-- Published: Monday, 22 October 2018 | Print | Disqus

By Avi Gilburt

The general investment public usually applies the same principles when they choose how and when to invest their hard-earned money. (And we wonder why the general public always gets caught holding the bag at the highs and selling at the lows?) And, much of these principles are merely phrases which sound reasonable, but when analyzed, one realizes that they are lacking in substance.

One such phrase is that the gold market is driven by supply and demand. It certainly sounds great and has been propagated through the market to make it sacrosanct. But, when you think about it beyond the simple phrase, how does it help you invest? What drives demand? What drives supply?

Well, I think we can all recognize that supply is driven mostly by demand, as the gold mines will ramp production when there is greater demand. While one can always find markets where supply has its own driver, such as the weather in agriculture having an affect upon supply, much of the market is truly focused on the demand for gold. Yet, have you ever heard anyone discuss what drives demand?

In a recent article I read, I think they summed up demand quite well (but I will not address the rest of the article which, in my humble opinion, presents old and outdated thinking regarding price drivers):

Demand in economics is the consumer's desire and ability to purchase a good or service. It's the underlying force that drives economic growth and expansion. Without demand, no business would ever bother producing anything.

So, many view demand as the basis for driving business and/or the price of any asset. But, again, what drives demand? Is that not the most important question to ask in order to determine at what level an asset should be priced?

Well, this is where I come back to market sentiment. When the market is in the throes of a positive sentiment trend for a particular asset, the price of that asset gets bid up. However, when the positive sentiment wanes, and then market then turns negative, the bid under the asset dries up, and eventually turns in the other direction. This is simply how markets work. In fact, a bull market does not die because of selling. Rather, a bull market dies because of a lack of marginal buyers. When everyone is already bullish, who is left to push the price higher?

Bernard Baruch, an exceptionally successful American financier and stock market speculator who lived from 1870 1965, identified the following long ago:

All economic movements, by their very nature, are motivated by crowd psychology. Without due recognition of crowd-thinking ... our theories of economics leave much to be desired. ... It has always seemed to me that the periodic madness which afflicts mankind must reflect some deeply rooted trait in human nature a trait akin to the force that motivates the migration of birds or the rush of lemmings to the sea ... It is a force wholly impalpable ... yet, knowledge of it is necessary to right judgments on passing events.

So, while it sounds great to say that the market is driven by supply and demand, until one can learn how to track that from a price perspective in a consistent and accurate manner, all this phrase provides to the average investor is a nicety without much substance. So, the next time someone tells you that the price of gold is driven by the laws of supply and demand, push them a bit harder and ask them what drives demand for gold. I am quite certain it will lead to one of the usual fallacies of what drives gold.

That brings me to my next point.

One of the perspectives I noted in my weekend reading within the gold market was a repetition of the fallacy that the demand for gold rises during a stock market correction, resulting in a price increase or rally for gold. In fact, this is simply based upon the common fallacy that gold is a safe haven for stock market volatility, but presented in a slightly different way. But, yes, they are both fallacies.

I have written many articles on this issue, and here is a link to my most recent missive on the topic.

For those unable to access it, here is the relevant section on the matter:

You see, the metals rallied quite strongly in early 2016, and we did not even have a stock market crash. In fact, as I warned would occur in late 2015, they rallied together. I bet many of you did not even think this is possible. Now, after you pick your chin up off the floor, you should also realize that this is not the first time this has occurred, nor will it be the last.

So, allow me to show you why only expecting an inverse correlation between equities and metals is just outright wrong.

We will begin with the 2007-2009 time frame, which evidenced the most significant period of market volatility since the Great Depression. Let's see if we can glean anything from the metals action in order to determine whether they are the safe haven everyone is selling you on.

We all know that the S&P 500 topped in October of 2007 and began an estimated 300-point decline into March of 2008, and then we saw a corrective bounce in the equities for a couple of months, before it continued to head down. During that same period of time, even while the markets were heading lower, the metals continued to rally strongly. Here we have "evidence" of precious metals supposedly rising during a period of market volatility.

But, when we then look toward the May 2008-March 2009 decline in the equity market, we have clear evidence that the metals also experienced significant declines within that time period. In fact, gold lost a little more than 30% during that time period. So, here we have a period of time where the metals were moving in the same direction as the equity markets, and clearly not acting like a supposed "safe haven."

