If we are, as I believe, on the precipice of a major decline in stocks, the question in my mind as we head into 2019 is to what extent U.S. Treasuries will continue to be the main go-to market in the risk-off trade and to what extent might a loss of confidence in the dollar as the worlds reserve currency lead to a rise in the price of gold?

The answer requires an examination of likely flows of money in 2019 and beyond, and those flows are very much determined by the point at which we exist in the current credit cycle.

We are in one of the longest credit cycles on record, with 2018 being the tenth year of expansion. GoldMoneys Alasdair Macleod quite correctly points out that in the late stages of the credit cycle money flows out of the financial sector into the real economy and with the flow out of financial assets, interest rates begin to rise.

10-Year U.S. Treasury yields rose from 1.385% on July 5, 2016, to 3.227% on October 1, 2018. The 10-year rate has corrected to 2.652% as of this writing, but it is clear that with the real economy doing better, interest rates have risen, which in turn has put downward pressure on stocks. With increased volatility in U.S. equities, the recent decline in rates reflects the safe haven risk off attitude.

But should we take it as a given, as most mainstream analysts do, that a flow out of stocks automatically means the only safety bunker to hide out in when stocks collapse is the U.S. Treasury market? The answer is an unequivocal NO! As Alasdair points out, in the late stages of a credit cycle, Main Street bids the total flows of money away from financial assets. So yes, some money has flowed from stocks to U.S. Treasuries in the latest equity market decline, thus providing the correction noted above since October 2018 in the 10-Year Treasury. But the point remains that in the late stages of the credit cycle, less money flows into financial assets, thus causing their prices to decline.

Once a major crash occurs and a new round of QE is administered, a new cycle usually begins. But can we assume that will happen again, especially with the existing credit cycle bubble, which is now the biggest global bubble yet by far?

Given its confidence in the ability of the PhD standard to replace the gold standard, mainstream pundits assume the U.S. Treasury market is better than gold. And the standard answer to my question is a resounding Yes! Taylor, cant you see the performance of geniuses like Greenspan and Bernanke? Well, this 71-year-old author is old enough to remember when the gods of money were not able to hold the system together. During the late 1970s, there was a massive exodus from both stocks and bonds, while at the same time, gold rose from $35 to a momentary $850 price tag.

Might we now be facing a replay of the late 1970s when confidence is lost in the governments ability to repay its debt obligations? And given the magnitude of much greater debt and debt to GDP ratios, might the pathology be many, many times greater than the late 1970s when confidence was lost in the dollar and gold skyrocketed from $38 to $850 in just a couple of years? Alasdair noted in his January 3 missive that The credibility of government debt is based on the assumption the issuer can afford to continue to roll it over rather than repay it.

Everyone knows the U.S. debt of $22 trillion will never be repaid, but at present the assumption remains that it can always be rolled over. But that assumption was lost in the late 1970s after Nixon removed the gold standard from international trade and the U.S. began printing mountains of dollars out of thin air to pay for socialism and Vietnam. Years of con-artistry since then by Keynesian central banks have left most investors confident that elitist bankers can always save the day.

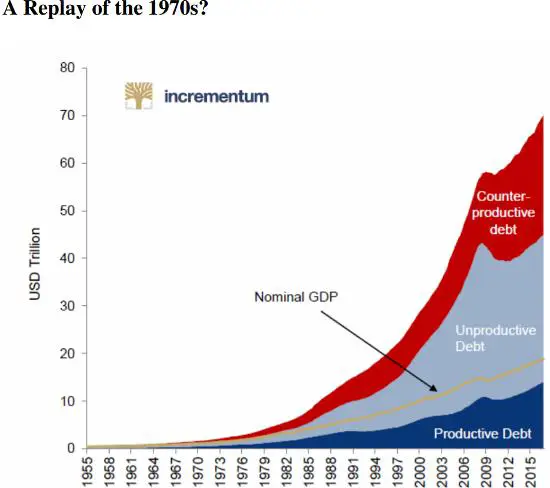

But now take a look at the exponential level of debt since the late 1970s until now and note how much faster debt is growing relative to GDP (yellow line). You dont have to be a rocket scientist to realize at some point if debt is growing exponentially and income (GDP) on at some low level of linear growth, a day of bankruptcy lies ahead. Yet with each bubble, the U.S. continues to pile more debt upon debt, and the ratio of Debt to GDP continues to grow still further.

Over time, more and more debt-based money becomes less productive and eventually counterproductive so that the more debt owed, the less income is generated. We are clearly at the counter-productive level now, not only because of mal investment that occurs with artificially low interest rates, but also because the cost of servicing the debt becomes greater and greater at the expense of productive use of capital. What happens is that income declines to such an extent that the only way debt can be serviced is one of two ways: (1) Either rates must rise to levels that reward savers, resulting in horrendous depression, necessary to set the table for long-term honest growth; or (2) Governments/central banks engage in hyperinflationary money growth that totally destroys the fabric of society and sets the stage for radical changes of government. I believe the U.S. is at such a crucial point of time now.

In the 1970s when double digit interest rates were required to dampen rising levels of inflation, the problems faced by then Chairman Volcker were kids stuff compared to the problems Jay Powell faces now. Even so, Treasury rates north of 12% were required to dampen excess consumption caused by excess government spending and a lack of monetary discipline by the Fed, which was pushed by President Nixon, much as President Trump is pushing Jay Powell now. But the Federal debt then was just a few hundred billion dollars, not $22 trillion as it is now! A mere 1% rise in interest rates now leads to $220 billion of additional government expense, without the government providing any additional services! To add to the problems of Jay Powell, the U.S. continues to spend trillions on wasteful military excursions, and aging baby boomers are now leading to a spiral of debt, taking the U.S. debt levels north of $50 trillion over the next 30 years.

But thats not all. In the past, the U.S. has gotten away with living beyond its means because foreigners like Japan and China have been willing and even eager to buy U.S. Treasuries. That began to change in earnest with the financial crisis of 2008 in no small part because of the financial injury to foreigners by dishonest U.S. bankers. Also, the rest of the world was then realizing that the U.S. Empire was expanding to the point where bankruptcy lay at some point in its not-too-distant future.

So now late in the current credit cycle, we are going to face a moment of truth. With interest rates far from anything like the double digits of the late 1970s and with a declining appetite to own U.S. Treasuries by foreigners, we are seeing rates rise rather dramatically, leading to massive volatility in stocks and the beginning of a very painful bear market in equities. At some point, history suggests that the Fed will begin to print money in whatever quantity it takes to keep the banks from going bankrupt, just as they did in 2008-09. The big question is, at what point is it obvious that the Emperor is wearing no clothes and there are no longer any takers of U.S. Treasuries, causing the Fed to print so much money so rapidly that foreigners completely abandon the dollar, leaving the Fed with no choice but to hyper-inflate?

Given the timing of the current credit cycle, we are nearing a point in time when either the Fed is somehow able to hold the dollar system together for another cycle or the system itself blows up or implodes, leading to a new global monetary regime.

In the optimistic scenario gold is likely to behave as it did after 2008, when it rose for the next four years. If my more pessimistic (but very realistic) possible outcome takes place, the dollar will be replaced as the worlds reserve currency and gold will be the only safe haven, leaving it priced at levels in terms of dollars that may be beyond the imagination of even the craziest gold bugs. Its simple math: if the dollar nears a state of worthlessness, gold rises to levels approaching infinity.