

Source: Peter G. Peterson Foundation

Similarly, states and local governments are asking current young workers to support those already in the pension system. The math is the same, though numbers vary from area to area. How can one worker support two or three retirees while still working and trying to raise a family with mortgage payments, food, healthcare, etc.? Obviously, they cant, at least not forever. But no one wants to admit that, so we just ignore reality. We keep thinking that at some point in the future, taxpayers will pick up the difference. And nowhere is it more evident than in public pensions.

In a future letter, I will present some good news to go with this bad news. Several new studies will clearly demonstrate new treatments to significantly extend the health span of those currently over age 50 by an additional 10 or 15 years, and the same or more for future generations. Its not yet the fountain of youth, but maybe the fountain of middle-age. (Right now, middle-age sounds pretty good to me.)

But wait, those who get longer lifespans will still get Social Security and pensions. That data isnt in the unfunded projections we will discuss in a moment. So, whatever I say here will be significantly worse in five years.

Let me tell you, thats a high order problem. Do you think I want to volunteer to die so that Social Security can be properly funded? Are we in a Soylent Green world? This will be a very serious question by the middle of the next decade.

We have discussed the pension problem before in this letterat least a half-dozen times. Most recently, I issued a rather dire Pension Storm Warning last September. I said in that letter that I expect more cities to go bankrupt, as Detroit did, not because they want to, but because they have no choice. You cant get blood from a rock, which is what will be left after the top taxpayers move away and those who stay vote to not raise taxes.

This means city and school district retirees will take major haircuts on expected pension benefits. The citizens that vote not to pay the committed debt will be fed up with paying more taxes because they will be at the end of their tax rope. I am not arguing that is fair, but it is already happening and will happen more.

States are a larger and different problem because, under our federal system, they cant go bankrupt. Lenders perversely see this as positive because it removes one potential default avenue. They forget that a states credit is only as good as its tax base, and the tax base is mobile.

Let me say this again because its critical. The federal government can (but shouldnt) run perpetual deficits because it controls the currency. It also has a mostly captive tax base. People can migrate within the US, but escaping the IRS completely is a lot harder (another letter for another day). States dont have those two advantages. They have tighter credit limits and their taxpayers can freely move to other states.

Many elected officials and civil servants seem not to grasp those differences. They want something that cant be done, except in Washington, DC. I think this has probably meant slower response by those who might be able to help. No one wants to admit they screwed up.

In theory, state pensions are stand-alone entities that collect contributions, invest them for growth, and then disburse benefits. Very simple. But in many places, all three of those components arent working.

- Employers (governments) and/or workers havent contributed enough.

- Investment returns have badly lagged the assumed levels.

- Expenses are more than expected because they were often set too high in the first place, and workers lived longer.

Any real solution will have to solve all three challengesdifficult even if the political will exists. A few states are making tough choices, but most are not. This is not going to end well for taxpayers or retirees in those places.

Worse, it isnt just a long-term problem. Some public pension systems will be in deep trouble when the next recession hits, which I think will happen in the next two years at most. Almost everyone involved is in deep denial about this. They think a miracle will save them, apparently. I dont rule out anything, but I think bankruptcy and/or default is the more likely outcome in many cases.

The good news is were starting to get data that might shake people out of their denial. A new Harvard study funded by Pew Charitable Trusts uses stress test analysis, similar to what the Federal Reserve does for large banks, to see how plans in ten selected states would behave in adverse conditions (hat tip to Eugene Berman of Cox Partners for showing me this study).

The Harvard scholars looked at two economic scenarios, neither of which is as stressful as I expect the next downturn to be. But relative to what pension trustees and legislators assume now, theyre devastating.

Scenario 1 assumes fixed 5% investment returns for the next 30 years. Most plans now assume returns between 7% and 8%, so this is at least two percentage points lower. Over three decades, that makes a drastic difference.

Scenario 2 assumes an asset shock involving a 20% loss in year one, followed by a three-year recovery and then a 5% equity return for years five through year 30. So, no more recessions for the following 25 years. Exactly what fantasy world are we in?

Their models also include two plan funding assumptions. In the first, they assume states will offset market losses with higher funding. (Fat chance of that in most places. Seriously, where are Illinois, Kentucky, or others going to get the money?). The second assumes legislatures will limit contribution increases so they dont have to cut other spending.

Admittedly, these models are just thatmodels. Like central banks models, they dont capture every possible factor and can be completely wrong. They are somewhat useful because they at least show policymakers something besides fairytales and unicorns. Whether they really help or not remains to be seen.

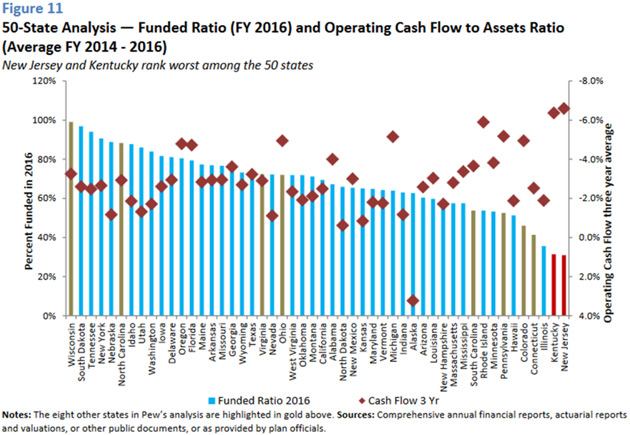

Crunching the numbers, the Pew study found the New Jersey and Kentucky state pension systems have the highest insolvency risk. Both were fully-funded as recently as the year 2000 but are now at only 31% of where they should be.

