-- Posted Friday, 27 March 2009 | Digg This Article | | Source: GoldSeek.com

| | Source: GoldSeek.com

It is generally considered that the Roman Empire was at its peak around 117AD under Emperor Trajan. From there it was downhill for centuries, although not in a straight line.

Its decline can be primarily traced to three reasons: declining moral values and political civility at home; an overconfident and overextended military in foreign lands; and fiscal irresponsibility. These reasons were cited by David Walker, former Comptroller General of the United States (1998-2008) who in a speech in August 2007 warned of the similarities between Rome prior to its fall and the USA today.

Economics is often overlooked when discussing the collapse of the Roman Empire. Inflation through currency debasement was a prime reason. The emperors needed more money to maintain their armies in foreign lands and to finance the massive and growing deficit, including paying for the dole and bread and circuses so that the locals wouldnt revolt.

Of course in those days they didnt have printing presses and paper money. So, instead of coinage being allowed to maintain its intrinsic value, coins or the means of exchange became imitations of what they used to be. It is said that by the time of the Emperor Claudius II Gothicus (AD268-270) the amount of silver in a silver denarius was a mere 0.02 per cent.

The emperors seemed never to hesitate to deplete their treasury for wars, maintenance of the empire and the lavish way of life of the Roman elite. When money ran out the emperors resorted to taxation to raise the funds necessary to continue. Taxation and monetary debasement kept up the illusion that all was well. Taxes became so onerous, especially to landowners, that small landowners and free men actually sold themselves into slavery to escape taxes. Slaves did not pay taxes. This became such a significant problem that in AD368 the Emperor Valens declared it illegal to sell oneself into slavery. Thus was born the feudal serf.

Many dispute that an American Empire exists. While one may argue about it, an extensive study done by Chalmers Johnson for his book Nemesis: The Last Days of the American Republic America does have an overextended and overconfident military in foreign lands. It has an estimated 737 military bases in more than 130 countries and employs over 2.5 million people including civilians. It has 38 large or medium-sized military facilities, which is similar to the 36 that Great Britain had at its imperial top in 1898 and the 37 major bases that Rome had in 117AD.

Since 1980 the USA has been involved in some 73 military operations, including the two Gulf wars and Afghanistan. From 1950 to 1979 the USA was involved in only 26 military operations, including the Korean and Vietnam wars. (Source: Wikipedia List of United States military history events).

Today, US military expenditures total over $500 billion annually, and when combined with Homeland Security the amount spent on military and security is over $800 billion. Its military expenditures are almost equal to those of all other countries combined. But as a percentage of GDP it is today less than what it was at the height of the Vietnam War. (Source: CIA World Factbook).

What about the decline of moral values and political civility? While one may argue their merits, consider: the rise and popularity of reality and tabloid TV shows and violent entertainment (wrestling?); blockbuster movies based primarily on fictional action heroes or cartoon characters many with a violent edge; tabloid talk shows where bashing and demeaning those with opposing views are popular and some of the hosts have become very popular (Rush Limbaugh as an example); entire TV channels devoted to specific causes of the political right or left; the decline of civility in elections; the rise in blogs on the internet, many of them devoted to single issues wherein bashing and demeaning the opposition is almost seen as sport; the rise of the prison population from about 500,000 in 1980 to almost 2.5 million today, many of them for minor drug infractions, making America the most incarcerated nation in the world. Prisons are a growth industry.

America is also one of the growing minority of countries that still executes convicted criminals. In 2008 executions in America stood fourth in the world, just ahead of Pakistan but well behind Iraq, Iran and China.

That brings us to economics. Debt, debt and more debt! America is not unique in this respect. Since 1980 global debt has increased sharply. According to the Flow of Funds Accounts of the United States (a Federal Reserve publication), all debt has grown from $3,953.5 billion in 1980 to $33,517.9 billion in 2008, an incredible increase of 748 per cent. Household debt (mortgages and consumer) grew by 990 per cent. GDP by contrast grew from $2,789.5 billion to $14,264.6 billion only 411 per cent. It took $2.60 of debt to purchase $1 of GDP during the period. Each recession and economic slowdown required increasing amounts of debt to purchase an additional $1 of GDP.

