-- Published: Monday, 11 March 2019 | Print | Disqus

Social Security Is Not Enough

Is That All There Is?

The Indexing Problem in Retirement Accounts

Double Problem

Cleveland, Eye Surgery, New York, and More Cleveland

I have long said I dont want to retire. I enjoy my work. Its not too physical, other than the travel (which is finally beginning to wear on me). Also, my savings are not yet sufficient to sustain the retirement lifestyle Shane and I want. I could retire now but would rather wait.

Fortunately, I have the choice of continuing to work and adding to those savings. I realize many Americans dont have that luxury. Some have to retire because of illness, or because their work requires more physical ability than their age allows. Many others dont retire because they just cant afford to.

TV commercials suggest a financial advisor is key to a leisurely retirement. A good one certainly can help, but only to the extent youve saved enough cash to give them something to invest. And as well see, many Americans havent.

My readers tend to be conscious of these things. You probably have above-average income and savings. Maybe your retirement plan is on track, but that doesnt mean you can rest easy. We all exist within a society and an economy. Its problems are ours, too, as we may find out when taxes rise to help pay for others to retire.

Today, well look at the state of retirement in America, updating some data I shared a couple of years ago. Then we will look at some strategies to keep your plan realistic and on track.

How much money will you need to retire, and how much will you have? Answering those questions is one reason a good financial advisor is worth every penny you pay them. But lets talk about some generalities.

Say you want to stop working at 65. Youre in good health and your family tends toward long lives. You expect to reach 90, having been retired for 25 years. Will Social Security alone be enough?

If you spent most of your life paying as much as legally possible into the system, and you retire in 2019 at age 65, your monthly benefit will be $2,757, which is then indexed for inflation (at least under current law). It jumps to $3,770 if you delay retirement until age 70.

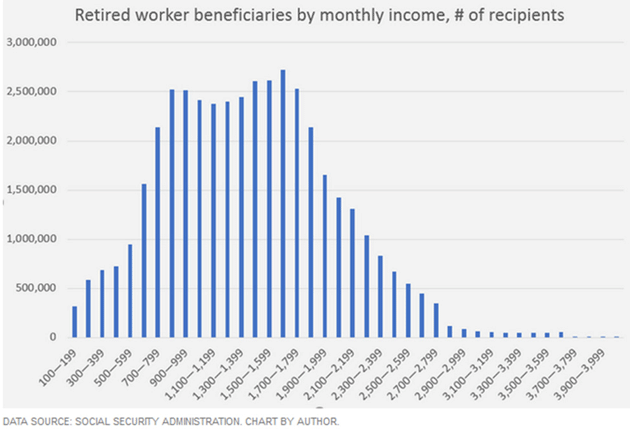

Since I am not yet 70 for another eight months, I really havent paid much attention to what I will get when I start my Social Security. I assumed like the charts that Ive seen below that it would be a couple of thousand a month. I was surprised to learn I may get significantly more. Considering how much Ive contributed over 50+ working years, its probably not that great a return. Yet most people get less. Heres the distribution.

A solid majority of Social Security recipients receive $2,000 a month or less, and many less than $1,000. The average benefit is $1,413, according to Social Securitys latest fact sheet. If thats all you have, your retirement lifestyle is not going to include many cruises and golf tournaments.

Of course, it shouldnt be all you have. Social Security was never supposed to be a complete multi-decade retirement plan. It was designed to keep retired workers out of poverty at a time when lower life expectancies kept retirement much shorter for mostif they lived to 65 at all. Now we live longer, and we have higher expectations, which political leaders have done little to dampen. Often theyve done the opposite.

Bottom line: Social Security probably wont give you much security. You need more.

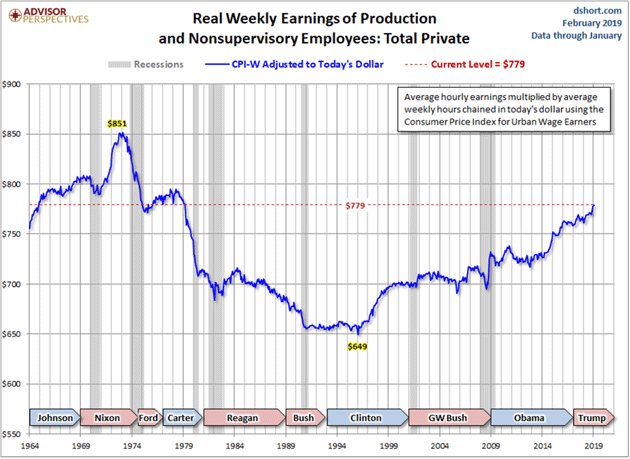

Ideally, people should avoid relying on Social Security and accumulate other savings as well. Many, perhaps most, do not. The reasons vary. I suppose some just spend their money unwisely and neglect to save anything. But income data says many Americans cant afford to both live a typical middle-class lifestyle andsave enough to finance a 20+ year retirement. Heres a Doug Short chart to illustrate.

