-- Published: Monday, 2 April 2018 | Print | Disqus

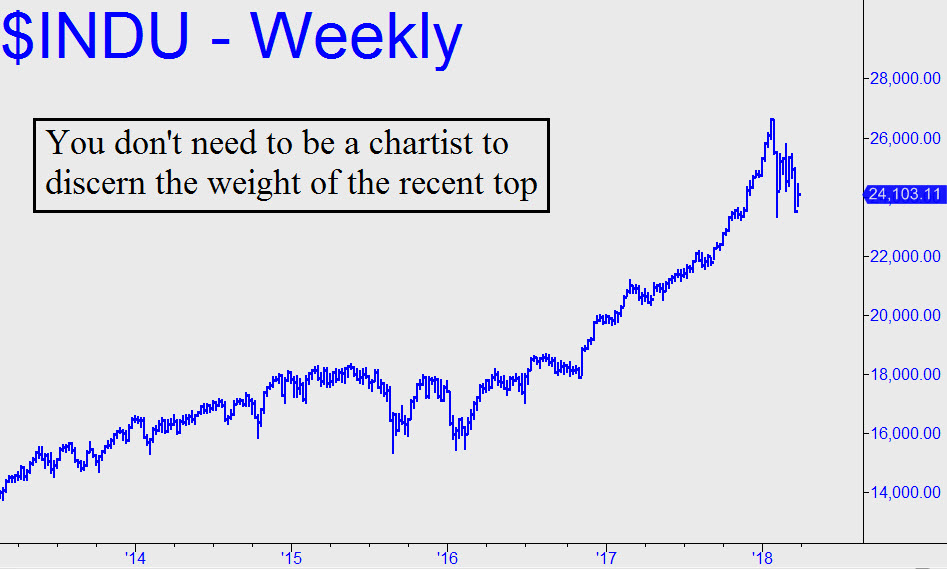

You dont have to be a chartist to discern the weight of supply sitting on the stock market right now. The steep pitch of early Februarys plunge tells us that many investors were caught completely by surprise. Although some undoubtedly expect shares to binge anew to untold highs, its possible that even more are waiting for a strong upswing that would allow an exit with less-than-stellar gains. That is the nature of the supply overhang mentioned above, and it will tend to limit the rallies. It will also exacerbate the downdrafts, with each new wave of selling persuading more and more investors to exit on the very next show of strength. Those bear rallies will come, but usually not with sufficient vigor to allow a satisfying exit by most or even many. The herd will not be quite as greedy when yet other opportunity to escape comes, but Mr. Market will anticipate this with an even more disappointing rally. This dynamic explains why bear markets most commonly turn ugly not when stocks are falling from record highs, but when rallies to lesser peaks sputter out after having failed to reach hoped-for levels.

FAANG Stocks Falter

To this sobering picture we must add a weighty accretion of negative stories that recently have turned some previous high-flying stocks leaden. The shares of Google and Facebook, to name two, have gone flaccid due to the intense scrutiny the companies are getting in the U.S. and Europe over the way they gather information about their customers and exploit it. Teslas abysmal failure to hit production targets for the highly vaunted Model 3 has called the companys very survival into question. Apples overrated smartphones, with their notorious battery problems, are finally meeting serious price resistance from consumers; and even the shares of Netflix, whose stock has soared as though everyone on the planet will eventually become a paying subscriber, have failed most recently to hit technical levels that should have been easy to attain. Moreover, all of these companies and many others will be challenged to beat earnings that at last glance reflected a perfectly-tuned economy that was hitting on all cylinders.

Despite the dark clouds on the middle horizon, there are signs the broad economy could continue humming along, keeping the stock market buoyant while ameliorating the odds of a crash. A tight job market has yet to produce any significant inflation. And the Fed, with the help of their clueless stooges in the news media, has been able to sustain the illusion that prosperity can go on for as long as the central bank desires. No one even questions why, even as the Fed purports to tighten, the supply of credit for housing, automobile purchases and leases, college tuition, stock buybacks and what-have-you has never been easier to access. (This situation will change precipitously when the yield curve finally inverts, but well save that discussion for another day.)

Why the Next Bear Market Will Be Different

A mixed bag for sure one that would not preclude a stock market rally to new highs nor, for that matter, the halving of share prices in a a relative trice. If it is the latter that occurs, or even just a pale version of it, it will unsettle Americas future like no bear market before it. Thats because Millennials and Gen-xers who continue to struggle to get on solid financial footing are about to take on nearly the entire financial burden of Baby Boomer Medicare, Social Security and public pension systems headed inexorably toward bankruptcy. That this is occurring in the very best of times is scary. It would seem less so if the stock market were to double again from current levels. However, as a practical matter, that would not mitigate the predictable outcome, only make it even more catastrophic and precipitous ultimately.

Bottom line, we owe too much collectively to pay off our debts through any mechanism other than deflation. This is a very likely outcome in my opinion, if not to say inevitable, and it is BORROWERS, not lenders, who will pay the price. Some have argued that our debts could conceivably be discharged via hyperinflation. However, this seems extremely unlikely to me, in part because debtors, including anyone with a mortgage, would skip free. There are dozens of other good reasons why we should expect the global financial disaster that lies ahead to start with an implosion i.e., a deleveraging of financial assets rather than with a hyperinflation. I have been writing on this topic for nearly 30 years and am willing to debate it any time, any place, with anyone. If you dont subscribe but want to join in the fun, click here for a two-week free trial to Ricks Picks, including access to a 24/7 chat room that draws great traders from around the world.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.