America and the industrial world have over the past 30 years been built on debt, creating a vast illusion of wealth. Since the financial crisis broke in August 2007 the US has added over $2 trillion of new debt. Most of this has come from the Federal Government and domestic financial sectors (banks, etc). Indeed the domestic financial sectors have seen some of the biggest growth over the past 30 years, growing by an incredible 2,878 per cent. They are now the largest debt holders, followed by households. In 1980 they were one of the smallest sectors holding debt.

Now the government proposes adding another $3.5 trillion of debt to bail out the now bankrupt financial sector. While everyone concentrates on the $165 million (later $218 million) of bonuses being paid to AIG executives, the real scandal is the bankruptcy of the US financial sector. Admittedly they are not alone, as the British and European financial sectors are effectively bankrupt as well. We are not saying that every single financial institution is broke (Canadas are not, for example) but even if they are not, they are affected by the massive slowdown in credit flows around the world.

At the centre of the financial scandal is AIG, until recently the worlds largest insurance company. To date some $180 billion of US taxpayer money has been funneled into AIG. While the public outrage was directed at the bonuses, it should have been directed at the $180 billion bailout. In a dramatic moment at the recent hearings a US senator or congressman was questioning a very uncomfortable Treasury Secretary Timothy Geithner over the $180 billion. Just as the questioning was starting to go somewhere, Geithner was relieved that the allocated five minutes of questioning was interrupted by Chairman Barney Frank. We never saw it raised again.

So why is the $180 billion important? Why did AIG need so much in the first place? And where did the money go? Recall that prior to becoming Treasury Secretary; Geithner was president of the Federal Reserve Bank of New York. He was at the center of the AIG bailout before he became Treasury Secretary.

The Federal Reserve is a quasi-public central banking system composed of a board of governors (chairman is Ben Bernanke), the Federal Open Market Committee (FOMC), 12 regional privately-owned Federal Reserve Banks acting as fiscal agents for the US Treasury, plus numerous other private US banks. Amongst the owners of the Federal Reserve are Goldman Sachs and J P Morgan Chase financial institutions at the centre of the storm.

AIG was the worlds largest writer of credit default swaps (CDS). A CDS is a credit derivative contract between two parties. The buyer makes periodic payments to the seller and the seller receives a payoff if an underlying financial instrument defaults. CDSs are similar to insurance, but unlike insurance they need not be sold by a regulated entity.

CDS contracts are marked to market and hedge accounting may not available. Both the buyer and seller of CDSs have counterparty risk. The buyers risk is that the debt he owns (actually there is no necessity to own it) might default. The sellers risk is that he might have to honour the CDS contracts he entered into. In other words it is akin to an option where one party is the buyer of the CDS and the other (the seller) is on the hook if the buyer comes to him to exercise his CDS. All of these transactions were conducted in an unregulated over-the-counter market.

The CDS market was estimated to have a face value of $45 trillion by the end of 2007. Some said it was as large as $65 trillion. AIG as a major writer of CDS contracts had a potential risk of at least $1.6 trillion. As the expectations (according to financial models) that these contracts would ever be exercised were low, AIG did not hedge its positions, assuming that there was the capability of hedging the positions in the first place. When the market collapsed, buyers came to AIG to exercise their CDS contracts, many of which were now deep in the money. AIG could not pay; it would more than wipe out their capital. AIG, whose stock was over $100 in 2000 and with a market cap of more than $250 billion, was effectively bankrupt and its shareholders were wiped out. AIG today trades under $1. Until September 22, 2008 AIG was a component of the Dow Jones Industrials.

Enter the Federal Government, which used the US Treasury to bail out AIG and take control of AIG. But not to the extent of being able to decide whether bonuses should be paid, it seems. The bailout money was then used to flow to financial institutions such as Goldman Sachs, J P Morgan Chase, etc. A facilitator was the Federal Reserve, whose members and owners were the same banks bailed out by the payments to AIG. What is of deeper concern is that there is nothing to suggest that the bailout requirement is finished. Billions more could be required to pay off and honour the defaulted CDS contracts written by AIG.

