-- Published: Thursday, 3 July 2014 | Print | Disqus

Please Note: US Markets are closed Friday for Independence Day.

| Close | Gain/Loss | On Week |

Gold | $1319.60 | -$7.30 | +0.27% |

Silver | $21.13 | -$0.03 | +0.67% |

XAU | 101.48 | +0.14% | +2.91% |

HUI | 239.71 | -0.60% | +1.33% |

GDM | 732.28 | -0.23% | +1.80% |

JSE Gold | 1483.23 | -33.98 | +2.10% |

USD | 80.22 | +0.27 | +0.25% |

Euro | 136.08 | -0.49 | -1.28% |

Yen | 97.85 | -0.40 | -0.77% |

Oil | $104.06 | -$0.42 | -1.59% |

10-Year | 2.648% | +0.020 | +4.58% |

Bond | 135.125 | -0.125 | -1.28% |

Dow | 17068.26 | +0.54% | +1.28% |

Nasdaq | 4485.92 | +0.63% | +2.0% |

S&P | 1985.44 | +0.55% | +1.25% |

The Metals:

Gold dropped $17.87 to $1309.03 just after this mornings jobs report was released, but it then bounced back higher midday and ended with a loss of just 0.55%. Silver slipped to as low as $20.81 at one point, but it then rallied back to $21.17 by late morning and ended with a loss of just 0.14%.

Euro gold fell to about 970, platinum lost $9 to $1495, and copper remained at about $3.25.

Gold and silver equities fell over 1% at the open and held near that level for most of the morning, but they then rallied back higher in the last hour of the day and ended near unchanged.

The Economy:

Report | For | Reading | Expected | Previous |

Nonfarm Payrolls | June | 288K | 210K | 224K |

Unemployment Rate | June | 6.1% | 6.3% | 6.3% |

Hourly Earnings | June | 0.2% | 0.2% | 0.2% |

Average Workweek | June | 34.5 | 34.5 | 34.5 |

Initial Claims | 6/28 | 315K | 315K | 313K |

Trade Balance | May | -$44.4B | -$45.2B | -$47.0B |

ISM Services | June | 56.0 | 56.5 | 56.3 |

The BLS net birth/death adjustment added 121,000 payrolls to Junes data. Private Payrolls rose 262,000.

All of this weeks other economic reports:

Next weeks economic highlights include JOLTS - Job Openings data and Consumer Credit on Tuesday, FOMC Minutes on Wednesday, Initial Jobless Claims and Wholesale Inventories on Thursday, and the Treasury Budget on Friday.

The Markets:

Charts Courtesy of http://finance.yahoo.com/

Oil fell on easing worries about supply after Libya reached a deal to reopen all of its previously blockaded export facilities.

The U.S. dollar index rose on better than expected jobs data that sent treasuries lower and the Dow and S&P to new record highs.

Among the big names making news in the market Friday were ADM, Lorillard, Qualcomm, and PetSmart.

The Commentary:

The ADP numbers yesterday were indeed a precursor to today's very strong payrolls number. The market was expecting a good number and that is exactly what it got - and more. Going into the report a 215K increase was the consensus - instead we got a 288K reading.

A bit later this AM, the June ISM service sector numbers came out and that also helped to confirm that strong jobs number. The employment component of that series came in at 54.4 against a 52.4 reading in May.

Stocks loved the number as the Dow rose above 17000. The S&P 500 and the Russell 2000 both moved higher as well. Any time weakness appears and it looks as if the Bears are finally going to get their day in the sun, back up these equity markets go only to set another new all-time high. It is nothing short of astonishing. Fighting the tape has been a fool's errand when it comes to these equity markets.

The VIX, or Volatility Index (I prefer to call it the Complacency Index) is flirting with levels last seen in February 2007! Amazing!

The yield on the Ten Year rose as high as 2.69%. According to one of the CME markets, the odds of a rate hike by the Fed at its June 2015 FOMC meeting rose to 57%. Yesterday the odds were 51%. Last month the odds were 43%. It is clear that the majority are coming around to the view that higher rates are in store next year. If the market becomes convinced that the Fed is going to be able to stay on top of any nascent inflationary pressures, gold is going to lose some of its current friends.

I suspect that today's strong number is going to shift more of the focus on the wages numbers coming our way in the future. Traders/investors are going to want to see some evidence of wage inflation. So far they do not seem concerned. As long as that is the case, the Fed can remain accommodative and will not be in a hurry to kick rates higher. Still, one can clearly see a subtle shift coming in regards to sentiment towards higher rates.

