A Week in the Life of a Topsy-Turvy Wildly Whirling World

-- Published: Monday, 11 March 2019 | Print | Disqus

By: David Haggith

Lets review this past devilishly whacky week to see if we can divine the way the world is turning and why the markets are churning. It was 2019s worst week in stocks and, well, just about everything economic all across this crazily spinning planet. Volatility lifted its head back out of the water like Loch Nesss monster while the citizenry took flight to treasury safe havens, bringing treasury yields down again to the five-years lowest point of the year. North Koreas Rocketman returned to his rocketry, and the Chinese threw up their hands and ran as far from Mar-a-Lago as they could or maybe they just threw up from too much chocolate cake.

The China syndrome is back

Most notably all over the world, bad news finally moved back to just being bad news, even as it arrived in cloudburst after cloudburst. Gold popped as money dropped and China flopped. Chinese exports fell 20%, outstripping the worst prediction four fold. The central bank of the billions of people of China mainlined major yuan jolts into the Xi dynastys tiring economy, and yet the Sino stock market fell off the mountain,taking a full pandabearplunge in one week.Apparently thenouveau richeChinese ghost-city dwellers are wising up to all this easing and just realized talk of more of the same as far as the eye can see simply means the economy is finished more than it means refreshed hope waits on some distant horizon.

Trump talked and China walked.The best boast Trump could biggly bluster from his tweet blaster was that the stock market would rise againifChina would only deal; China chose, instead, to cancel Chairman Xis second coming at Mar-a-Lago. Most market makers are saying the Chinese trade wars now have more downside than upside. Markets have priced in Trumps repeated wafting of wistful hopes that a deal will be struck any day. His twittering about had the lightness of ether this week. If it happens that China does sign a grand bargain, the market money is already riding on that deal, so it wont bring a lot more lift. If it doesnt happen, on the other hand, the table cloth gets pulled out from under the Mar-a-Lago gold settings, and one can only hope all the crystal doesnt shatter as Xi xings away without his chocolate cake.

Central banksters on parade

The European Central Bankjoined all other major central banks in twirling away from the tightening it had just promised and rushing back to renewed rounds of easing via mega loans to banks because it got schooled in a hurry to the awakening that it cannoteverunwind its balance sheet. It made this stunning pivot when reality forced it to admit the European economy is stalling. The ECB forecast prerecessionary growth of just 1.1% for 2019. To finish the dance, reports came in after Chairman Draghis announcement that some ECB thinksters didnt think their central bank downgraded the economy far enough!

And, so, the bank that once promised it would do anything to save the Franco-German Empire will return to doing what hasnt worked so far. As happened in China, this new round of promised profligacy was not greeted with the now customary market ecstasy. Exasperated European investors dwelled, instead, on what the ECBs flash reversal revealed about Europes economy.

And, so, the old regime returned in which bad news is just bad news. It was almost as if exhausted investors felt Central Bankster Draghis sudden ankle twist indicated central bankers are clueless since only a couple of weeks ago Draghi was boldly certain his central bank needed to torque up financial tightness. Suddenly, he and his bankster troop were break dancing on their bonnets in the streets of Belgium.

How appropriate that this carnival took place in the same week asMardi Grasin the US. Speaking of which

The Fedgoose-stepped to the same tune, singing from sea to shining sea its reiterated message that tightening is over now. Boston Fed head, Eric Rosengren, indicated the Fed is dead in its tracks, saying it could take many meetings before the Fed recaptures a sense of where this spinning economy is now going in order to figure out what to do with interest rates:

It may be several meetings of the Federal Open Market Committee before Fed policymakers have a clearer read on whether the risks are becoming reality, and by how much the economy will slow compared to last year, said Rosengren in his speech. He added that patiently watching is the best policy for now.

Notice the shift to figuring out how much the economy willslow, rather than worrying it may start to run too hot, which required full-blast quantitative tightening up until December. These guys know what theyre doing!