Multiply this through the financial system and you have one gargantuan bankrupt mess. It impacts all of us, no matter where we live. The US taxpayer (and Canadians as well) will be saddled with this generational collapse for years. Indeed, as we have noted before, the credit rating of the US (and Britain) could be at risk. The CDS market itself allowed financial institutions buying CDS contracts to leverage themselves up to incredible levels, believing they had contracts protecting themselves. In the stock market an individual with a stock account is allowed to leverage himself 2:1 with a stock or 70:30 with an optionable stock. In the world of derivatives the financial institutions in many cases were leveraged 30, 40, and 50 to 1. Incredible leverage. And because these financial institutions were operating primarily in an over the counter unregulated market there was little requirement to ensure that requirements could actually be met.

And of course they paid themselves handsomely as well. Some hedge fund managers collected payouts over $500 million in a year. CEO compensation, which was about 30 or 40 times the average workers wage back in 1980, grew to almost 350 times as much in the 2000s. While middle-class wages stagnated in a world of deregulation and declining unions, the upper echelon enriched themselves beyond comprehension.

Ponzi schemer Bernie Madoff is an example. He and his family amazed a fortune of over $800 million including 4 homes New York, the Hamptons, Palm Beach and Cap dAntibes in the south of France .So where did Madoffs money go? We may never know because no one in authority and no one in the mainstream media are asking. The answers may be too embarrassing and reveal an even deeper scandal.

The pressure to get the Obama administrations $3.55 trillion budget proposal passed is immense. While we suspect there will be a great hue and cry in congress over it, ultimately it will pass with minor changes that will lop off a billion here or $10 billion there. A $3.45 trillion budget was finally passed by a congressional committee. Whether it will survive congress and the senate is another question. The budget is expected to create at least a $1.8 trillion deficit this year alone.

Also under scrutiny is the huge $1.1 trillion bank bailout program that is coming on the heels of the Federal Reserves $1.15 trillion bailout package through quantitative easing. The latter program will balloon the Federal Reserves balance sheet as they make a $300 billion purchase of longer-dated US Treasuries, plus another $750 billion of mortgage-backed securities. The Federal Reserves balance sheet has already doubled in the past year to $2 trillion. Expectations are that the balance sheet could balloon to $4 trillion or more.

Put it all together and over $12 trillion of Government money has gone or will go toward bailing out the financial institutions. This is almost 86 per cent of US GDP. While the assets to be bailed out are trading (if they are trading at all) from virtually worthless for the lowest quality paper to about 80 cents on the dollar for the highest, it amounts to a massive bailout of Wall Street. Wall Street banks want at least 60 cents on the dollar for assets that overall are worth 30 cents on the dollar or less.

Geithner and Larry Summers hope to make all of this work with another wrinkle by having private buyers for the toxic paper backed by low-interest loans from the US government for up to 97 per cent of the price they pay for these toxic assets. They dont have to repay the government until they at least break even on their three per cent risk. Then they collect most of the profits even as the US taxpayer is at risk for 97 per cent of the assets.

So why is this all so easy when there is such a hue and cry on the street against this bailout? Because from Obama on down, a huge percentage of campaign funds comes from the very Wall Street firms that are being bailed out. And we note the incestuous relationship between the Federal Reserve and the banks being bailed out. They are in effect the owners of the Federal Reserve, and many of the people in the Obama administration (and the Bush administration prior to that) are from the same Wall Street firms currently being bailed out. They are in hock to Wall Street and bailing themselves out. It is an atrocious deal for the American taxpayer as he bears the risk. The financial institutions and CEOs and others who caused the mess get bailed out and keep their bonuses.

But already the protests are mounting from both the left and the right. Taxpayer groups are outraged. Faux Boston Tea Parties have been held. There have been death threats and vandalism directed at executives of the bailed-out companies.

