The Great Recovery Rewind: How the Federal Reserves Balance-Sheet Unwind is Unwinding Recovery

-- Published: Monday, 28 January 2019 | Print | Disqus

By: David Haggith

We are in the end time of an unprecedented era of financial expansion the greatest expansion of the worlds money supply ever attempted, expansion of the Federal Reserves vast and unchecked powers far beyond what the Fed could do before the financial crisis, and super-sizing expansion of banks that were already way too big to fail.

I am calling this time in which we are now unwinding this monetary expansion theGreat Recovery Rewindbecause I believe this attempt by the Federal Reserve and other central banks of the world to move us away from crisis banking is taking us right back into economic crisis. That is why this was the top peril listed in my Premier Post, 2019 Economic Headwinds Look Like Storm of the Century. It is more potent in possible perils than all the trade tariffs in the world.

Even the CEO of one of the Feds largest member banks says no one knows what devastating effects the Feds unwinding of its balance sheet will cause. JP Morgan Chases Jamie Dimon warned that the Feds unwind is a massive experiment as untried as thequantitative easingthat is being unwound.

QE has never been done on this scale, he said. We cannot possibly know all of the effects of itsreversal.

Jamie Dimon, the chairman and CEO of JPMorgan Chase, is one of many prominent figures in finance who warn thatthis reversal of direction could send stock prices plummeting and derail the U.S. economic expansion.I dont want to scare the public, but weve never had QE [before]. Weve never had the reversal [before]. Regulations are different. Monetary transmission is different. Governments have borrowed too much debt, and people can panic when things change .

Earlier this year, noted bond fund managerBill Gross expressed his own concernsabout the effect of this unwinding. Last yearformer Fed Chairman Alan Greenspan warned of a massive bond market bubble that will be deflated in the process .

Former U.S. Treasury Secretary Lawrence Summers says, tightening involves real dangers and needs to be carried out with great care.

According to Peter Bockvar, the chief investment officer (CIO) of Bleakley Advisory Group, I believe the market is headed for a brick wall the deeper quantitative tightening gets.

Ray Dalio, founder of hedge fund Bridgewater Associates, observes that quantitative tightening is bound to produce effects entirely opposite to those from quantitative easing, namely, higher interest rates, wider credit spreads and very volatile market conditions.

Even the Fed Prez, himself, uses language that casts the Great Recovery Rewind as experimentation:

We are looking carefully at that [the unwinds impact on interest rates], and the truth is,we dont know with any precision, Fed Chairman Jerome Powell told reporters on Wednesday . Really, no one does. You cant run experiments with one effect and not the other. Were just going to have to be watching and learning.And, frankly, we dont have to know today.

However unprecedented the Great Recovery Rewind is, some outcomes can already be readily extrapolated; and they are playing out as I thought they would.

The withering economic effects of the Great Recovery Rewind

Rising reserve risks.You may recall the Fed pumped up its member bank reserves to make us all more secure in case of runs on banks as we almost saw during the financial crisis of 2007-2009. Now, as youll see below, the reserves in the accounts of member banks have been bleeding out faster than red ink in the last days of a failing Ponzi scheme.

For those banks to drain their reserves, the Fed has to reduce its reserve requirements; so the Fed has to be involved in this great reserve flush. It may be allowing this on the basis that it believes the world is more financially secure now, so it thinks the concern about runs on banks is long gone; but we all know from the last financial crisis that the world can become financially insecure in a small window of time, while the scars from an economic crash can endure a lifetime.

This photo dated October 24th, 1929, shows a view of people rushing to a saving bank in Millbury, Massachusetts as the stock market on Wall Street crashed, sparking a run on banks that spread across the country.

Compounding US government debt.One of the side-effects of the Fed sucking money out of the global monetary system is that the Fed used to roll over its holdings in US treasuries by purchasing more at an incredibly low interest rate for the US government. The government is now forced to sell a lot more treasuries in auctions to its primary dealers (member banks in the Federal Reserve System) without the Fed backstopping that by sucking them all up.

That presses the government to either pay higher interest on its treasuries to attract new buyers or raise less money with each $1,000 bond it issues. (Say, sell a $1,000 bond for $945, instead of $950.) Either results in higher yields on government bonds. (See: BOND PRIMER: What is the difference between bond yield, bond interest, and bond price?) That accelerates the government debt vortex.

Interest impact.Heres another side effect that justifies calling this time theGreat Recovery Rewind: Because government bonds are foundational in the credit market, higher yields on government bonds result in higher interest on all kinds of things, including home mortgages and auto loans. On large items, people shop payments, so those items are now less affordable. Therefore

Housing Collapse 2.0 and Carmageddon.Rising interest is already taking us into another housing crisis and Carmageddon. Ive been writing about these as the first major industries that will get the impact of the Feds Great Recovery Rewind. (My next article will show how deeply into a new housing crisis we have already fallen, and weve all heard about the number of automobile factories closing in the US.)

