Debt is future spending pulled forward in time. It lets you buy something now for which you otherwise dont have cash yet.

Whether its wise or not depends on what you buy. Debt to educate yourself so you can get a better job may be a good idea. Borrowing money to finance your vacation? Probably not.

The problem is that many people, businesses, and governments borrow because they can. Its been possible in the last decade only because central banks made it so cheap.

It was rational in that respect. But it is growing less so as the central banks start to tighten.

Earlier this year, I wrote a series of articles (synopsis and links here) predicting a debt train wreck and eventual liquidation. I dubbed it The Great Reset. I estimated we have another year or two before the crisis becomes evident.

Now Im having second thoughts. Recent events tell me the reckoning could be closer than I thought just a few months ago.

Debt Doesnt Fuel Growth Anymore

Central banks enable debt because they think it will generate economic growth. Sometimes it does. The problem is they create debt with little regard for how it will be used.

Thats how we get artificial booms and subsequent busts. We are told not to worry about absolute debt levels so long as the economy is growing in line with them.

That makes sense. A country with a larger GDP can carry more debt. But that is increasingly not what is happening.

Let me give you two data points.

Hoisington Investment Managements Lacy Hunt tracks data that shows debt is losing its ability to stimulate growth. In 2017, one dollar of non-financial debt generated only 40 cents of GDP in the US. Its even less elsewhere. This is down from more than four dollars of growth for each dollar of debt 50 years ago.

This has seriously worsened over the last decade. Chinas debt productivity dropped 42.9% between 2007 and 2017. That was the worst among major economies, but others lost ground, too. All the developed world is pushing on the same string and hoping for results.

Now, if you are used to using debt to stimulate growth, and debt loses its capacity to do so, what happens next? You guessed it: The brilliant powers-that-be add even more debt.

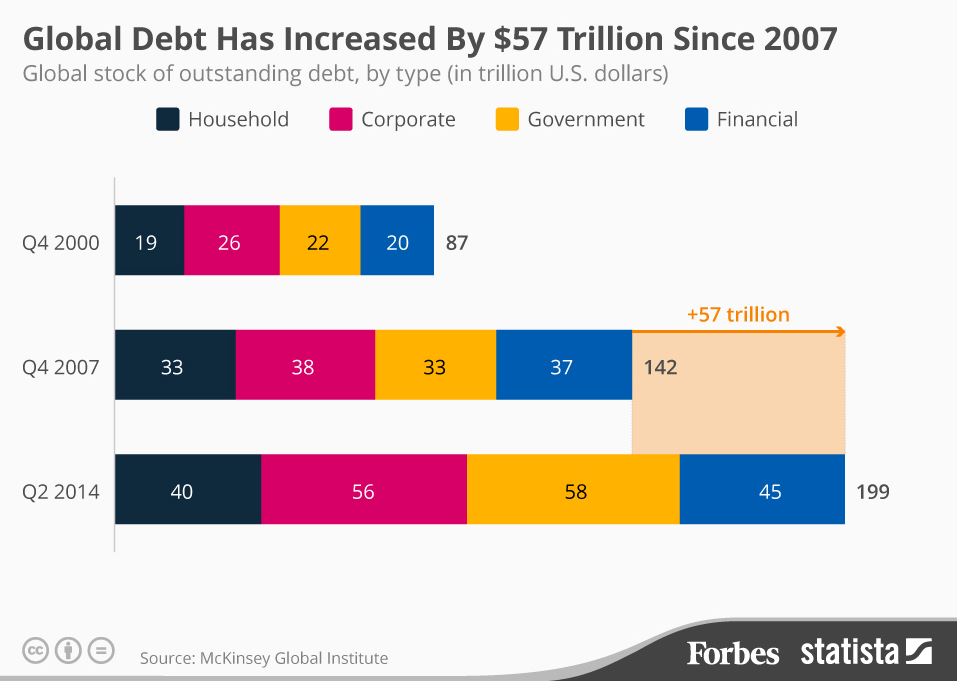

Heres How Much Debt We Actually Have

This is classic addiction behavior. You have to keep raising the dose to get the same high.

But centuries of history show that every prior debt run-up eventually took its toll on the economy. There is always a Day of Reckoning.

The US economy is so huge and powerful that our current $24.5 trillion government debt (including state and local) could easily grow to $40 trillion before we meet that day. We are one recession away from having a $30 trillion U.S. government debt total.

It will happen seemingly overnight. And deficits will stay well above $1 trillion per year every year after that, not unlike now.

Even though a budget deficit is under $800 billion this year, we added over $1 trillion of actual debt. That is due to off budget items that Congress thinks shouldnt be part of the normal budgetary process.

It includes things like Social Security and Medicare They vary from time to time and year to year and can be anywhere from $200 billion to almost $500 billion.

And heres the point that you need to understand. The U.S. Treasury borrows those dollars and it goes on the total debt taxpayers owe. The true deficit that adds to the debt is actually much higher than the number you see in the news.

Household and corporate debt is growing fast, too. And not just in the U.S.

Heres a note from Economic Cycle Research Institutes Lakshman Achuthan:

Notably, the combined debt of the US, Eurozone, Japan, and China has increased more than ten times as much as their combined GDP [growth] over the past year.

Yes, you read that right. In the last year, the worlds largest economies are generating debt 10X faster than economic growth. Adding debt at that pace, if it continues, will boost the debt-to-GDP ratio at an alarming rate.

Lakshman continues.

Remarkably, then, the global economyslowing in sync despite soaring debtfinds itself in a situation reminiscent of the Red Queen Effect we referenced 15 years ago, when tax cuts boosted the US budget deficit much more than GDP. As the Red Queen says to Alice in Lewis Carrolls Through the Looking Glass, Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!

This Wont End Well

I am trying to imagine a scenario where this ends in something less than chaos and crisis. The best I can conceive is a decade-long (and possibly more) stagnation while the debt gets liquidated.

But realistically, that wont happen because debtors wont let it. And they outnumber lenders. For this reason, something like the Great Reset will happen first.

The rational course would be to delay the inevitable as long as possible. Yet in the U.S. were rushing it.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.