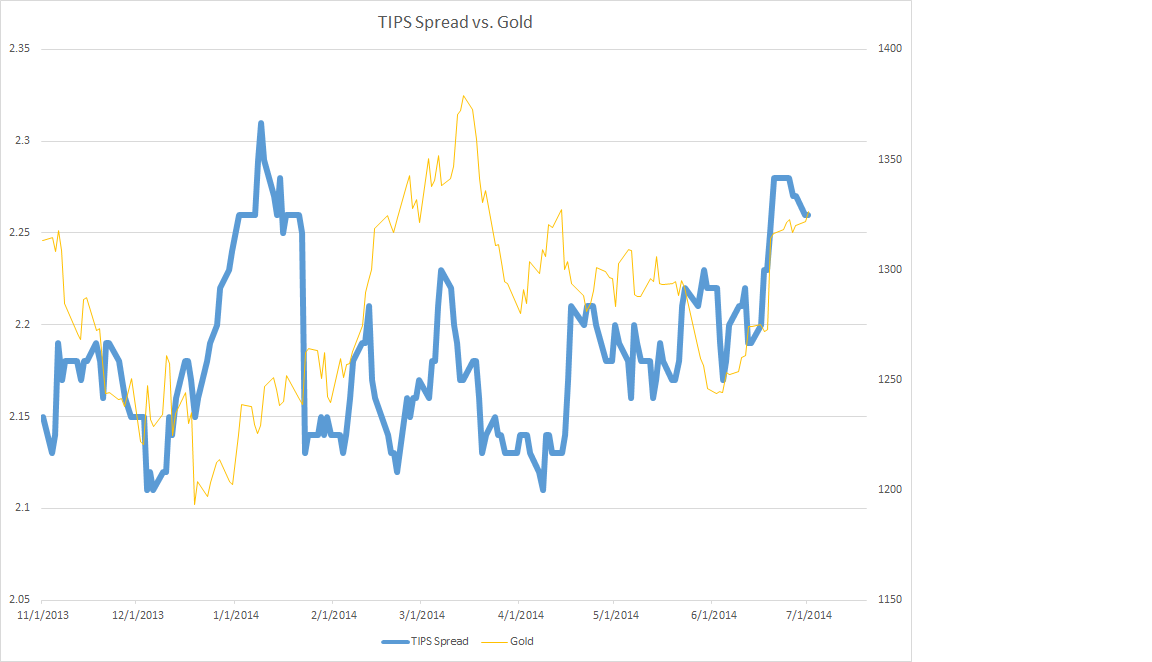

As far as gold is concerned, the metal looks as if geopolitical events in Iraq are continuing to provide some support. The stronger Dollar coming on the heels of the payrolls number, provided pressure. The lack of wage inflation did likewise. However, while the market bent, it did not break. The geopolitical premium remains. Also, while I have noticed that the TIPS spread has weakened somewhat this week, it is still up near 6 month highs.

If grain prices continue to work lower, it will be up to the energy complex to bring support to the commodity sector as far as inflationary aspects are concerned. Right now crude is continuing to weaken and has fallen down near that support zone I noted on the crude chart I put up in yesterday's post.

Coffee, sugar, cotton, soybeans, wheat and corn are all lower today - along with crude, heating oil and unleaded gasoline. Cattle are strongly higher as news hit the market after the close of pit session trading yesterday of a record $1.58 paid for cattle in the Southern Plains. I had to double check that price print as I thought I was hallucinating. WOW! Those who have cattle to sell are sitting very pretty right now. By the way, as a side note, I just picked up my brisket for my July 4th barbeque - GREAT GOOGLY MOOGLY! I wonder how it now compares to caviar as far as price per ounce? AS I have said before in many posts - there is not going to be much if any relief in sight for meat prices for the remainder of this summer. We are going to have to wait for the 4th quarter, but especially for Q1 2015 for any significant relief.

On the currency front - ECB President Draghi was out making some dovish comments once again. Those, while not the main mover in the Forex arena, certainly did nothing to soothe any Euro bulls. One gets the distinct impression, especially after today's payrolls number, that interest rates, if they are going to go up, will certainly be doing that here in the US, well before they will be over in the Eurozone. That should keep the Dollar supported at the expense of the Euro.

You can see on the chart of the long bond that prices have been falling recently and have broken the uptrend line shown. Bonds have bounced however from the support zone noted. They will need to at a bare minimum, take out that level before we can say with any degree of certainty that a serious downtrend has begun. It is too early for that right now. We will need more confirmation in the price action.

