-- Published: Thursday, 27 September 2018 | Print | Disqus

By Bron Suchecki of the Gold Industry Group

There has been a recent change for the better in central bank attitudes to gold

There has been net gold demand by central banks approx. 500 tonnes per year as a source of return, liquidity and diversification

Policy shift to maintaining stable gold holdings reflects central bank concerns about financial markets and geopolitics

Little in the current global economic and political environment to support any reason to change in this conservative position

Central bank positivity to gold and gold buying should provide long-term underlying support to gold prices

Should central banks hold gold?

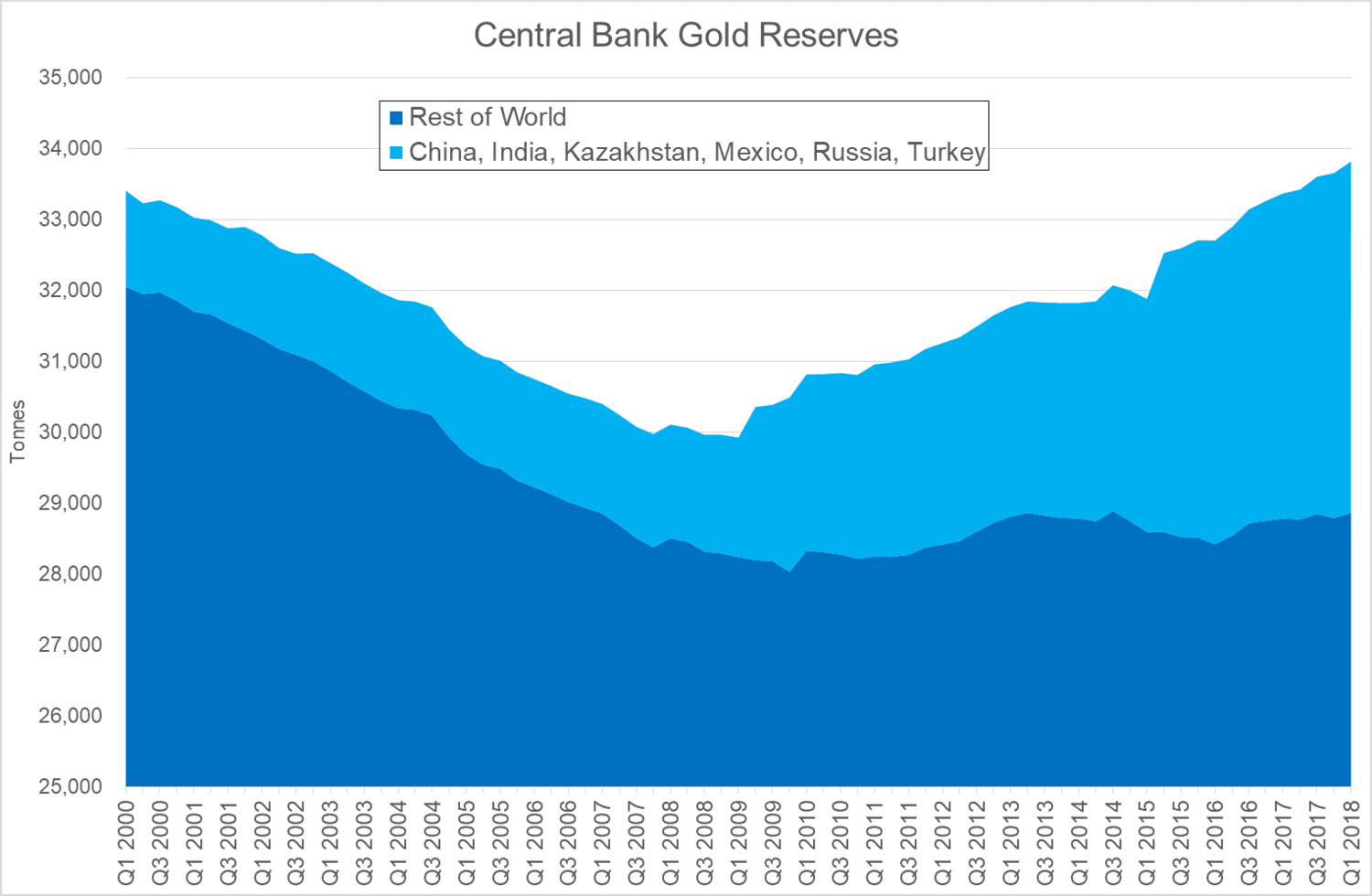

From the late 1980s into the new millennium the answer appeared to be in the negative, with global central bank reserves declining from around 36,000 tonnes to under 30,000 tonnes.

