The Bears Have it Right: Economy went Polar Opposite of Bullish Predictions

-- Published: Tuesday, 19 February 2019 | Print | Disqus

By: David Haggith

Bears, like myself, picked the meat off market bulls throughout 2018. We scoffed at the start of the year when bulls concocted a narrative that said bears would starve because 2018 was going to be the year of global synchronize growth. We bears bawled that this was euphoric nonsense.

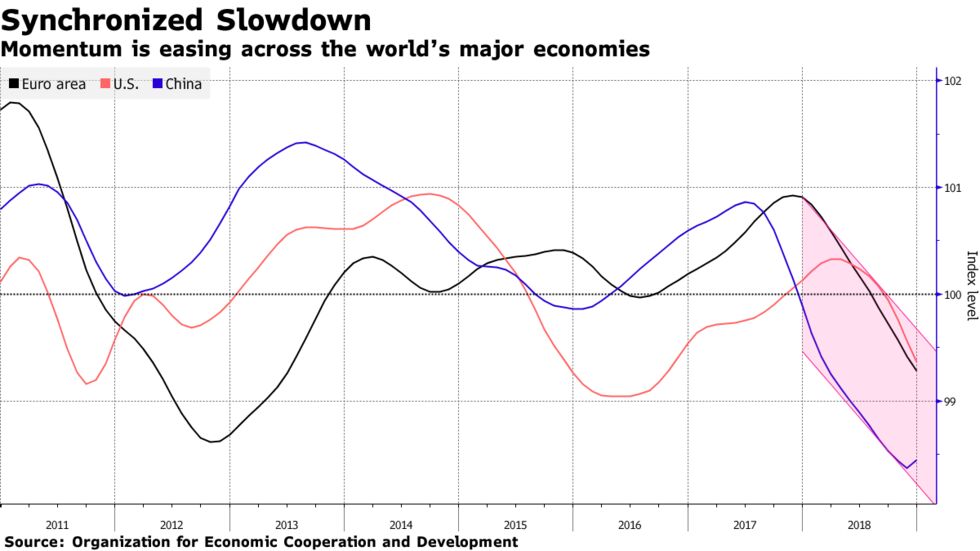

Global economies fell off a cliff as soon as the bulls narrative took hold, and all economies continued to falter for the entire year. The US was the only major economy to get a significant boost, due to absolutely massive tax cuts, which piddled away after two quarters (fourth quarter now estimated at 1.5%).

The more polar opposite from bulls the bears went, the more right they were

Im going to make my first prediction for 2019; but, first, Ill offer the following points as proof the bears were completely right for 2018:

Global cooling of all economies continued all the way into 2019, with IMF and central banks writing down their future estimates. It turned out to be the year of globally synchronized slowing. This happened largely due to the unwinding of the Feds balance sheet, and in spite of massive US tax cuts.

TheRetail Apocalypsegrew worse throughout 2018 just as bears said would be the case for the full year. Retail sales, originally reported by wishfully bulls who hoped December would finally make them right, turned out to have tanked miserably. Just like globally synchronized growth, holiday sales flopped on their head.

The bears boldly claimed 2018 would be the year ofCarmageddon. US auto sales fell so badly that 2018 became the absolutely historic year in which multiple lines of US cars were discontinued for good, and several US auto factories were permanently closed. The country that brought mass manufacturing of cars to the world practically went out of the car business, though SUVs, vans and trucks continue.

The US housing market worsened one gradient at a time every single month after the first quarter of the year. Canadian, UK, and Australian housing markets have done about the same.

Bears said (cynically to the bovine mind) nearly 100% of tax money repatriated to the US along with money from massive corporate tax breaks would go into stock buybacks, and your most polar of bears right here said, vast as those buybacks would be, they still would not save either the US economy or the US stock market from becoming a train wreck in 2018. Neither would money fleeing out of other economies into the US. Testosterone-hot Bulls thought that was ludicrous because the tax cuts were enormous. However, the Feds unwind was just as enormous, soUrsa Majorrose in ascendancythroughout the year, and Taurus fell into an icy winter. Emerging market stocks and developed markets all fell. Even the US stock market fell to pieces right at the start of the year and looked like a mess all year.

Nevertheless, a deafening chorus of bulls maintained through the year that the US stock market would end the year higher even after the October surprise (for bulls, not bears) had begun. Bears, on the other hand, held their line and predicted US stocks would end lower than at the start of the year. Bears proved resoundingly correct as the dumbfounded bulls fell silent in the nights of December.

Bears, including yours truly, had claimed throughout the decade-long recovery that the Fed would never be able to unwind its balance sheet or return to normal interest rates without crashing its fake recovery. Yours truly even said 2018 would be the year this claim proved true. Stepping up to that proof, Jerome Powell volunteered himself for aface-plantin late December, which he reinforced again this January. Having valiantly promised in September that Fed rate increases would continue apace and balance-sheet reduction would continue on autopilot, Powell reversed himself less than three months after his balance-sheet reduction hit full speed. China also moved back to massive easing, and the ECB just indicated it may return to more easing, having only just stopped easing at the end of 2018. The Bank of Japan has simply said it will continue with its quantitative easing program. Central banks appear to be scrambling to stop the wreckage their tightening has already caused.

The dialogue about synchronized growth is ancient history, replaced predominantly at the end of 2018 by talk about the possibilities of global recession starting in 2019, which is where Ive said for two years a bad 2018 will take us, and of late by talk of a Goldilocks economy that is just bad enough to re-engage the Fed in economic stimulus but not so bad as to kill the market. Good luck with the replacement narrative. It wont hold any better than globally synchronous growth did last year.

