-- Published: Monday, 20 July 2020 | Print | Disqus

David Haggith

Goldman Sachs, JPMorgan, and BlackRock Financial Management are stacking up wealth like never before, thanks to the Great Recession 2.0, a.k.a. the Second Great Depression. Yet, the Fed maintains its recovery plans do not create wealth disparity.

Fed-hawk Ron Paul wrote this week,

Federal Reserve Chair Jerome Powell and San Francisco Fed President Mary Daly both recently denied that the Federal Reserves policies create economic inequality. Unfortunately for Powell, Daly, and other Fed promoters, a cursory look at the Feds operations shows thatthe central bank is the leading cause of economic inequality .

When the Fed decides to pump money into the economy, it does so by putting it in the pockets of wealthy, and oftentimes politically-connected, investors who are able to spend the new money before the Feds actions result in widespread inflation.

At no time have we seen more clearly how that works than in this weeks second-quarter corporate reports from major US banks. The oligarchs are actually prospering while Rome burns.

MarketWatchreports that major banks have been hauling in more dough than bakers can even dream of.

Goldman Sucks, the vampire squid during the last financial crisis, hit the mother load, reporting a 41% rush in second-quarter revenue to $13.3 billion from a year ago. Was it because the economy isnt hurting them? No, it was hurting them (and other banks) in terms of what we might call more pedestrian or old-fashion activities like making money off mortgages and car payments.

They struck gold because their father, the Fed, knows how to print money and essentially gave lots of it to them! Much of it comes by way of a pass-through in which they use the Feds free or practically free money to help other corporations, obtaining rich fees for doing so; but some of it was just direct gains in cash from bonds they issued then sold directly to the Fed.

The Fed so thoroughly believes that all support for the average person has to come through the banks that it saved the banks before they could even start to fail. You could call that failsafe or preventative FedMed, or you could call it making sure the oligarchs in our economy get vastly wealthier while everyone else becomes poorer.

As Ron Paul said, the Fed is the leading cause of economic inequality.

How banks and their richest friends win when everyone else loses

First, there are those fees the major investment banks make by using Fed money to help other businesses in a crisis:

Cash might be king during a crisis but for top investment banks helping the Federal Reserve do whatever it takes to keep credit flowing during the pandemic,the ace in the hole has been capital markets fees.

Take JPMorgan, Chase & Co. which recorded a chart-busting $33.8 billion of revenue for the second-quarter on Tuesday, despite the coronavirus recession, and a 54% jump in investment banking fees from a year ago.

Citigroup Inc. also on Tuesday reported $19.8 billion in revenue for the second-quarter, driven in part by a 68% surge in fixed-income trading revenue anda 131% jump in investment-grade debt underwriting activityfrom a year ago.

Yet, the money is not just made off of service fees. When the Federal Reserve says it will backstop all kinds of bonds, not just government bonds, it creates a market for banks to actually print their own money. As they are losing money right now from standard loan operations, they are enabled by the Fed to make more than they ever have by essentially printing their own.

A crashing economy equals massive Fed support. When the Fed promises to buy up as many bonds as the banks will sell, what is to stop the banks from issuing their own bonds and selling them directly to the Fed for easy cash or convincing their rich customers to issue bonds at ultra-low rates that the bank promises will immediately all be purchased.

Sure, the bond is an offsetting liability when the banks issue their own, but think of what you can do by investing all the cash at the good rate you can get from the Fed, which offers to buy up all you have. Its essentially a money-printing engine, and up go stocks as you do that.

The bonds they convince customers to issue are not even a liability for the banks, as the bank can buy them all and just immediately pass them through to the Fed for a tidy markup.

The Fed plays a big part of that, because theyve really opened up the capital markets, said Stuart Plesser, a primary credit analyst for banks at S&P Global Ratings, in an interview Tuesday.

He pointed to recentbondissuancerecordsset by both U.S. investment-grade and high-yield companies during the pandemic, as examples of the ways several of the worlds largest investment banks have thrived as the Fed has offered more than $2 trillion in emergency funding facilities andmajor corporations have raced to build up war chests this year.

Get the money while its cheap, and you dont qualify for this kind of easy money unless youre very big and very rich.

The Fed isnt just soaking up existing bad debt. Its creating a market and enticing corporations to offer new bond issuances into the market the Fed is creating (as essentially the sole but certain buyer in that market). Their friends at major investment banks make nice service fees along the way.

