We Could See $100 Oil Again Soon, But Not for the Reason You Think

-- Published: Tuesday, 9 October 2018 | Print | Disqus

By Frank Holmes

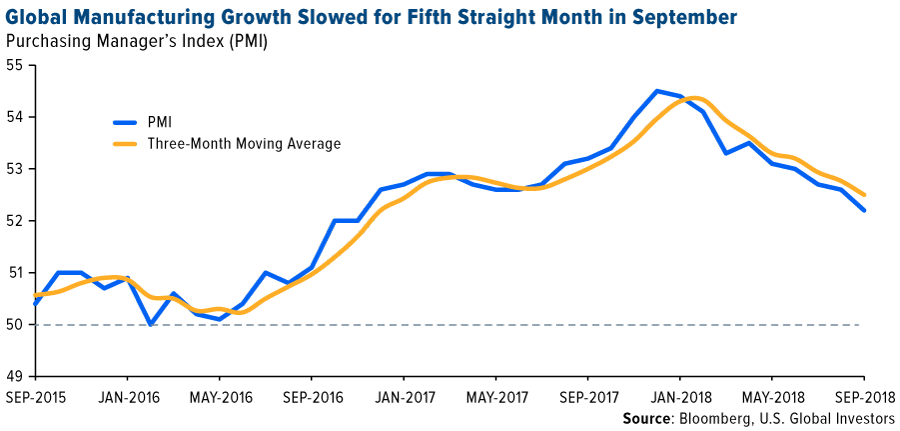

According to a recent Cornerstone Macro report, the three most influential macro trends this year have been 1) the strengthening U.S. dollar, 2) the flattening yield curve and 3) slowing global manufacturing expansion. Ive written about all three topics numerous times this year, but the one Ive watched the most closely has been global manufacturing, as measured by the purchasing managers index (PMI). Since its 12-month high of 54.5 in December 2017, the PMI has declined in eight of the past nine months. September marked the fifth straight month of slower manufacturing growth.

This matters because the PMI is a useful, forward-looking indicator of the economic health of the manufacturing sector, which accounted for around 15.6 percent of global gross domestic product (GDP) in 2016. Our research has shown that the index can be used to forecast world demand for materials and energy one, three and six months out, with a reasonable measure of accuracy.

Take a look below. The chart shows that, based on 10 years worth of data, copper and West Texas Intermediate (WTI) crude, as well as energy and materials equities, all benefited in the three months after the PMI crossed above its three-month moving average. WTI saw the biggest jump; 64 percent of the time, it gained 5 percent on average.

Conversely, in the three months after the PMI crossed below its three-month moving average, those same assets either fell or were effectively flat. Seventy-one percent of the time, copper lost a little over 1.5 percent on average when manufacturing growth began to slow.

So how accurate has the PMI been so far this year? The index crossed below its moving average in February, and since then, materials have predictably failed to gain traction. The S&P 500 Materials Index is down about 6 percent, while copper prices are off 13 percent on fears that demand in China, the worlds largest consumer of the metal, is shrinking. (Australian miner BHP Billiton reported last week, however, that it believes Chinese copper consumption is actually set to increase substantially, by as much as 1.6 million metric tons, between now and 2023, thanks to its ambitious Belt and Road Initiative (BRI)).

Crude oil and energy stocks, on the other hand, have fared very well on tightening supply in Venezuela and Iran, the latter of which is scheduled to face a new round of U.S. sanctions effective November 4. Since February, WTI prices have surged 13.6 percent and are now at four-year highs, while the S&P 500 Energy Index is up 2.7 percent. Oil traders are now betting that crude could rise to as high as $100 a barrel by next year, Reuters reports.

Does oils outperformance, despite a steadily cooling PMI, mean our research is flawed? Hardly. The index, remember, only tells us the probability that a price change will occur. Extraordinary government policies, such as the U.S. reimposing sanctions on Iran, must also be taken into consideration. If the PMI alone were 100 percent accurate 100 percent of the time, we would all be multibillionaires from betting on the winners every time. Sadly, thats not the case.