This outrage may also be directed at Washington. Given that there is already some growing disillusion with the Obama administration, this could tip it over the edge. In addition to the taxpayer revolts there have been growing anti-war protests as it is becoming clear that the odds of the US pulling out of its foreign wars are slim to none. We have already seen the impact of protests and social unrest in Eastern Europe, France and elsewhere in the past number of months, where there is also rising xenophobia and nationalism. It will grow in the US and quite possibly here in Canada as well. Violence is a sure byproduct.

The huge bailout plans and massive budgets are designed to jump start the US economy, get credit flows moving again and benefit the global economy as well. But the lessons of past such bailouts and prolonged periods of low interest rates are that all they create are more financial bubbles. The US Treasury market has already reacted to this as initially the bond market rallied to record high prices (record low yields), but now, despite the promise of more billions of dollars of purchases through quantitative easing, the bond market is faltering. The USs creditors are becoming nervous. Our chart of US Treasury Bonds is below.

With the potential for the US debt, already over $11 trillion (public debt $6.7 trillion, intergovernmental holdings $4.3 trillion total is 80 per cent of GDP), to grow an additional $9.3 trillion over the next decade, the question is where will all the money come from. No wonder US government debt is under review for possible downgrades.

Given quantitative easing, the US is willing to create or print money. The action is ultimately inflationary. The Federal Reserves balance sheet that has doubled to $2 trillion in the past year will soon double again and could go even higher. The remainder has to come from the markets but buyers are already beginning to balk. China, with over $700 billion of US debt, wants to diversify further. Already the Chinese are attempting to diversify through purchasing other securities or buying companies to satisfy their long-term need to ensure access to commodities and other industries.

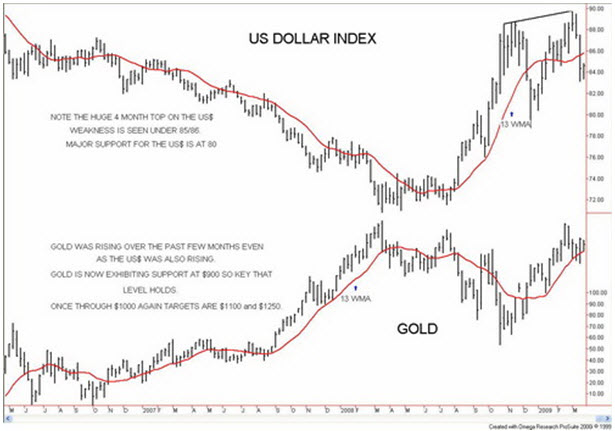

The Chinese are also joining the growing chorus that the US dollar is no longer worthy as the worlds reserve currency. Currently over 70 per cent of central banks holdings are in US debt instruments. But with growing US debt, nerves are becoming jangled. No one knows what will replace the US dollar. Baskets of currencies, IMF SDRs all are being mentioned. The UN has also joined the chorus calling for a new world currency. The US, like Britain before the Bretton Woods agreement of 1944, will not give up its reserve currency status easily. The dollar is already showing signs of going into a major decline. The other side of that is that gold has nowhere to go but up. We show charts below.

If rising quantitative easing doesnt sink the dollar, then rising protectionism will surely set off rounds of competitive currency devaluations. Around the world unemployed workers are putting enormous pressure on governments to create jobs in the home country, not buy goods from abroad to create jobs there. Protectionism is showing its ugly face with the growing dispute between Mexico and the US; Mexican trucks carrying Mexican goods into the US were blocked and the contents unloaded and loaded onto US trucks. This action was in direct violation of NAFTA. Mexico finally in retaliation put tariff increases on a host of US products. Trade wars are underway and NAFTA is at risk. The World Bank has noted that 17 of the G20 countries have become more protectionist in the past year, despite platitudes and pledges that they would not do so. The beggar-thy-neighbour policies of the 1930s are making a comeback even if no one wants to admit it.