But what is to stop the banks from being enticed into making their own bond issuances as well? Even if they are limited by the Fed in ways I dont perceive, they can certainly buy the entire bond issuance another corporation offers, knowing they have a guaranteed repurchaser in the Fed and then sell it directly to the Fed for profit.

The Fed has promised to soak up as much of this new debt as corporations, including banks I would presume, want to create. So, everyone is issuing bonds into the Feds ready vacuum cleaner. Its cheap, easy money to get at a time when the economy is losing money everywhere outside of those who know someone who knows the Fed.

It takes billions to be a player in that risk-free casino and big connections with investment bankers, or you have to be one! You and I cannot play in that game.

Who knows if corporations will ever even have to pay off those bonds at maturity? Perhaps the Fed will find a way to use the crisis to simply write off those bonds or will endlessly refi them at almost-zero interest because not doing otherwise would cause a crash down the road.

Its a great gig if you can get it!

Revenue from this activity is at its highest since five years ago. No surprise. Five years ago, the Fed was roaring along in QE3. Now they are in QE4ever in that QE3 could be stopped but not reversed. QE4ever cannot even be stopped without crashing the party.

That is how Goldman added to its Sachs of gold via massive bond trading enticed and made possible by the Fed issuing trillions to purchase bonds. That is how Goldman and its bankster pals wiped out all expectations with their corporate reports this week. After which, it gained an additional expansion of its wealth because the good news caused its stock to go up.

It is the biggest banks that make all of this money. They are the ones that are the Feds direct dealers of government bond issuances. They are the main wholesale-level financial corporations that carry out the bond issuances of all other major corporations. The little banks may be struggling, but they dont make the headlines, so who among us will ever know unless they collapse?

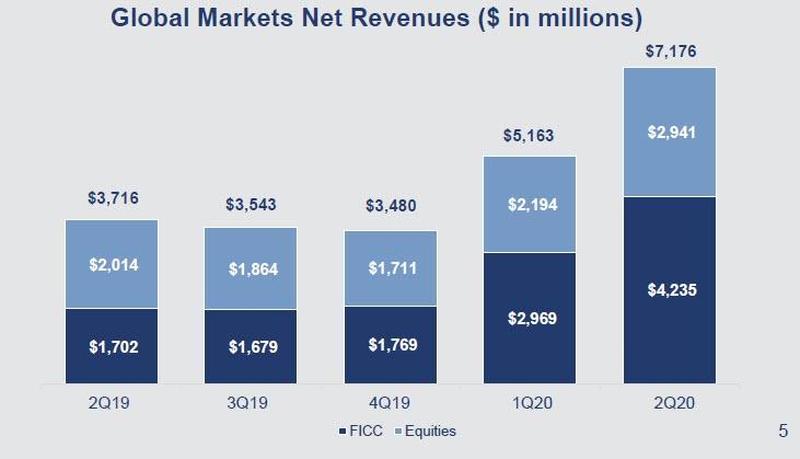

Thus, it turns out Q2 2020 was the second-best quarter on record for Goldman Sucks net revenues.How high was it? Well,one segment of their income, Global Market, was up 93% YoY.Not bad! Thats how it goes for corporations with a direct fuel line from the Fed because that is where the Feds new money directly flows.

But the Fed has nothing to do with the creation of wealth disparity. Nothing! And to think they not only say that with a straight face but that no one in the media tears their face off when they do!

If you want a picture of how good the COVID crisis has been for the biggest banks, try this image for size (of GS revenue from Fixed Income, Currency and Commodities):

If only airlines could fly so high in times like this!

The best way for a big bank to make bank is for the economy to go broke!

Once again, we see there is nothing like a major economic crisis to provide exactly the rationale the Fed needs to fire up its money-printing engines like never before! While all the new money goes into banks first, the Fed promises it will trickle down to the extremely rich who can afford to play with big stakes in bond markets and who, then, roll some of that money on into stocks for faster gains, and then it will trickle down to you an me.

Can we believe the Fed is dumb enough not to realize the rich will filter 99% of that into their own hands to prevent it from getting down to you? Please! It has never worked any other way. If you want any of it, youre going to have to fight to your death to get it.