I think there is an insidious way rising mortgage interest is taking down the housing market besides just making houses more expensive. While mortgage applications are down by almost half due to rising interest, an even moreinterestingdevelopment is that thepercentageof applications that are getting approved is also down by about half.

With total applications being down, youd think banks would be inclined toward approving a higher percentage of the apps they get. So, why are they approving a lower percentage from an already much smaller stack of applicants? Losing half of your applicants and then cutting the percentage of those that get accepted in half is a 75% drop in approved loans! (SeeBusiness Insiders Americans stopped buying homes in 2018, mortgage lenders are getting crushed, and an economic storm could be brewing.)

Here is what I think is happening: Banks dont usually issue loans to carry them until they are paid off. They issue them to resell them to other banks and investors. In terms of the loan resale market, loans are somewhat like bonds. In the same way that the bond you hold falls in resale value (price) when bond interest on other bonds is rising, fixed-interest loans a bank issues today will be worth less when it resells them in a month if interest rates are rising quickly. (Wholl want to buy that loan when they can buy one that pays higher interest?)

Even if a bank plans to carry the loan itself, it might think it makes more sense to wait another month or two to loan out its money at an eighth-of-a-percent more interest for the next thirty years than to loan it out now if it is certain rates will rise that much in a short time. (Or it might just want to use its money to buy and hold those risk-free government bonds now that interest is getting interesting again!)

A full rewind back into the housing market collapse that began in 2007 could be readily foreseen as an obvious effect of the Feds tightening because 1) tightening after a period of sloppy easing triggered the last collapse; and 2) one of the reasons the Fed gave for buying government treasuries was to reduce mortgage interest and other long-term interest specifically to prop the housing market back up and stimulate the economy.

This is why Ive repeatedly maintained that, when the props are pulled, well fall back into the same recession. It took total denial to believe doing the opposite would not have the opposite effect. We have seen the opposite effect happening with long-term interest ever since the Fed began its balance-sheet unwind. Falling back into the same pit by winding back what we did to get out of the pit is why I call this theGreat Recovery Rewind.

Hence, my prediction a couple years ago of a major stock market upset last January (as began in the last week of January) with a much worse one in the fall of 2018 when the Fed would hit full Recovery Rewind speed. (O.K., I also said something big would happen in the summer with stocks, and not much did,except the deFAANGing of the high-tech market that drove the bull market for a decade.) Thats why I was so certain of the timing of these stock markets major plunges turns and of the summer start of a repeat crisis in housing and automobiles that certainly materialized.

Stock drop.This brings us to another inevitable side effect of the Federal Reserves Great Recovery Rewind loss of stock values. Think about it: Another one of the main reasons the Fed eventually admitted for hoovering up government bonds was to save us from the 50% crash in stock values that happened between 2007 and 2009. It did this by taking interest so low on bonds that it pushed investors into riskier assets in order to make money. In the process, this created money in bank reserve accounts that banks could use to buy those riskier assets. That worked.

Naturally, reversing that flow would raise bond interest and correspondingly suck money back from stocks by providing safer assets that are starting to provide a profitable return again. How could it not? We witnessed that throughout 2018, seeing each major increase in the Feds Great Recovery Rewind speed immediately cause greater damage to stocks.

That is why Ive always maintained the Fed cannot unwind without crashing its fake recovery. (Fake in that its not really a recovery if the patient has to stay on artificial life support forever. Its just prolonged dying. Its only true recovery when a patient becomes capable of living on his or her own.)

How could the Federal Reserve not see its great recovery rewinding?

When the Fed merelysuggestedit would begintaperingits purchase of bonds (quantitative easing) in 2013, it created what became known as the Taper Tantrum, a full-scale financial panic that I remember well because the Fed made this surprise announcement the day after my wife and I decided not to lock in the interest rate on our pending home purchase. Over the weekend, we saw our new interest rate rocket upward; so, we locked in as fast as we could on Monday and have forever paid a little more because of what felt like the fastest rise in mortgage rates even known to humankind.

Stock prices plummeted then, too, as the 10-year treasury note soared a full 100 basis points to 3% yields. The Taper Tantrum cost a lot of people a lot of money, and that was just anannouncementmany months out that the Fed would slowlybeginto buy feweradditional treasuries, not that it would start rolling back the actual number it already held. The Fed was very careful this time to telegraph its unwound intentions more slowly and sedately.