The St. Louis Fed head piped in that he was in favor of holding interest rates at the present level with the same focus on how things are falling apart:

Vice Chair Richard Clarida stressed cross currents and head winds are strengthening.

The Dallas Fed head harmonized with everyone else:

Substantial growth in BBB and lower-rated bonds is indicative of a weakening in corporate credit quality in the U.S . which sort of reinforces, for me, why I feel we should be taking no action for some period of time.

Fed Governor Lael Brainard and Bank of Canadas Deputy Governor Lynn Patterson also joined the chorus of CBers singing refrains of a new season of easing. Patterson said the Canadian economy looks like it will be weaker through the first half of the year than it appeared it would be in January, and the Bank of Canada toned down its convictions over future rates hikes.

So, the central choristers sang as the high-stepping Fed heads joined Draghi to spin in the streets of their financial capitals, but the citizens watched in stony silence at their odd and globally united parade. All this market hopium gave no high anywhere. Stocks did nothing but fall, fall, fall, which would seem to confirm Jerome Powells candidly stated concern last month that people are losing faith in big institutions by which he seemed to mean central banks.

Is there anyone who would ever have thought more rounds of quantitative easing would be less effective this time around because the Law of Diminishing Returns still rules? Oh, yeah, me right here all along.

Numbers fell from the sky like rain

To cap this capricious week of chaos and carnival, one of those once-a-year flukeyjobs reportscruised in under the radar at a mere 20,000 new jobs, smashing far below the lowest expectations of the gloomiest, doomiest prognostications of 150,000.

As if that were not enough rain on the parade, all hail broke loose that same day whenthe US budget deficit took a rocket ride to the moon. That is to say, it was reported that day that the US deficit vaulted into the heavens in a whopping 77% ascension in the first four months of this fiscal year another Trump triumph. He ordered the tax cuts, and he ordered the spending increases, so he gets to own it.

With the greatest revenue boosters now receding in the rear view mirror and GDP fading smaller and smaller each of the last two quarters, it doesnt look like those tax cuts will ever be paying for themselves. The Fed made that definitive by forecasting an even bigger GDP plunge this quarter to a 0.3%-0.8% lowland that makes Europe look great again. So, we can reverse the Trump Tax Cuts to restore fiscal responsibility, too, or just spend ourselves into oblivion because the interest alone is now pushing half a trillion dollars. Half a trillion here, and half a trillion there, and pretty soon youre talking real money. Dont worry, the Debt Drifters will say, Its only money; we can always print more the new money theory of thenuevo-socialistaDemocrats that Ill be attacking into in new articles soon.

With socialists rising all over the nation to preach infinite money creation Sanders, AOC, Warren, and the Fed, which socialized all the losses of the capitalists withnuevomoney and with Democrats voting to give illegal Russian aliens the right to vote in US local elections if the locals so choose (even as they decry Russian interference in US elections) and with an habitually anti-semitic congress woman in hijab now being excused by ranking (and just plain rank) Democrats for her relentless rants about Benjamin-seeking Jews, I think the world is doing awhirling dervishon its axis right now.

My country has become crazy like an asylum on parade. But, hey, the end of next week brings us into theIdes of Marchwhen all debts were settled, the Roman pantheon was worshipped and caesars were killed, ending the crisis of the Roman Republic and triggering the civil war. So, lets raise a glass of Italian whine to the fact that, even when things are this crazy, theycanget worse!

Carmageddon and the Retail Apocalypse soldiered on

General Motors mothballed one of its Ohio factories this week, and Dollar Tree announced it will be closing several hundred stores even as clothier Charlotte Russe announced closure of all of its stores with immediate liquidation of all inventory. The Gap said, during its earnings report, it will be shuttering 230 stores. Victorias Secret said it will be stripping off 53 of its North American boutiques.

Two top execs of Americas largest mall landlord, Simon Property Group, said this trend is acclerating, using phrases like I dont want to scare you and we have many more [store closures] that are in the pipeline.

And, yet, there are idiots out there who keep crowing that the good times are really on a roll now. After all, we just had a fantastic bear-market rally, now ended. How could it be better?

