-- Published: Tuesday, 18 June 2019 | Print | Disqus

- David Haggith

The US deficit this year is already over three-quarters of a trillion dollars, putting the first eight months of the fiscal year almost equal with the entire past fiscal year. It is also $200 billion above the previous record for this portion of the year, and this Mays deficit alone was 40% higher than last Mays.

The previous deficit record was set in the middle of the last recession, which means the government is already spending more than it did to try to pull us out of the last financial crisis. In spite of all of this fiscal stimulus, the economy appears to be receding on many fronts.

The government (Donald Trump) is now routinely begging the Fed for assistance and tweeting tantrums when the Fed sits on its hands. The stock market is begging the Fed for assistance, too, and will certainly throw a tantrum of its own if none comes. All eyes are on the Fed this week, but the Fed may no longer be up to the task.

QT is QE on the QT

Ive laid out in earlier articles how the Feds member banks may already be feeling a liquidity squeeze that will force them to stop refinancing the government from their excess reserves, which are in excess no more, until the Fed restarts quantitative easing. (See Liquidity Stress Fractures Begin to Show in the Federal Reserve System.) I think that will play out next year, but for now the Fed is continuing to intentionally tighten the system.

The Fed built up those excess reserves in its member banks in order to make the banks more robust against future problems

like crops failing across the midwest because they never got planted, leaving farmers to default on loans. A graph in the above referenced article shows those excess reserves are rapidly depleting (by 50% so far), meaning banks are becoming less capable of weathering future problems.

The depleting of those member-bank reserves as the Fed continues its QT is a covert form of quantitative easing (QE) because, as the Fed draws down its balance sheet by letting bonds mature so the government has to pay them off, money is flowing out of the reserve accounts of the Feds member banks and to the government to buy up new government bonds so the government can refinance that debt and new debt for its current spending. The new-debt money that goes into the government keeps the government buying goods and services and paying employees and so stimulates the economy and becomes a major part of measured GDP, weak as it now is.

Its FedMed forever

What happens to interest on a massively and rapidly growing government debt when the second tier of lenders of last resort the Feds member banks with their easy money have spent out all their excess reserves and, so, have to stop? It seems to me you have only two choices interest on the national debt soars at that point of low liquidity when banks cannot deplete their reserves any further to soak up government debt because their depleted ability forces the government to find other creditors who are not so robust with extra cash, OR the Fed goes right back to QE and has to reverse its whole tightening regime in order to keep monetizing government debt.

The latter, of course, is the scenario Ive said for years you can bank on. The Feds recovery was unsustainable from the onset and requires ever greater amounts of QE, because QE is getting tired

really tired. Because its big numbers create shock and awe no more, the Fed gets less bang for the buck.

By September, QT will be finished, and the Fed will be back to lowering interest rates (probably staring in July). By next year it will become obvious that ending QT and cutting rates is not enough. In fact, it will be hard for the Fed to get its base rate, the Fed funds rate, down any lower than it already is without reverting to more QE; so, the Fed will have to rewind its rewind (rewind its recent attempt at balance-sheet reductions) and go right back to overt QE to keep the government from ever facing skyrocketing interest when its member-bank reserves get too tight to continue the covert QE.

That means its rinse and repeat of the last cycle, except this time FedMed wont work because weve all been here before and all know now the Fed has no end game. The Fed can never tighten again, so it is QE4-ever, which will cast a dismal pall over the already waning global economy. (Thats a teaser for next year because Im not quite ready yet to say where next year is going in any specific way, but it reveals the overall direction I think is most likely.)

Meanwhile, what could scream recession more confidently than this:

CME Groups FedWatch Tool has the odds of a rate cut by end of next month at 79.4%, 95.2% by September 2019, and then a staggering 98.6% by the end of 2019. Talk aboutconfidence that rates are indeed heading lower. JPMorgan was the first to jump the shark, changing their forecast to two rate cuts by the end of 2019, while Barclays quickly followed suit and upped the ante, changing their forecast to a stunning three rate cuts by the end of 2019. These forecast revisions are seemingly being confirmed by recent figures being released, most notably the latest US job numbers, which just missed the mark in a significant way.