Decades of consistent central bank gold sales were so detrimental to gold market sentiment that in 1999, as gold was selling off towards sub-$250 per ounce, fourteen central banks agreed to limit their selling under the Washington Agreement on Gold. Soon after, gold began its bull market run to over $1,900 although central banks continued to sell, on average, 400 tonnes a year.

Today, at close to 34,000 tonnes, total central bank gold reserves have recovered to a 20-year high, primarily driven by China and Russia and other emerging market countries. A focus on the aggregate figure, however, hides a more fundamental change in central bank attitudes towards gold that occurred after the late 2008 financial crisis, when central bank reserves bottomed.

This chart groups the six central banks who have increased their gold reserves by more than 100 tonnes since the 2008 financial crisis, compared to the remaining central banks. Excluding the key gold accumulating countries of China, India, Kazakhstan, Mexico, Russia and Turkey, the gold holdings of other central banks has been stable since the global financial crisis, a timing which is unlikely to be coincidental.

The chart also shows that that while central bank gold reserves in total are now back to where they were in 1999, almost all of the increase was due to six central banks. As the World Gold Council notes, the expansion of EM foreign reserves has resulted in net gold demand by central banks approx. 500 tonnes per year as a source of return, liquidity and diversification, with many commentators interpreting it as a strategic diversification by China and Russia away from the US dollar.

This is a major structural change in global central bank attitudes towards gold after decades of selling.

Clearly the policy shift to maintaining stable gold holdings reflects broad central bank concerns about financial markets and geopolitics.

With little in the current global economic and political environment to support any reason to change in this conservative position, it should provide long-term underlying support to gold prices.

Courtesy of the Gold Industry Group

News and Commentary

EU Discusses Unilateral No Deal Brexit Contingencies (Bloomberg.com)

Gold prices inch up as investors look for bargains (Reuters.com)

Fed raises U.S. interest rates, sees at least three more years of growth (Reuters.com)

Fed lifts interest rates, no longer says policy is accommodative (MarketWatch.com)

Fed likely to lift rates, possibly end accommodative policy era (Reuters.com)

Gold Prices (LBMA AM)

26 Sep: USD 1,198.80, GBP 910.49 & EUR 1,018.86 per ounce

25 Sep: USD 1,199.45, GBP 912.30 & EUR 1,019.77 per ounce

24 Sep: USD 1,198.75, GBP 913.69 & EUR 1,018.70 per ounce

21 Sep: USD 1,207.60, GBP 914.88 & EUR 1,025.25 per ounce

20 Sep: USD 1,203.00, GBP 910.55 & EUR 1,027.72 per ounce

19 Sep: USD 1,203.00, GBP 912.48 & EUR 1,028.44 per ounce

Silver Prices (LBMA)

26 Sep: USD 14.48, GBP 11.01 & EUR 12.32 per ounce

25 Sep: USD 14.29, GBP 10.86 & EUR 12.15 per ounce

24 Sep: USD 14.32, GBP 10.90 & EUR 12.17 per ounce

21 Sep: USD 14.33, GBP 10.87 & EUR 12.18 per ounce

20 Sep: USD 14.23, GBP 10.75 & EUR 12.14 per ounce

19 Sep: USD 14.18, GBP 10.76 & EUR 12.13 per ounce

Recent Market Updates

Central Banks Positivity Towards Gold Will Provide Long Term Support To Gold Prices

Europe Unveils Special Purpose Vehicle With Russia and China To Bypass SWIFT, Jeopardizing Dollars Reserve Status

Gold Set to Soar Above $1,300 Goldman and Bank of America

Goldnomics Podcast: Silver Guru David Morgan Silver and Gold Will Protect in the Coming Currency Collapse

This Weeks Golden Nuggets Dalios Dollar Crisis, Fitts U.S. Government Missing $21 Trillion and Silver Gurus End of Empire

Dalio Warns Of Dollar Crisis History Is Doomed To Repeat Itself

Silver Guru Video: The End of Empire and End of Fiat Currencies

Silver Is Undervalued Relative to Stocks, Bonds, Gold GoldCore

We Are In Never Never Land Accounting As U.S. Government Is Missing $21 Trillion

This Weeks Golden Nuggets BOE Warns Of UK House Price Crash

Mark O'Byrne

Executive Director

| Digg This Article

-- Published: Thursday, 27 September 2018 | E-Mail | Print | Source: GoldSeek.com