Could We Reach Peak Oil Sooner Than Anticipated?

But back to $100-per-barrel oil. Not only are traders betting on a return to these prices, but banks are also baking it into their forecasts. In a note last week, HSBC said it sees real risks of this happening by 2020, adding that there are clear signs of falling exports and builds in Iranian exports. We would expect to see much more tangible signs of falling exports ahead of the November cut-off.

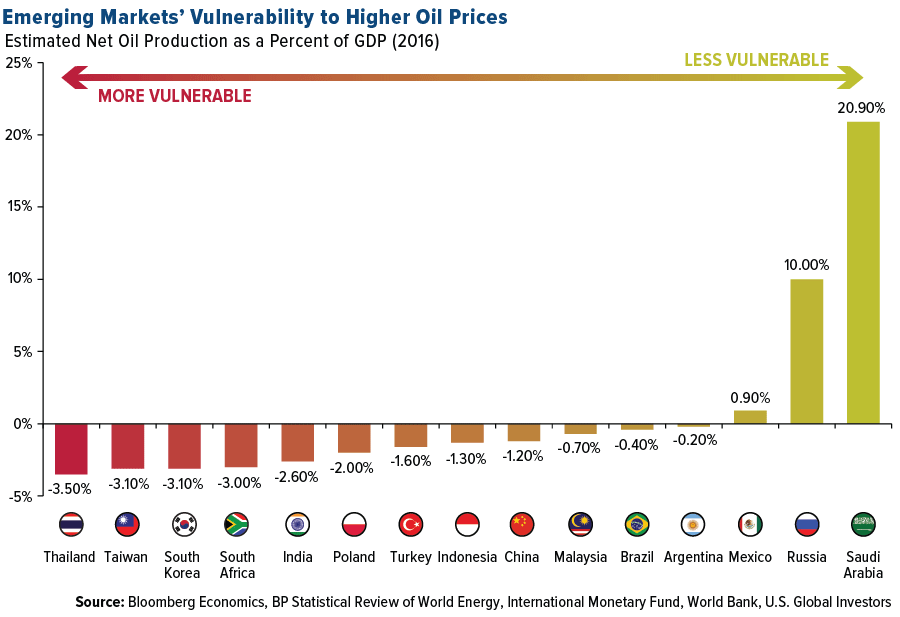

So how will this affect the global economy? It shouldnt come as a surprise that net import countries would be most impacted by higher fuel costs. Among the emerging markets Bloomberg Economics estimates would feel the greatest pain are Thailand, South Korea, South Africa and India. Conversely, the economies that stand to benefit the most from rising oil prices are Mexico, Russia and Saudi Arabia.

Even higher prices could become a reality as soon as the next decade if world supply continues to tighten. Energy and mining research firm Wood Mackenzie (WoodMac) recently issued a warning that not enough oil discoveries are being made to replace capacity. We need more Guyanas, a lot more, and we need them soon, WoodMac chairman and chief analysts Simon Flowers urged, referring to the massive find made in the South American country early last year.

Spending on exploration collapsed following the price crash in 2014, which has propelled the world closer to peak oil much sooner than anticipated.

The oil market could be running short of oil capacity by the late-2020s at the current low discovery rate, Flowers said. Thats worryingly near at hand given it takes the best part of 10 years for the average new discovery to build to peak production.

The supply gap, according to WoodMac, could reach 3 million barrels per day (b/d) by 2030, 9 million b/d by 2035 and a formidable 15 million b/d by 2040.

A Promising New Copper Discovery

Speaking of new discoveries, I want to congratulate my friend Robert Friedland, founder and executive chairman of Ivanhoe Mines. The Canadian copper mining company announced last week the important new discovery of the metal on its 100 percent owned Western Foreland property in the Democratic Republic of Congo (DRC). Makoko, as its called, is Ivanhoes third major find in the DRC, following Kamoa-Kakula, which WoodMac has called the worlds largest, undeveloped, high-grade copper discovery.