It is a mess out there and it will get messier. With a critical mass of the worlds financial institutions bankrupt, and while many argue that bailing them out with taxpayer money is the only way to go, nobody knows how to deal with the real potential of a taxpayer revolt. These are temporary fixes at best as they are directed at solving the symptoms and starting a new bubble rather than getting to the core of the problem. They are superficial solutions, and like the illusion of debt that occurred before this collapse, the current solution is merely an attempt to recreate the illusions.

The stock market is reacting positively. How long it will last? We are struck by potential similarities with a collapse seen in 1939. We have often noted the similarities between the stock market patterns of the 1930s and those of the current decade. However, patterns are never exact and sometimes they run opposite to what occurred before.

Our chart below shows the Dow Jones Industrials in 1939-40 and 2007-09. Note an important top made on March 10, 1939. What followed was a swift collapse to lows on April 11, 1939. The current market may be replicating this but in the opposite manner. This time we note a low on March 9, 2009. We note as well the descending wedge triangle on the DJI chart that formed over the past several months. The low on March 9 at 6,440 hit the bottom of this wedge triangle. We are now breaking out over the triangle. The target is at minimum 9,000/9,200 and the next hard down trend line. A full realization of this run up could see a run to 11,000 to 11,500 and the breakdown zone of last July/August 2008. If that target was realized this would indeed be a significant rebound rally and draw a lot of people back in.

But whether this rally runs out around 9,000/9,200 or reaches its ultimate potential target of 11,000+ we emphasize that this is a corrective rally only (but one that is highly tradable).

As to the timing: while 9,000/9,200 by mid-April is very possible we would be surprised by a stampede to 11,000 in the same time period. But investors should not be under any illusions that this is the start of a new bull market. Violent rallies within the context of a longer-term bear market are not unusual. If a run like that were to occur it would be spectacular but ultimately prove to be merely a sucker rally. We continue to believe that the final lows in this bear market will not occur until at least 2012 and possibly not until 2016. Ultimate targets could be around 4,000 DJI.

The markets and the economy are in a mess. The authorities are throwing everything they can at it to try and save the financial system. But their approach is misguided; fighting a debt collapse with more debt at taxpayer expense is a plan that will ultimately fail miserably. But the rebound rally could be an opportunity to not only regain back some of the losses gleamed over the past 17 months but to raise cash and restructure, ready for the next phase of the great bear market of the first decade of the new millennium.

David Chapman is a director of Bullion Management Group Inc. the manager of the BMG BullionFund www.bmsinc.ca

Note: Charts created using Omega TradeStation. Chart data supplied by Dial Data.

Note: The opinions, estimates and projections stated are those of David Chapman as of the date hereof and are subject to change without notice. David Chapman, as a registered representative of Union Securities Ltd. makes every effort to ensure that the contents have been compiled or derived from sources believed reliable and contain information and opinions, which are accurate and complete.

Note: The information in this report is drawn from sources believed to be reliable, but the accuracy or completeness of the information is not guaranteed, nor in providing it does Union Securities Ltd. assume any responsibility or liability. Estimates and projections contained herein are Unions own or obtained from our consultants. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any securities and is intended for distribution only in those jurisdictions where Union Securities Ltd. is registered as an advisor or a dealer in securities. This research material is approved by Union Securities (International) Ltd. which is authorized and regulated by the Financial Services Authority for the conduct of investment business in the U.K. The investments or investment services, which are the subject of this research material, are not available for private customers as defined by the Financial Services Authority. Union Securities Ltd. is a controlling shareholder of Union Securities (International) Ltd. and the latter acts as an introducing broker to the former. This report is not intended for, nor should it be distributed to, any persons residing in the USA. The inventories of Union Securities Ltd., Union Securities (International) Ltd. their affiliated companies and the holdings of their respective directors and officers and companies with which they are associated have, or may have, a position or holding in, or may affect transactions in the investments concerned, or related investments. Union Securities Ltd. is a member of the Canadian Investment Protection Fund and the Investment Dealers Association of Canada. Union Securities (International) Ltd. is authorized and regulated by the Financial Services Authority of the U.K.

-- Posted Friday, 27 March 2009 | Digg This Article | Source: GoldSeek.com