I predict we are caught in an economic polar vortex

This particular polar bear said for the past couple of years the Fed will continue tightening right into a recession because that is what it does. Though the Fed has stopped raising its target interest for interbank lending and has said itmaystop unwinding its balance sheet and, it continues unwinding its balance sheet, apparently still believing it can.

Theyield curvehas already twisted and contorted into portions that are flat or inverted. Nomuras Charlie McElligot notes that steepening of the curve after inversion is the actual point at which we have almost always gone into recessions historically. My way of putting it is that flattening of the yield curve cocks the gun; reducing interest rates again fires the gun.

My first prediction for 2019: I believe the US will go back into recessionas soon as the Fed actually reverses course on interest rates. I believe things will be generally bad enough by late spring or summer (for all the reasons I laid out in my Premium Post titled 2019 Economic Headwinds Look Like Storm of the Century) that well see the Fed actually stop QT and reverse interest rates.

However, we will already be in a recession when they do, though it will not be officially declared that the US entered recession until the end of the year or start of 2020 because recessions are only declared a monthafterGDP has receded for two straight quarters.

The first quarter of receding GDP is when therecession officially begins. In other words, data only tells us in hindsight that the economy has been receding, and often we dont know until GDP numbers get revised.

The past is prologue to the future and history rhymes

I expect the Fed to live up to its historic reputation of declaring no recession in sight even as it is standing in the middle of one. While we wont likely have any official delcaration until next year, the rest of us will feel the polar swamp wetting the seat of our pants before the Fed feels a thing.

(Bearin mind, the Fed has to keep as good a face on everything as it can because if it actually said it saw a recession coming, it would crash the stock market all over again. Its words would become a self-fulfilling prophecy because investors hang on every shade of meaning of every word the Fed chair speaks. And another market crash would take a crumbling auto, retail, housing economy down with it.)

Now bulls are back to saying the fact that market fear is gone and greed is back is good reason to believe we are on the rebound. They find a narrative for their wishes no matter what. Who you gonna trust?

Before you answer that

Consider that stock market mania throughout the past decade has been supported with a misleading narrative of rising earnings per share. As I continually pointed out, EPS was mostly rising due to stock buybacks, not due to the soaring health of corporations. We would not be seeing major retailers falling right and left for the past two years, automakers shuttering factories, Caterpillar sales constantly struggling to slow their descent, high-tech stocks crashing 40% if companies were fundamentally doing better and better.

Fundamentals were repeatedly and readily ignored as EPS rose. What we saw was historically massive buybacks reducing the number of shares in the denominator of the EPS number. Nobody cared that buybacks were the primary reason EPS was rising and were the sole financial fuel buying the rise. All that mattered was that EPS looked nominally good while buybacks were on a rampage.

However, Morgan Stanley, which was in my opinion the only major bank right about last year, now says EPS is about to bomb:

Mike Wilson, chief equity strategist at Morgan Stanley, on Monday downgraded S&P 500s earnings-per-share growth target for the year to 1% from 4.3% and warned of a looming earnings recession. Our earnings recession call is playing out even faster than we expected, said Wilson in a report. When we made our call for a greater than 50% chance of an earnings recession this year, we thought it might take a bit longer for the evidence to build . For the current quarter, U.S. companies are projected to report an earnings contraction of 4.1%, based on analysts median estimates in January. That is significantly deeper than the average 1.7% decline over the past 15 years.

The benefit of the Trump Tax Cuts was as fleeting as I figured it would be, while the exponential rise in the US national debt as a result of those cuts goes as far as the eye can possibly see. (Bears were also right that the tax cuts have failed to pay for themselves.) The pressure on bond interest is upwards, curbing the future potential for stock buybacks even as repatriated cash to fuel buybacks also starts to fade.

Many share my opinion that stock buybacks, once mostly illegal, are nothing more than obscene market manipulation:

For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserves spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.

Another way of saying that is, if you take buyback out of the historic stock market timeline, what remains would have left no growth whatsoever over the last decade. Take Fed money out of the equation as a good part of the fuel for buybacks before the tax cuts, and none of that would have happened.

Moreover, it has been reported many times, including here onThe Great Recession Blog, that corporate CEOs and executives do an inordinate amount of trading around their own buyback announcements to their own advantage.

Well, guess what, with cash spending from tax repatriation starting to fade into the rearview mirror and with interest rates rising due to the Feds balance-sheet unwind (monetary tightening) and the US government issuing a growing supply of bonds to fund its endless deficits, buybacks will be diminishing until the Fed goes back to quantitative easing and to sopping up (monetizing) the government debt.

The bears were right on the money for all of 2018, and the economic climate will remain perfect for polar bears for as long as the Fed remains on its tightening program. By the time the Fed completely figures out a few months from now that it cannot remain on its tightening program, the economy will have receded over the edge of an arctic basin.

My own writing winter has almost thawed, thanks to generous and committed readers for whom I intend to work diligently this year if we clear my goal. The thermometer is now just one mark from the goal I set as necessary in order to continue writing on the economy. Since past is prologue for reader generosity, too, Im going to venture my second prediction for 2019, which is that readers of like mind will put this fundraising thermometer over the top by the end of February so this writing does continue. How that prediction turns out is fully under your control, and Ill willingly depart the scene if I am wrong. If you prove me right, Ill stop making so many fundraising pleas and stay focused on the work of trying to beat the establishment before it beats us all.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.