In fact, Goldmans other side of banking in its report shows how that is working for the rest of us. Their provision for credit losses, like those of other banks that have reported this week, has soared. Thats the part where the rubber meets the road for you and me. For them, those losses are small stuff compared to their gains from Fed money printing. So, what do they care?

The Fed could require them to write off mortgages or, at least, the unpaid payments for good in order to qualify for making those ungodly gains on the other side of their balance sheets so that some help goes to the common folk. But that is unthinkable. The little people who are hurting need to struggle through and manage via what little trickles down to them by having the corporations they work for saved.

Thus, the banks that are too big to fail are made monumentally richer (again) on one side of their balance sheet while you lose your home in bankruptcy on the other side and the banks casually write off the loan for whatever they can get out of your rapidly devaluing house (or car or whatever). Its merely a small cost of doing business on the ugly side of they balance sheet as a tradeoff for the huge gains on the other side.

Alternately, you become the banks debt slave over the years ahead as you struggle to make up forbearance payments while the biggest banks do not struggle at all.

The Feds longstanding rationale is that this way you dont have to worry about the too-big bank falling on you by failing so that you lose your deposits. Well, so long as it is one of the big banks. If its a small bank that cannot play with the big boys in this Fed-direct game, it might fail, but thats OK even for you. The Fed will arrange to have those banks snarfed up by one of the big boys at fire-sale prices just like it did in the Great Financial Crisis in order to protect your deposits.

The Fedsmodus operandiASSURES us that the banks that are too big to fail will become much bigger.

Think the Fed has us covered then? Well, did it have the GFC covered before it happened to the whole world? No. It happened, didnt it? It most likely hurt you to some extent. It hurt some people to a huge extent when stocks plummeted and they lost their retirement funds. It sent companies out of business, and even some major banks (remember the name Washington Mutual?) went down for the count. (WAMU probably wasnt part of the club because it was competing outside the normal way of doing business as a thrift institution that had become bigger than investment banks.)

So, dont think this plan cannot fail. The Fed has failed many times.

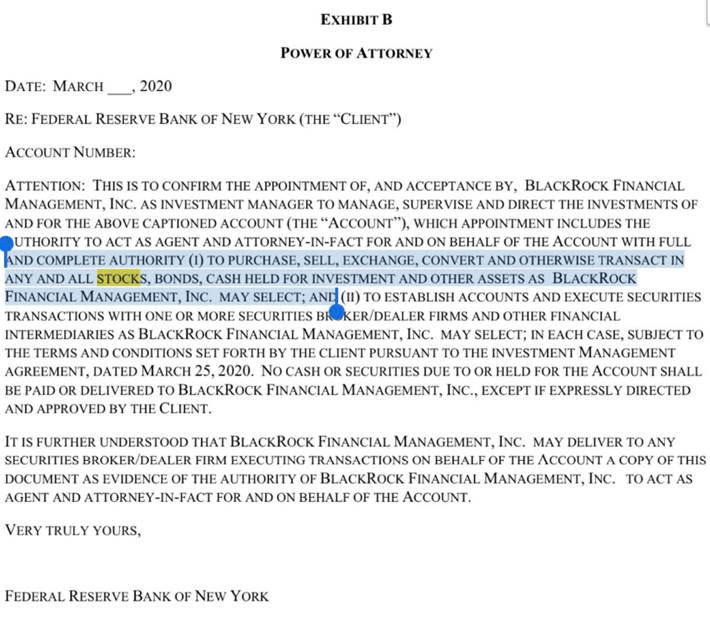

Not only is BlackRock doling out Fed funds for fantastic fees, it is also getting Fed funds to use to buy stock on the Feds behalf! The Fed doesnt want to look like it is already buying stocks because it feels the public might frown on that, so it does it through its proxy, while the mainstream media is dumb enough to completely ignore that connection as if it is a legitimate arms length operation and as if the Fed is not buying stock.

Lets take a deeper look.

The Fed is allowing BlackRock to manage, supervise, and direct the investments for the Feds account.

While Janet Yellen once said, longer term it wouldnt be a bad thing for Congress to reconsider the powers that the Fed has with respect to assets it can own, none of that matters! Its a smoke screen! A mere inconvenience to the Fed. The Fed has been using proxies to buy stocks for years.