After last Mondays announcement, shares of Ivanhoe popped 9 percent on the Toronto Stock Exchange.

In the press release, Robert chalked the find up to the accumulation of in-depth, proprietary geological insights gained by Ivanhoes exploration team during nearly two decades of exploring in the region.

Given the early drilling success at Makoko, he added, we are highly confident that we have the secret blueprint for additional exploration successes in the Western Foreland area in 2019 and beyond.

Earlier this year, Robert visited our office and said that by 2021, youre going to need a telescope to see copper prices. Chinas BRI, as I mentioned earlier, is expected to boost demand dramatically as scores of new power plants and electrical grids come online. The Asian giant has also joined several other countries in requiring that electric vehicles (EVs) replace gas-powered ones over time. EVs need three to four times as much copper as traditional vehicles do.

With copper prices down close to 16 percent for the year, now might be an ideal buying opportunity.

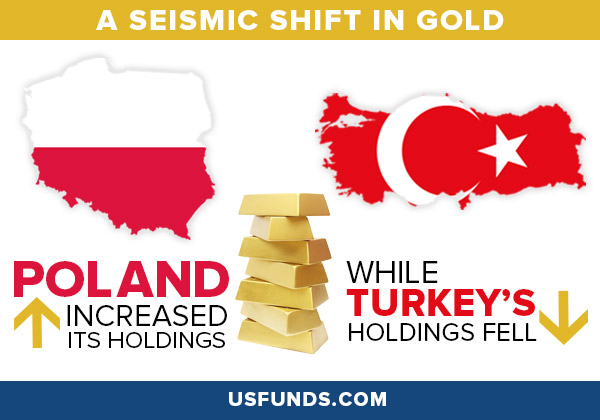

Poland Adds to Its Gold Reserves. Should You?

Stocks sold off more sharply late last week than weve seen since late June, with the S&P 500 Index sliding below its 50-day moving average. The unemployment rate fell to 3.7 percent, its lowest level in nearly half a century, convincing many investors that the Federal Reserve will now begin to raise rates more aggressively in an effort to prevent the economy from overheating.

Meanwhile, the trade dispute between the worlds two largest economies doesnt appear to be abating anytime soon. Now that President Donald Trump has succeeded in rebooting NAFTAprovided it gets ratified by Congresshes likely to turn up the heat on Beijing. Some analysts predict the U.S. will eventually max out tariffs on all Chinese imports. J.P. Morgan now forecasts a full-blown trade war as its new base case scenario for 2019.

The U.S. economy is humming along robustly, but its better to prepare for the next downturn while the bull is still running than after its crashed into a wall. Last week I spoke with Daniela Cambone of Kitco News and explained the reasons why Im bullish on gold, including Vanguards decision to slash its exposure to metals and mining, and the recent Barrick Gold-Randgold Resources merger deal.

During the interview, I also discussed the news that Poland purchased gold this pastsummer at a pace not seen in 20 years. The Eastern European country, which was just upgraded to a developed market, added nine metric tons to its gold reserves in July and August, the most since 1998, and the most by any European Union country in the past two decades. Speaking with Bloomberg, mBank senior economist Marcin Mazurek said the Polish central banks decision was likely based on diversification, combined with the expectation for higher global inflation.

You can watch my full interview with Daniela Cambone by clicking here.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2018): BHP Billiton Ltd., Ivanhoe Mines Ltd.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

The S&P 500 Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The S&P 500 Energy Index comprises those companies included in the S&P 500 that are classified as members of the GICS energy sector. The S&P 500 Materials Index comprises those companies included in the S&P 500 that are classified as members of the GICS materials sector.

The Purchasing Managers Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.