If however we begin to see a STEADY series of good payrolls numbers, along with rising wages, I fully expect this chart to break down for good. The jury is out so we wait.

Happy Independence Day (July 4th) to my American readers (and to anyone else who might be celebrating along with us). When I look at the incredible system of government given to us by our Founding Fathers, and then shift my attention to what we now have left of it, I fear my kids and grandkids are not going to be able to see anything remotely in common with it by the time they are grown. Liberty is precious precisely because it is so rare among the annals of human history. This generation seems to have forgotten that although one wonders if they ever knew it in the first place.

I will get some updated charts up later... busy morning...- Dan Norcini, More at http://www.traderdannorcini.blogspot.com/

GATA Posts:

TF Metals Report: Halftime

Reserve Bank of India apparently plans to start leasing its gold

UK regulator sees 'no clear evidence' of gold market rigging by investment banks

The Statistics:

Activity from: 7/02/2014

Gold Warehouse Stocks: | 8,298,485.371 | +402.657 |

Silver Warehouse Stocks: | 175,523,034.696 | -706,382.31 |

Global Gold ETF Holdings

[WGC Sponsored ETFs]

| Product name | Total Tonnes | Total Ounces | Total Value |

New York Stock Exchange Arca (NYSE Arca) AND Singapore Exchange (SGX) AND Tokyo Stock Exchange (TSE) AND Hong Kong Stock Exchange (HKEx) AND Mexico Stock Exchange (BMV) | SPDR® Gold Shares | 796.392 | 25,604,803 | US$33,950m |

London Stock Exchange (LSE) AND NYSE Euronext Paris AND Borsa Italiana AND Frankfurter Wertpapierbörse (Deutsche Börse - Xetra) | Gold Bullion Securities | 138.13 | 4,441,056 | US$5,852m |

London Stock Exchange (LSE) AND NYSE Euronext Paris AND Borsa Italiana AND Frankfurter Wertpapierbörse (Deutsche Börse - Xetra) AND NYSE Euronext Amsterdam | ETFS Physical Gold | 152.66 | 4,908,200 | US$8,004m |

Australian Stock Exchange (ASX) | Gold Bullion Securities | 11.16 | 358,789 | US$473m |

Johannesburg Securities Exchange (JSE) | New Gold Debentures | 42.14 | 1,354,816 | US$1,797m |

Note: No change in Total Tonnes from yesterdays data.

COMEX Gold Trust (IAU) Total Tonnes in Trust: 164.28: -0.48 change from yesterdays data.

Silver Trust (SLV) Total Tonnes in Trust: 10,038.52: -3.95 change from yesterdays data.

The Miners:

Pretivms (PVG) drill results, Lake Shores (LSG) record quarterly production, and Kirklands (KGI.TO) closed financing were among the big stories in the gold and silver mining industry making headlines Thursday.

WINNERS

1. Paramount | PZG +5.21% $1.01 |

2. Tanzanian Royalty | TRX +5.16% $2.24 |

3. Timmins Gold | TGD +4.09% $1.79 |

LOSERS

1. Solitario | XPL -4.38% $1.36 |

2. Golden Minerals | AUMN-3.51% $1.10 |

3. Avino | ASM -2.05% $2.39 |

Winners & Losers tracks NYSE and AMEX listed gold and silver mining stocks that trade over $1.

Please see Yahoos Mining/Metals News Wire for all of todays mining news.

- Chris Mullen, Gold Seeker Report

- Would you like to receive the Free Daily Gold Seeker Report in your e-mail? Click here

Additional Resources for todays Gold Seeker Report can be found:

© Gold Seeker 2014

Note: This article may be reproduced provided the article, in full, is used and mention to Gold-Seeker.com is given.

Disclosure: The owner, editor, writer and publisher and their associates are not responsible for errors or omissions. The author of this report is not a registered financial advisor. Readers should not view this material as offering investment related advice. Gold-Seeker.com has taken precautions to ensure accuracy of information provided. Information collected and presented are from what is perceived as reliable sources, but since the information source(s) are beyond Gold-Seeker.coms control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. Nothing contained herein constitutes a representation by the publisher, nor a solicitation for the purchase or sale of securities & therefore information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. Investors are advised to obtain the advice of a qualified financial & investment advisor before entering any financial transaction.

| Digg This Article

-- Published: Thursday, 3 July 2014 | E-Mail | Print | Source: GoldSeek.com

Gold Seeker Weekly Wrap-Up: Gold and Silver End Slightly Higher on the Week

Gold Seeker Weekly Wrap-Up: Gold and Silver End Slightly Higher on the Week

{kind=link}

{kind=link}