Who can believe that, if J. Powell picks up the phone and calls one of its major member banks and says, Were going to conduct X operation, which will make you $20 billion, and we want you to invest that $20 billion in XYZ, that the bank he calls wont do exactly that? They certainly wont be the beneficiary of those free-money operations in the future if they dont!

So, it is with the blackest of corporations BlackRock.

According to the Federal Reserves website, they created a special purpose vehicle (SPV) in March 2020 managed by BlackRock to do the buying of bonds.Most people are well aware of the bond purchases that is [sic.] already happening . However, in the investment management agreement with BlackRock, most people missed the fact that the Federal Reserve also included language to allow them to transact in stocks as well.Essentially, the Fed is ready to go and buy stocks if truly needed. This is their hidden ace card.

BlackRock is the Feds sole partner for administering everything the Fed does through this particular SPV. Why would anyone think that given the power specifically stated over which BlackRock has full and COMPLETE AUTHORITY to supervise and DIRECT all investments as attorney-in-fact that BlackRock would not be using that decision-making authority already to buy all stocks as the document names first in the order of all that BlackRock may select?

Sure, theyre just sitting on that power!

Its a great gig if you can get it, but to get it, you have to know J. Powell. It probably helps if hes deeply invested in your corporation! (No apparent conflict of interest there! Im sure Powell officially stepped out of the vote after making sure he knew everyone was on board with voting the right way.) I dont want to say, Powell is just serving his self-interest here. Ill leave that for you to say (or not) based on what you see in the document.

What I do want to say is that, if you think the fact that banks were doing great in their quarterly reports this week hadanyreflection on how the economy is doing youre not thinking! And youre probably not one of my regular readers.

Unless, of course, you mean there is an inverse relationship between how well banks are doing and how the economy is doing. In which case, youre right on. The banks are doing greatbecausethe economy is doing so poorly. Theyre doing great because of their partnerships with the Fed, like this one with BlackRock, partially owned by Jerome Powell.

To know that, however, you have to read the fine print of those SPV agreements the Fed has been issuing with its agents, as in the illustration above.

You see, its not necessary for the Fed to buy stocks directly when it appoints administrators of its agencies and states outright they havefull decision-making authorityon whether to use the money in those accounts tobuy stocks!

Will the stock market crash again anyway?

Some bullish investment advisors say (in order to sell stocks or justify their own lunacy in buying them at oxygen-depriving heights), stocks always go up. With this kind of support finally fully in place, would it any wonder? Maybe they always will.

Certainly, historically, over a long enough timeframe, stocks have always gone up. However, one can just as truthfully say, stocks always crash because, over a long enough time frame, they alsoalwayscorrect to the economy. If they dont this time, it will be an historic first.

Just as the economy hasalwayscontinued to growover the longterm, so have stocks; but whenever the economy has gone down hard, so have stocks! They went down in 2018 when the Fed thought it could reverse QE. They went down this year hard! Theyre topping out again as the Fed has slowed its QE from doing all that it takes for the moment. So, to think the Fed never fails at supporting them is to deny history.

You might ask why the Fed continues slowing its money-printing engines, seeing full well that stocks started stalling as soon as that support faded (even though it is still continuing at a greater rate than any previous QE, but just much less than the burst given at the start of this economic crisis)?

The Fed has been rapidly roaring toward the limits of its promised $5 trillion in QE. It would probably like to not overshoot that $5 trillion if it can avoid it, or it wouldnt have felt a need to put that cap there in the first place.

Why does the Federal Reserve limit its promised QE? Because you cannot just increase the printing of money exponentially without eventually crashing the value of your money.

You also cannot do all the Fed is doing without creating massive economic and financial distortions that become ever harder to manage in the future. The Fed knows that by experience. It certainly saw how unable it was to back out of its last rounds of QE.

You alsocannotdo what the Fed is doing without creating greater wealth disparity, and that is problematic for the Fed in a time of utmost social unrest. That is why the Fed categorically denies, as noted at the start of this article, that it is doing that. The Fed clearly doesnt want to be blamed for creating economic disparity.

The number-one reason the market is likely to crash, in spite of the Feds support, (possibly in August, almost certainly by October) is

The Fed knows there are limits

It knows it is risking considerable problems as it pushes again into full warp drive. As captain, J. Powell can probably hear Scottie yelling, Shes gonna blow, Captain. Meaning there is risk in blowing up huge inflation.