Let them dance over the cliff with their bankster band leaders.

Stocks couldnt stop stumbling

If youre looking for the reason stocks fell relentlessly this week, how about all the above? The quants can have their numbers; the chartsters can charter away, but reality carries the day.

TheS&P 500slipped back under its 200-day moving average. TheNasdaqnodded the same. The S&P Buyback Index, which tracks all the stocks that are rising in the S&P due to buybacks, actually fell harder than the overall index. The NasdaqFAANGsfandangled below their 200-day running average, too.

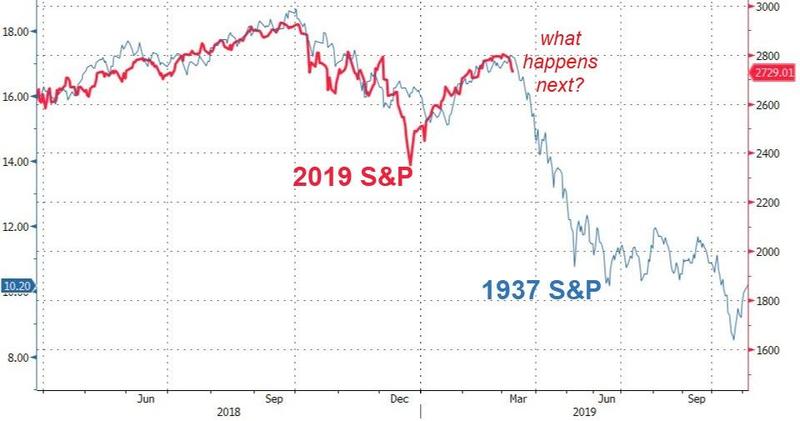

Intriguingly, perhaps ominously, the S&P continued its relentless retracing of its 1939 crash pattern:

I wouldnt make any prediction based on an eery chart coincidence, any more than Id claim Ivanka Trumps husband is the antiChrist just because his business address is666 Fifth Avenue; but its still fascinating! Especially in a world gone weird. Twain said history rhymes; today we might say it is comprised of fractals of peculiar coincidence.

The wide reality gap, however, appears to be closing:

Best-case scenario, the two lines converge in the middle at 2350 where the S&P last found its bottom.

TheDow transportation stocksmatched an ancient record of badness this past week. Their eleven-day fall paired up to their worst losing streak since Watergate. If youre a Gen X-er, you may never even have heard of that. There was this guy with a shoe-shaped nose named Nixon . Well, never mind. Suffice it to say it was a bad time far in the rearview mirror that looked well,increasingly like the present time.The fall of a president shook the nation to the core of its being.

Important to note: The Dow transports are not stocks that merely reflect how the rest of the stock market is falling. This 135-year-old index is the canary in the coal mine. The trannies, as they are lovingly referred to by gender-neutral marketeers, reflect the entire condition of the industrial world in America. The trannies go down when the closing of thousands of stores reduces shipping and when Trump Tariffs drag imports and exports down to stall speed, and when housing construction slows, which slows the movement of all kinds of materials, and when global economies start lurching like an auto out of fuel. They go down when the economy stops moving because they are the movers of all things real and not virtual, and boy have they gone down, hitting their worst path in half a century.