Source: Harvard Kennedy School

Other states in shaky conditions include Illinois, Connecticut, Colorado, Hawaii, Pennsylvania, Minnesota, Rhode Island, and South Carolina. If you are a current or retired employee of one of those states, I highly suggest you have a backup retirement plan. If you arent a state worker but simply live in one of those states, plan on higher taxes in the next decade.

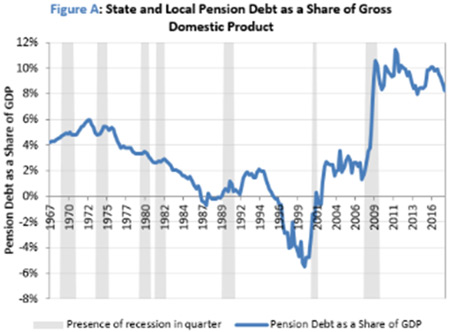

But thats not all. Even if you are in one of the (few) states with stable pension plans, youre still a federal taxpayer, and thats who I think will end up bearing much of this debt. And as noted above, it is debt. The Pew study describes it as such in this chart showing state and local pension debt as a share of GDP.

Source: Harvard Kennedy School

For a few halcyon years in the late 1990s, pension debt was negative, with many plans overfunded. The early-2000s recession killed that happy situation. Then the Great Recession nailed the coffin shut. Now it is above 8% of GDP and has barely started to recover from the big 2008 jump.

Again, this is only state and local worker pensions. It doesnt include federal or military retirees, or Social Security, or private sector pensions and 401Ks, and certainly not the millions of Americans with no retirement savings at all. All these people think someone owes them something. In many cases, theyre right. But what happens when the assets arent there?

The stock market boom helped everyone, right? Nope. States' pension funds have nearly $4 trillion of stock investments, but somehow haven't benefited from soaring stock prices.

A new report by the American Legislative Exchange Council (ALEC) shows why this is true. It notes that the unfunded liabilities of state and local pension plans jumped $433 billion in the last year to more than $6 trillion. That is nearly $50,000 for every household in America. The ALEC report is far more alarming than the report from Harvard. They believe that the underfunding is more than 67%.

There are several problems with this. First, there simply isnt $6 trillion in any budget to properly fund state and local government pensions. Maybe a few can do it, but certainly not in the aggregate.

Second, we all know about the miracle of compound interest. But in this case, that miracle is a curse. When you compute unfunded liabilities, you assume a rate of return on the current assets, then come back to a net present value, so to speak, of how much it takes to properly fund the pension.

Any underfunded amount that isnt immediately filled will begin to compound. By that I mean, if you assume a 6% discount rate (significantly less than most pensions assume), then the underfunded amount will rise 6% a year.

This means in six years, without the $6 trillion being somehow restored (magic beans?), pension underfunding will be at $8.4 trillion or thereabouts, even if nothing else goes wrong.

That gap can narrow if states and local governments (plus workers) begin contributing more, but it stretches credulity to say it can get fixed without some pain, either for beneficiaries or taxpayers or both.

I noted last week in Debt Clock Ticking that the total US debt-to-GDP ratio is now well over 300%. Thats government, corporate, financial, and household debt combined. Whats another 8% or 10%? In one sense, not much, but it aggravates the problem.

If you take the almost $22 trillion of federal debt, well over $3 trillion of state and local debt, and add in the $6 trillion debt of underfunded pensions, you find that the US governments from the top to bottom owe over $30 trillion, which is well over 150% of GDP. Technically, we have blown right past the Italian debt bubble. And thats not even including unfunded Social Security and healthcare benefits, which some estimates have well over $100 trillion. Where is all that going to come from?

Connecticut, the state with the highest per-capita wealth, is only 51.9% funded according to the Wall Street Journal. The ALEC study mentioned above would rate it much worse. Your level of underfunding all depends on what you think your future returns will be, and almost none of the projections assume recessions.

The level of underfunding will rise dramatically during the next recession. Total US government debt from top to bottom will be more than $40 trillion only a few years after the start of the next recession. Again, not including unfunded liabilities.

I wrote last year that state and local pensions are The Crisis We Cant Muddle Through. Thats still what I think. Im glad officials are starting to wake up to the problem they and their predecessors created. There are things they can do to help, but I think we are beyond the point where we can solve this without serious pain on many innocent people. Like the doctor says before he cuts you, This is going to hurt.

Well stop there for now. Let me end by noting this is not simply a US problem. Most developed countries have their own pension crises, particularly the southern Eurozone tier like Italy and Greece. Well look deeper at those next week.

This is not going to be the end of the world. Well figure out ways to get through it as a culture and a country. The rest of the world will, too, but it may not be much fun. Just ask Greece.

I havent done very well staying home in June so far. This week, I made last-minute trips to both New York and Houston. There is actually nothing on my calendar except for one day trip to St. Louis the week after nextuntil a busy August.

There are lots of good things happening in my business and personal life, but its too early to share. And in the spirit of trying to do shorter letters, let me just hit the send button and wish you a great summer week! (Unless, of course, you are in the southern hemisphere.)

Your trying to figure out how we will muddle through this debt train wreck analyst,

| John Mauldin

Chairman, Mauldin Economics |