Zero Hedge

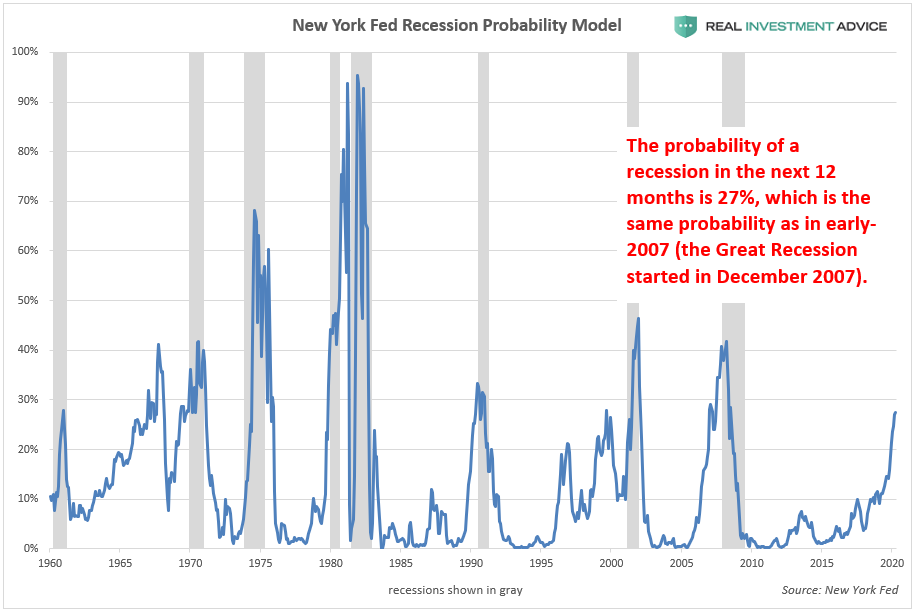

You dont start slashing rates like that (or expecting the Fed to slash rates as quickly and as often as that unless your true outlook is that you see the economy rapidly heading into recession. The last time the New York Feds yield-curve model (the difference between 10-year bonds and 3-month bills) looked as recessionary as it became this May was near the start of 2007 and we tipped into recession by the end of that same year. By the time it got to this same level in 2001, we were ALREADY IN a recession:

The end of confidence in the con game

President Trump recently denigrated the Fed as very, very disruptive because it didnt listen to him, so it raised rates too much and should not have done quantitative tightening. In a way hes right because Ive always said here that the Fed could not possibly do what the tightening it said it could, which it also said would be as boring as watching paint dry. (Of course, the real problem is that it ever did QE in the first place.)

What a bunch of stumble-bums these overtrained economic eggheads who run the Fed are according to the president. While I think he is right, I cant see how his talk does anything but create a lot less economic confidence. And the Fed, without public confidence in its confidence game, is dead. So, the presidents efforts to kill confidence in the Fed are bound to be somewhat suppressive to the Feds ability to stimulate the economy.

And the Fed knows it. In a recent Premium Post, title Teasing out the Feds Big Plan for our Future, I laid out in the Feds own candid words how concerned about declining trust in public institutions. I showed how its words really add up to its being concerned over its failing reputation because Powell kept talking about the Fed having to work hard to build and sustain the publics trust in order to retain its monetary policy independence.

That all means, if you think the good times are going to keep rolling because the Fed is coming to the rescue, think again. We are moving into deeper tariffs, diminished bank reserves, higher government interest on skyrocketing new debt as far as the eye can see at a time when we have a Fed that has been weakened by the failure of its last plan and by the president slashing away at it.

If you think the latest bad news like rising unemployment, fewer new jobs, falling GDP, diminishing corporate earnings are good news because it all means more Fed free money, rethink. The nation is more fed up with the Fed than ever and is overfed on debt. The next round of lower interest and renewed QE are nothing more than proof that FedMed failed.

Now that failure is being underscored by the president of the United States saying the US money managers are all a bunch of loser, dunderheads:

Trump told CNBCs Joe Kernen on Squawk Box. Our Fed is very, very disruptive to us

. The Fed chairman is navigating three discrete challenges: setting a policy to extend what is already a 10-year-old expansion, explaining clearly why the Fed does what it does, and ignoring the loudest public Fed badgering from a president in recent memory.

The Washington Post

Trump bemoaned the Feds unwillingness to submit to his control and tried to distance himself from the Fed, even though the people he is most upset with were his appointments:

They havent listened to me

. We have people on the Fed that really werent, you know, theyre not my people, but they certainly didnt listen to me because they made a big mistake. They raised interest rates far too fast. Thats number one. Number two, they did quantitative tightening.

Value Walk

When the president of a nation is shaking a big stick at its central bankers, claiming they are disruptive, dont take orders and have made a big mistake, that can bring the nation to a crisis of confidence in its syndicate of banksters. When the president is right in claiming their tightening failed (we all saw it happen), it makes the tightening look like a big mistake.

The real mistake, however, was all the quantitative easing that was never sustainable in the first place because it created a market that would always be dependent on continued easing, leaving us in a recovery from which we cannot recover. That was obvious from the outset, or I wouldnt have been saying for years that the present situation was where we were going to wind up.

Whether you view that situation the Donalds way (as the tightening failed) or mine (as the quantitative easing was a recovery plan from which we could never recover), the cartel of bankers clearly doesnt merit confidence. The failure is theirs to own either way. Now, when people lose confidence in their monetary system, economic collapse follows, and the president biting at the Feds heels to make sure people know where to put the blame is going to help make sure that happens.

David Haggith

| Digg This Article

-- Published: Tuesday, 18 June 2019 | E-Mail | Print | Source: GoldSeek.com