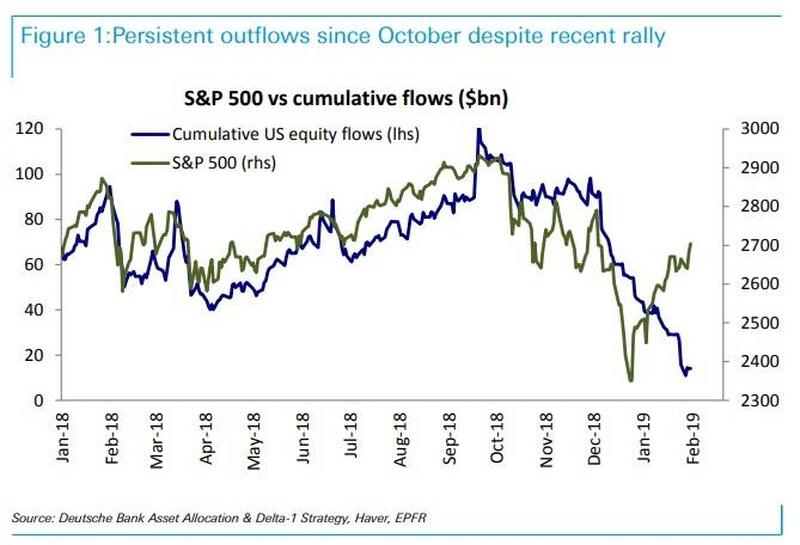

2019 also is turning out to be, inspite of all its market madness, the year of capital flight from US stocks. Well, I guess that is the mark of its madness. Yes, you heard that right. Even though stocks were bid toward their former heights throughout the first two months of the year, more money flowed out of the US market than flowed in throughout that same time. Apparently nobody with big money believes in this rising market.

Its a great paradox, but as the market punched skyward day after day, knocking holes through the clouds, nearly wiping out its major 2018 losses, investors were lightening their ships by sending their treasures on lifeboats to nearby islands. Where? I dont know; but here is a map of the journey:

Money kept leaving at the same pace, even though the market returned to rising. When the market finally reached the S&Ps triple-tested 2800 ceiling for a fourth attempt and skidded along the bottom of the ceiling to finally lose lift and drop back away, the fleeing investors proved right. Exactly how the market rose so much with so much money fleeing, I never found a good explanation for prices going up almost equal and opposite to the money going out.

But, like I said, Its a weird and whacky world.

The Big Bear rally now appears to have fallen from the lucky stars above to examine its nether regions. Each of the last three bear rallies rose to this same height, and each one dropped lower than the one that preceded it. If this one should find its rest along that trajectory of deeper bottoming bottoms, it has an exponential distance to descend that would take us back to 2014:

While the bears prey, let the bulls pray that the S&P 500s last 2400 bottom holds because the next sturdy stop for chart dwellers is between 2200 and 2100, taking out the entire Trump Rally; and below that, its no-mans land.

No, thats not a prediction, but it is where this thing could fall for the simple reason that rallies based on hopium and the euphoric high it delivers when mainlined to the moon, have very little support stops along the way back down either simple chart supportor real fundamentals especially real fundamentals. And those are my basis for saying this market has no support.

A wild and wacky whirled

When the entire world is margined into the stratosphere on corporate debt, individual credit card debt, mortgages (including millions still hunkered in from the 2008 crash) stock margin debt, delinquent student debt, sovereign debts (all in a world of rising interest), falling earnings and falling stock buybacks, you can find as much downdraft as the sinking Titanic.

Or everything could go right just like the Donald says it will! All hail the chief! Well, itcould!

Maybe this was just a week of blips, not of Freudian slips that are showing the true nature of the debt-addled economy through all the holes in the lacy veil that covers its stinking corpse. Maybe all is as golden as the Donalds showers, and China will give us a deal that makes the Trump Tariffs salutary, and the ECB will finally save the Euromess with reinforced rounds of easing, and Brexit will exit as smoothly and gracefully as the most refined Englishman can hope for, and the US stock markets last bottom will hold like a rock foundation as steady hands in the market hoist from that stronghold again the Federal flag of hope. Maybe housing will find a second wind, and the Retail Apocalypse will hit a brick-and-mortar wall that stops it from mauling all of Americas malls, and automakers will retool to produce fleets of electric dreams, turning the auto market around in just a year to a future as bright as an LED headlight. Maybe everything will go like your most golden dream.

And maybe the Beatles will regroup for a reunion from the land of the gratefully dead in a great yellow submarine piloted by a young Elton John to float across strawberry fields forever. Maybe. Maybe the world will turn a new page, this long tiresome trip to nowhere will end, and the troubles we never dealt with will just dissolve away in an opiated haze. Maybe. Its a wonderful whacky world, so anything can happen.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.