So, yeah the Fed can do all of this, but you dont stay at Warp-factor 10 any longer than you must, even if you can. There are limits, and the Fed knows it. (And, no, Im not a Trekkie, but it seems the mostaproposanalogy.)

Others know it, too, because what is said below of the Feds partners in what should be a crime can be said of the Fed:

Opimas CEO Octavio Marenzi amusingly warned thatGoldmans almost indecent earnings may trigger a political backlash,The Fed has been able to engineer a huge bounce back in the markets by injecting trillions of dollars, benefiting investment banks primarily.This will lead to calls for the government to do more to help Main Streetrather thanWall Street.

The Fed has to be very mindful about managing the backlash that would happen if it goes too far. There is no Fed magic for preventing public outage if the economic disparity becomes too obviously the Feds own doing.

The Fed doesnt like political backlash because it threatens its free hands. It must, therefore, look disciplined and be able to argue it is only doing as much as necessaryfor the economy for everyone.

So, the Fed cannot do everything and anything it takes to prop up stocks forever if that means becoming so extreme that it will create public outcry. So far, they have adroitly steered clear of that.

One would think these close relationships with agents like BlackRock that are making landslides of money off the Fed would already be creating backlash. The Fed must be very careful not to wake the sleeping public.

The Fed now takes a rest from the warp-drive support that is absolutely essential to the market, putting the market at risk of slumping from lack of warp-factor ten support.

Please note that this recent rush of the greatest support the Fed has ever given STILL did not get the Dow or the S&P back up even to the last height they attained. And they attained that previous height with half this level of Fed support. So, diminishing returns are being seen in a big way now.

And the currently apparent market topping is happening even though the Fed is actually far from resting. It has simply dropped down to a new high cruising speed by only expanding its balance sheet, as Ive reported a couple of times, at a rate of 1.5x the rate of expansion under QE3.

Just a few years ago, two-thirds of that much financial expansion was enough to support a seemingly endless bull run. 1.5x QE3 is now just barely able to sustain the market at the level it reached under this years earlier whopping expansion of more than $3 trillion. In fact, I think it wont sustain it there for long before the Fed has to go back up to warp 10.

Its already out of control

Do you think the Fed has all of this under control? Well, as Ron Paul concluded,

In response to the government-caused economic collapse, the Federal Reserve increased the money supply by about a trillion dollars from mid-April to early June. In contrast, it took the Fed all of 2019 to grow the money supply by 921 billion dollars.Even before the lockdown, the Fed was massively intervening in the economy in a futile attempt to prevent economic crisis.

In other words, the Feds last recovery effort was already spinning so badly out of control that the Fed had to create almost a trillion dollars into the economy back in 2019 because of the stock failures of 2018. Does that sound like control? It sounds like frantic attempts to keep from losing control to me.

The Fed believed it could unwind from its recovery efforts, as it always preached it could and would (and as I always said it would fail at). It learned the hard way it cannot. It crashed its own recovery, making itself look inept.

Fed Powell averred the Fed was at risk of losing public trust. So, the Fed did increasingly more and more to prop the recovery back up through the Repo Crisis until COVID-19 gave it the excuse it needed to go thermo-nuclear into full thrust.

Is that how an organization that has it all under control operates? I dont think so. I dont think they savor the idea of looking like idiots or of losing public trust and getting, as a result, a lot of public backlash because senator and Reps start getting public pressure. They must keep the sleeping child asleep.

Now the Fed is slowing down just as COVID is speeding back up. The Fed is slowing down because it is quickly reading the limits the Fed preset for itself limits that exist because the Fed KNOWS it has to manage money supply carefully, or it will destroy the value of its product, which is money, or lose the public trust and face backlash that can potentially strip it of power.

There is no free lunch. The Fed is not limitless in how much money it can create. The Fed is not God.

Even modern monetary theory has it limits

What the Fed is doing right now is calledModern Monetary Theory creating as much money as it takes to fund the federal government and move the economy. Central Bank of India Governor and University of Chicago Professor Raghuram Rajan explained why MMT wont work because it has its limits, too.

