-- Published: Tuesday, 26 May 2020 | Print | Disqus

Keith Weiner, Monetary Metals

The price of gold dropped a few bucks this week, but the price of silver jumped about half a buck. The drumbeat for the gold bull market is well underway, and it is beginning now for silver. So lets do a quick update on the supply and demand fundamentals.

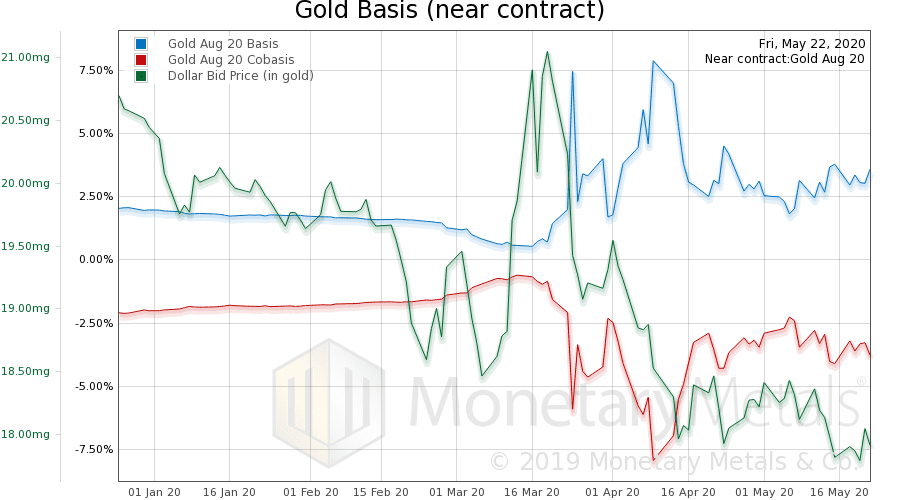

Here is the graph of the gold basis.

The basis has come in quite a bitbut it is still 3.6% annualized. We do not believe that this as a true reading. It is a sign of buying of futures, which is the opposite of scarcity of metal and the opposite of the crisis goldbugs believe is imminent. To clarify, we believe a crisis of counterparty defaults is coming, but today is not that day.

We believe this is a sign of the market makers absent from the market. Their balance sheets are in need of shrinking, and they are backing away from trades like gold carry.

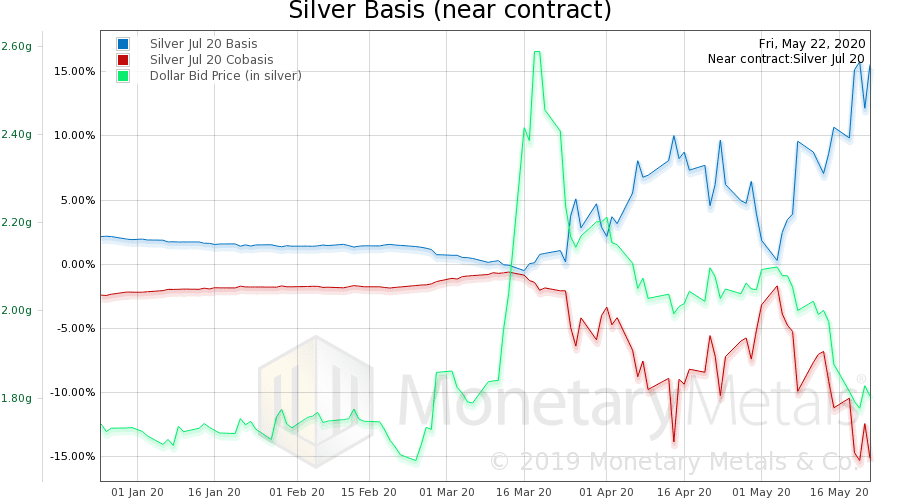

Silver is much more extreme.

The July basis is 15%! (The continuous silver basis is 7.2%, compared to 3% for gold). There is buying of silver futures, as evidenced by the jump in price. And, with market makers largely absent, the basis is pushed up.