So far, the Feds Great Recovery Rewind has certainly not been as dull as watching paint dry, as Fed Chair Janet Yellen assured us would be the case. The crisis in stocks grew so severe so quickly last fall when the Fed finally kicked its rewind up to it full projected speed that the Federal Reserve has already voiced possible capitulation to the markets fear by stating it is taking its balance-sheet unwind off of autopilot after all.

Fed Chair Jerome Powell pivoted and said the Fed will be monitoring the stock market with a more patient approach in the Feds deliberate raising of interest targets. Hes even hinted the Fed may slow or pause its balance-sheet unwind. That contradicted his own auto-pilot statement in the fall when the Fed rose to full rewind velocity. Such an abrupt about-face makes it clear the Great Recovery Rewind sure aint paint drying.

While flattening of the yield curve happens before recessions, the recessions dont occur until right after the Fed reverses policy and starts lowering interest rates again due to the problems a flat yield curve creates. With talk already of reducing rewind velocity, a move back to easing may not be far ahead.

I think the Fed actually sees the recession coming but can never say so because its mere change of a pronoun reverberates throughout markets. What would happen if it ever said it sees a recession developing? Why else would the Fed start easing if it didnt see trouble coming? By the time the Fed returns to easing, a recession is already foaming at the mouth. So, either they see it coming but lie and say they dont as Ben Burn-the-banky famously said in the summer of 2008 or they are blind in the area of their supposed expertise.

My reservations about reserves

If the Fed continues to tell banks they must hold a certain ratio in reserves-to-loans as the most liquid form of protection against runs, then liquidity is going to tighten up if reserves fall and interest rates are going to rise due to shorter supply of loans. That could also explain why banks are not approving as many loans because reservesarefalling.

It appears that the Federal Reserves member banks are buying up US treasuries with their reserves and holding them, rather than reselling them, because their excess reserves are depleting rapidly. (Remember my comment above about how banks may not be issuing as many loans if treasuries with rising rates are looking attractive because they are seen as completely safe?)

It also appears the Fedistelling banks they have to maintain that ratio:

One reason why people may have underestimated bank demand for cash to meet the new rules is that Fed supervisors have been quietly telling banks they need more of it, according to William Nelson, chief economist at The Clearing House Association, a banking industry group.

The Feds Great Recovery Rewind is reducing bank reserves as follows:

By shrinking its balance sheet, the Fed reduces the amount of reserves in the financial system, therefore lowering the amount of money banks have to lend to consumers and businesses.

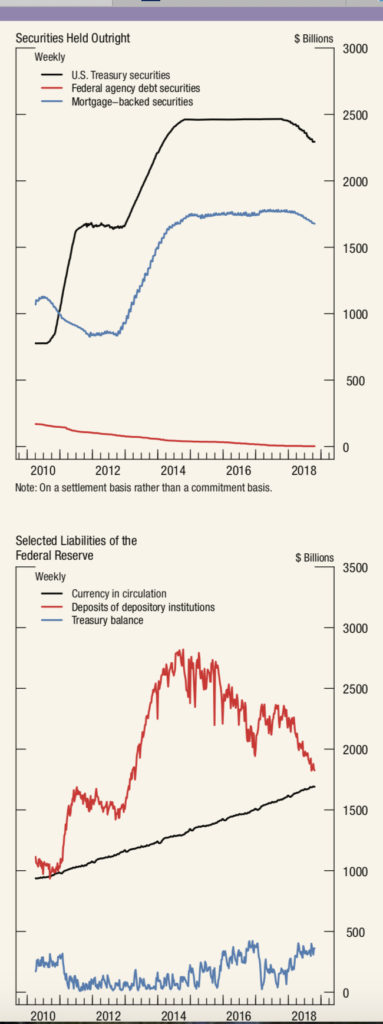

In a Premium Post that accompanies this post, I contacted the Federal Reserve and got a direct explanation of how the unwind actually draws down member bank reserves. (I was never satisfied with the answer that they are just evaporating the money, and they are not.) Even without that complex explanation, you can see how the balance sheet unwind is playing out in the following graphs from the Federal Reserve with the top graph showing the Feds own holdings and the bottom graph showing the reserves of all its member banks that are held in Federal Reserve banks:

First, the Federal Reserve stopped quantitative easing (flat part of the black and blue lines in the top graph), which meant the Fed stopped buying government treasuries (black line) and mortgage-backed securities (blue line) from its member banks, which it had been doing by creating deposits in the banks reserve accounts that they could lend against. Then you can see how, as the Fed began unwinding its balance sheet (were the black and blue lines in the top graph begin to fall), bank reserves (red line) plunged more.