But gold also found a bottom and began to rally four months before the equity markets, after which time, they began to rally together again for two years.

So, when one is presented with these facts, does it make sense that the metals are surely going to rise during periods of market volatility? Are metals really the "safe haven" everyone believes they are during down markets? Are these markets inversely correlated as so many claim?

If you need further evidence, consider this additional fact. Back in 2008, the folks at Elliott Wave International published a study that showed that in 10 out of 11 recessionary periods since 1945 gold experienced a negative total return.

For further evidence that one should not assume the two markets move inversely, one simply has to look back to the period of time between 2003-2008. During those 5 years, the metals rallied alongside the equity markets. And, no, this is not a misprint.

So, when one is presented with these facts, can you really believe that metals are the "safe haven" everyone claims they are during down markets? Can one also come to the conclusion that these two markets trade inversely with each other? So, should you be buying metals only because you believe the stock market is going to crash?

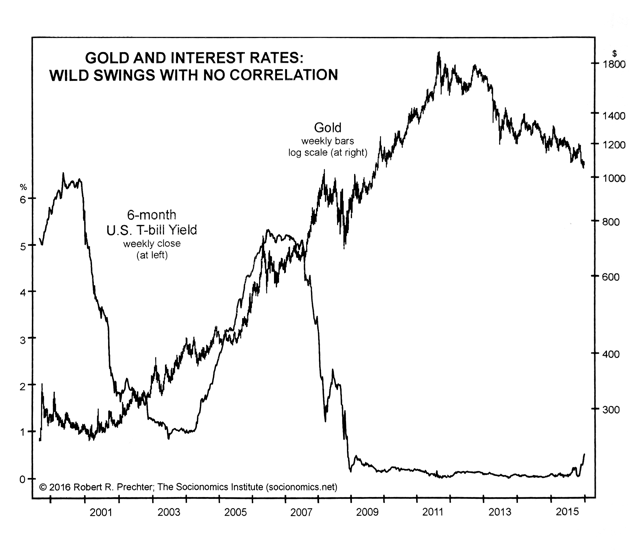

The last fallacy I would like to confront is the fallacy that relationship between interest rates and gold. I have heard arguments from both sides on this one, and while there is a large camp that believes rising interest rates is positive for gold, unfortunately, history again will shine the light of truth on this fallacy.

Source: Robert Prechter, The Socionomics Institute.

I dont think there is much to say after you review this chart.

Isnt it amazing what one learns when we shine a light of truth and market history on some of the fallacies propagated throughout the media?

As I wrote in my prior article, I want to thank all of you who have trusted me to the point where you have chosen to follow me during the time I have been writing at Seeking Alpha. In fact, I just hit a major milestone of 30,000 followers. For that, I am very grateful, honored and humbled.

During that time, many of you have questioned me as to why I do these types of write-ups in my articles. The answer is quite simple, as I explained to some commenters. I believe in honesty, especially intellectual honesty. And, I get so frustrated by people who do not think for themselves and are brainlessly fed what to think by the news media and analysts. So, my articles are designed to push people to think for themselves in an intellectually honest manner rather than buy into what they are fed in print and on television.

In fact, I take pleasure in being able to open peoples minds to much of the intellectual dishonesty that is presented in the guise of market analysis. And, I find this effort to be extremely rewarding as I have received thousands of notes, posts, emails, private messages and comments over the last seven years telling me how I have changed peoples lives. Isn't that one of the purposes for which we were put here by our creator?

So, within this current missive, I sincerely hope I have dispelled the notion that metals trade inversely to the stock market and have dispelled the fallacy that they are a safe haven when we are experiencing equity market volatility. History has a way of proving truths and dispelling falsehoods, no matter how commonly adopted. As Elliott eloquently stated:

In the dark ages, the world was supposed to be flat. We persist in perpetuating similar delusions.

R. N. Elliott, Nature's Law, 1946

Avi Gilburt is a widely followed Elliott Wave technical analyst and founder of ElliottWaveTrader.net, a live Trading Room featuring his intraday market analysis (including emini S&P 500, metals, oil, USD & VXX), interactive member-analyst forum, and detailed library of Elliott Wave education.

| Digg This Article

-- Published: Monday, 22 October 2018 | E-Mail | Print | Source: GoldSeek.com

{kind=link}