It should not be hard for people to visualize that big buying of futures drives up the price of futures relative to the price of spot. The July contract is 47 cents higher than spot as of Friday.

As an aside, we would not heed the Monetary Metals calculated fundamental prices of gold and especially silver. The model was not designed for a market without market makers.

Capital Consumption

We have said many times that the (seemingly) endless rise of asset prices is just the process of capital consumption. It is the conversion of one partys wealth into anothers income, to be consumed. But some people ask, Arent there cases when an assets price goes up because it should go up? When it actually increases in value? Shouldnt investors have a right to sell and make a capital gain?

Yes. So lets look at the difference.

As an aside, there is always a hazard when trying to write about an important truth. Truth is contextual. Suppose you say that, water boils at 212F. Someone can respond with, Actually at the top of Mt. Everest, water boils at 161.5F. Its true, but elevation is a change of context. Everest does not show that the original statement is falseit shows the boundary of the context in which the original statement is true. Sea level.

The same applies when we say that endless bull markets cause capital consumption. The context is the global megatrend since 1981: falling interest rates. A falling interest rate also means a falling discount rate, which is how much less a dollar of earnings next year is worth today. The less the discount, the greater the present value. The greater the present value of future earnings, the higher the price of a stock, bond, or a property.

Our numerous comments over the years apply to the context of when a rise in asset prices is due to a fall in the interest rate. In this case, no more value is created. The asset should not be worth a penny more, and would not be worth more if the interest rate were stable (as in the gold standard). And therefore if more value is paid to the seller for the asset, it is at the expense of the buyers capital (or the buyers lenders capital).

Gold Investing Example

Of course, we are not against making money (though we are against the Feds perverse inventive to consume capital, and we are against zero-sum games, and we are against Ponzi schemes). Lets drill down into a case where an asset goes up in price as a result of going up in value. This is a case of gold investing, i.e. investing gold to finance the development of a gold income.

Suppose an investor buys an allocation of a Monetary Metals gold bond, which finances a mining company to get into production. And then the mining company enters production. It begins making quarterly payments. This is precisely what everyone wanted.

Of course, the bond now has lower risk than before. Therefore, its logical that market participants could value it at a higher price. One should always think of bond price and interest rate as the inverse of each other. Higher bond price means lower interest rate.

However, in this case the lower rate is not due to any voodoo of the Fed. It is due to the real reduction in risk when the miner began production and more importantly began paying.

If the price is higher, then it is logical that some of the original investors may want to sell and realize a capital gain. This is not consumption of the capital of the new investors. The new investors rightly pay more because the risk is lower. That is, they have a lower expectation of loss. Their risk-adjusted rate return may be the same as the original investors.

This example is not illustrating capital consumption, but specialization. In an advanced market economy, different investors focus on different niches. The investor who focuses on the earlier stage seeks the higher returns that come with that risk. When the risk is reduced, it is time for him to exit at a profit and deploy his limited capital into the next early stage investment. Meanwhile, other investors find it to be a good time to enter the investment once the risk is reduced.

It is rational for the price to rise as an investment goes through the stages of de-risking. And it is healthy for an investment to go through the hands of different of investors also. Price is the signal for the earlier investors to relinquish the asset to succeeding investors.

In the chronic falling interest rate and hence endless bull market of the irredeemable dollar, the distinction we highlight in this essay is obscured. The distinction between creating wealth and consuming wealth is similarly hard to see.

This is one reason why we need to move to the gold standard. Not to keep consumer prices stagnant (which is neither possible nor desirable), but because the distinction between wealth-creating and wealth-destroying enterprises is crystal clear. With a stable interest rate, asset prices change only when asset values really change.

Keith Weiner, Monetary Metals

© 2020 Monetary Metals

| Digg This Article

-- Published: Tuesday, 26 May 2020 | E-Mail | Print | Source: GoldSeek.com