Finally, you can see how bank reserves (red line in the bottom graph) have declined by almost half already during this time. Although Janet Yellen recently reminded us that correlation is not causation, I can tell you that my correspondence with a Fed economist in the Premium Post says there is direct correlation to what is happening in bank reserves.

What I cannot prove is motive, but I believe the Fed encouraged banks to start reducing their balance sheets in order to provide liquidity to the stock market and other markets during its tapering from QE and now during its final runoff of bonds. The member banks may even be holding government treasuries to protect the government from rising interest rates just as the Fed did. The consumption of bank reserves looks to me like a massive buffer for the government and the economy as trillions flow out of bank reserve accounts and into sopping up treasuries.

The Feds largest member banks are the primary dealers for Fed treasuries, which they buy in auctions. They transfer money from their reserves to the government treasury when they buy those treasuries. Now that the Federal Reserve is no longer buying those treasuries back from banks by creating new money in the banks reserves, their reserves are dropping, whether it is because the banks are choosing to hold the treasuries for the interest or because they cannot resell them all or because they are putting the money they make from selling treasuries to other uses. The bottom line is their reserves are plummeting in step with the Federal Reserves Great Recovery Rewind.

The Fed has told me it deletes money from the governments bank account as treasuries mature because the Fed is the governments banker. So, the Fed loses its treasury asset in the roll off, but it also wipes out an equal liability in the governments reserve account as its payment from the government. Thus, both sides of the Feds balance sheet come down the same amount in order for the sheet to balance. (Deposit money is considered a liability by banks because they have to give that money back upon demand.)

That, however, would not deplete the nations money supply, except that the government has to replenish its bank account (or build it up in advance of the Fed writing it down), which it does by selling new treasuries to the Feds member banks that are the governments treasury dealers. Those banks transfer money from their reserves to the governments account at the Fed to pay for their treasuries.

I suspect the member banks purchases of the new treasuries the government has to issue to replenish its funds have been the mitigating factor that has kept government bond interest from soaring during the roll-off by providing a market as ready and large as the Fed, itself. However, if they buy and hold the treasuries, it depletes their reserves, which means they have less money to loan against in the general marketplace. That would be how money exits the monetary system.

Alternately, they may buy and resell the treasuries but not put the money from their treasury sales back into their reserve accounts because they now have better investments than the interest the Fed pays them on their excess reserves (excess reserves meaning those that are above what their Liquidity Coverage Ratio is requiring of them). Either way, the money from all those treasury sales the government is making is not going back into the member banks reserve accounts.

If the banks dont soak up those treasuries by holding them as their own assets, they resell them on the open market. That would likely drive the governments financing costs up in order to find enough buyers. That can happen in the form of higher interest on the open market or a lower bond price (as described above). That would feed back through the system to what the primary dealer banks will expect in government auctions in order to assure a retail profit on the treasuries.

While I dont have all the facts about what banks are doing internally, it is obvious from the graphs above that the monetary is tightening up in direct correspondence with the termination of QE and its unwinding. We know banks are approving a smaller percentage of a smaller pile of loan applications, and we know their reserves have plummeted, which means they have less money to loan against and could easily explain why they are approving far fewer loans.

We are seeing declines in housing prices, declines in the auto industry leading to closing factories, increases in the government debt due to rising interest (in addition to the increases that happened due to declining revenue and the increases that are due to rising spending). The rise in interest that is happening due the Feds Great Recovery Rewind will also mean a decrease in stock buybacks just as the extra cash from the Trump-Tax-Cuts repatriation (a one-time occurrence in 2018) is used up so that corporations have to return funding buybacks with credit if theyre going to do them. Stock buybacks have been one of the leading drivers in the stock markets climb over the past decade. So, all of this is a complex and toxic brew of chemical reactions.

Some have opined that the Federal Reserves Great Recovery Rewind will not be as potent as its initial easing because it created new money at the rate of $80 billion a month and is only backing out of that at the rate of $50 billion a month. However, it could actually become more intense. Consider that the Fed was creating $80 billion a year when the economy was shrinking and needed a push. So, it was pushing against the drainage. Now the Fed is subtracting $50 billion a year just as the economy has started shrinking again and still needs a push. So, the unwind pulling things down with the drain.

The Fed is also tightening as global trade is tightening and as tariffs are going up, making things more expensive to consumers. Its also doing something that makes a lot of people feel unsettled, rather than something that makes them feel happier. No one is likely to enjoy unwinding as much as they enjoyed economic stimulus. The Fed is unwinding in an unforgiving environment that might be more reactive to withdrawal than a stifled economy is to stimulus.

For Premier Post Patrons who want to drill deeper into the Great Recovery Rewind, here is some deeper content that explainshow the Great Recovery Rewind works,howit impacts interest rates, andhowit may be monetizing the US government debt:

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.