First, his interviewer noted how widely this bad idea, fostered by Stony Brook Universitys abstract Professor Stephanie Kelton, is successfully spreading, simply because governments all over the world need her arguments to justify the money printing they need in order to accelerate into their economies back to life due to all their past profligacy that has left them with nothing for battling the Coronacrisis:

We talked aboutsustainabilityand one of the big topics in markets at least is this whole idea of QE MMT infinity, the ability of sovereigns to borrow. Now in developed countries, they have historical capital theyve built up and credibility . But youre starting to also see this idea youre starting to see more emerging market countries experiment with it, including Indonesia and several others.

Rajan, as a rare former central-bank governor who seems to get it, responded,

We know that markets can be complacent until a certain point and then they turn on a time [sic.]. We are at this point in a benign phase supported by an enormous amount of central bank liquidity emanating from the primary reserve currencies, the euro area, the US Fed and to some extent the Bank of Japan and the Bank of England.

But we must also recognize is that there are no free lunches.If theres one statement you want to keep to pound into the head of every policy maker, its that there are no free lunches.If you borrow today, there is a presumption that it will be repaired at some point, so you are in a sense taking away resources from somebody else in the future.

Now it may be a generation or two down the line will be on the hook for this whether they can pass it on to their children is an open question but youre definitely taking away their ability to borrow by borrowing today.

So the idea that there are free lunches which certainly is what the lay person takes away from MMT is very sort of attractive, seductive butits absolute nonsense .

It strikes me these guys who want to open up the government wallet and spend to protect everybody from the consequences of the pandemic dont realize thattheres one person whos bearing the hit: it may not be you, but it might be your children .

And the question is: Why dotheyhave to pay when they have no part in this?

Indeed. Why do they? Thats a moral question Ive been raising here for some time, but our generation apparently doesnt have the moral compass to care about what it is doing to its children.

However, I think we are already at the point where the next generation from all the previous decades of extreme government deficits are reaching their limit in borrowing. The next generation is the Millennial generation because we started down this path of massive deficit increases in the Reagan days.

Those days may have been nothing compared to now, but those are the days when we effectively started to say deficit be damned, we need the money now! We need our military. We need to change the world through war. Or we need our welfare! We need to save the poor now with the money of our children!

Well, those children have grown, and those who started down this path are aged and now get to face the end of the road along with their children.

Rapper Steve Mnuchin, US Treasurer at Large

Were at the point where the ever-widening spirals of debt necessary to maintain the old debt and create the new debt needed for a dying economy are swinging so wide that the Fed will have a hard time going one more circle wider without discovering the center doesnt hold this time, and centrifugal force throws everything apart.

Hold on to your common cents

You know life has taught you there is no such thing as a free lunch, and you can SEE that the Feds containment efforts are now swinging in enormous outward spirals that dont look very round anymore, requiring new inventions even by Fed standards. And you know that new inventions alway contain unknown risks.

So, believe in what your commons sense tells you. Does this look like something the Fed has under control? Or does it look like how you would expect things to look when the Fed is losing control? Do you trust these guys?

This thing is blowing up!

Consider the following:

We were already screaming toward an economic collapse, given that it took a trillion dollars in monetary expansion on the Feds balance sheet last year just to keep us in the perpetual Repo Crisis, as Ron Paul notes.

It took that much just to help the economy trundle along at a near-recessionary rate of 2% annualized GDP growth through a half year of manufacturing recession. We were, in other words,already under massive stimulusjust to sustain ourselves in a half-baked recession last year and to keep the banking crisis from blowing up.

And just remember, even though bankers are rolling in the dough like drunken bakers right now because the Fed looks out for its own first and foremost (because it is literally owned by banks), there were banks that failed under the Feds watch last time, bringing on the Great Recession; so, there will likely be banks that fail under their watch this time, too.

It is not as though the Fed has not failed spectacularly in the past! They are not gods, and sometimes, Im, not even convinced they are smart. Maybe they are, and they just dont care about the smaller banks because the big ones will snarf those up like vampire squids, but we have many times seen smaller banks fail and have seen the stock market fail this year under the Feds full and ready watch!

So, why would anyone say, The Fed has this covered; the market cant fall? The market has fallen many times under the Feds watch, and it will again.

The end of all of this could easily look like this, says Paul:

A coming crisis will likely be triggered by a collapse in the dollars value and a rejection of the dollars world reserve currency status. The economic collapse will be worse than the Great Depression. This will result in widespread violence along with government crackdowns on liberties, accelerating the US slide into authoritarianism.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.