Source: Advisor Perspectives

In constant dollars and adjusting for hours worked, average weekly earnings for non-managers are now $779, and thats an almost 40-year high. Millions of those now approaching retirement age spent their entire lives earning the equivalent of $40,000 a year, at most. Little surprise they dont have six-figure retirement savings. The simple fact of the matter is, it takes enormous discipline to save even 6% for your 401(k) at that income level.

In a country of 330+ million people, shockingly few have enough retirement savings to support the stereotypical leisurely golden years. Dennis Gartman shared some disturbing numbers last week.

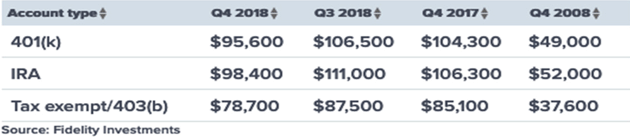

Firstly, we note that there were 133,800 millionaires late last year with sums of more than $1 million in their retirement accounts, which on its face, sounds like a large number. But that is down from 187,400 at the end of third quarter of last year, according to Fidelity Investments. According to the Federal Retirement Thrift Investment Board, which oversees TSPs, as of the end of last year, there were 21,432 millionaires compared to 34,128 at the end of September in those TSP accounts. The 4th quarter of last year was a disaster to those solely involved with equity investments; it was merely horrible for those with a more balanced investment portfolio.

But these are not really our focus this morning; our focus is that the average balance in 401(k)s, 403(b)s, or IRAs fell to $95,600 at the end of last year from $104,300 at the end of the 3rd quarter for 401(k)s, to $78,700 from $85,100 for 403(b)s and to $98,400 from $106,300 for IRA balances. It was not the drops in value that caught our attention; it is the fact that the averages are only at or near $100,000, forcing us to wonder what sort of retirement can the average retiree look forward to with this minimal sum of money set aside? Is that all there is? Really? Is that really all there is? If so, we are in very real trouble.

The average IRA balance is not necessarily indicative of retirement savings generally, as many other vehicles exist, but its probably a good proxy. And an average of around $100,000 wont yield much of a supplement to the monthly Social Security benefits described above.

I found this chart on CNBC, which also refers to the study Dennis quoted:

Many of our parents and grandparents had defined benefit plans and other guaranteed retirement benefits from the corporations they worked for. Those are increasingly an endangered species in the private sector while 401(k)s, IRAs, and Social Security arent giving the average person enough to retire on anything close to a comfortable lifestyle.

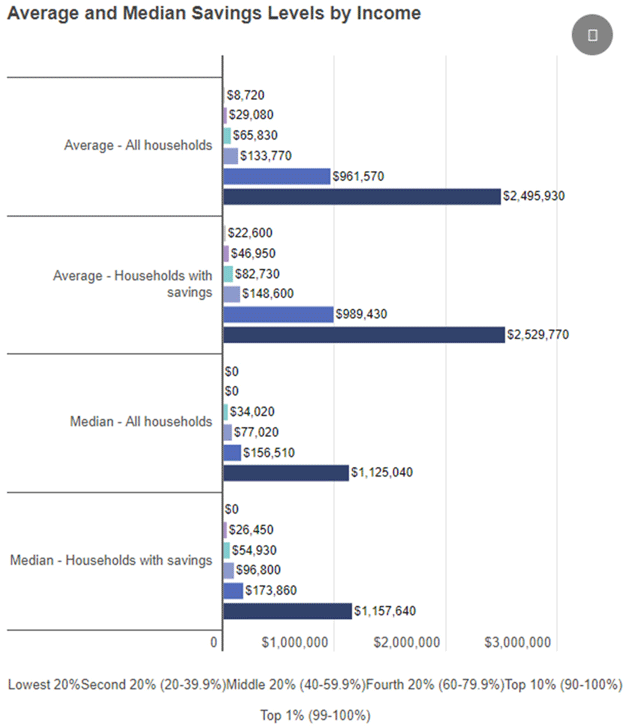

Average household savings for the bottom 40% are under $30,000. Median household savings for the bottom 40% are zero dollars. Clearly the top percentiles and especially the top 1%, skew the average. Note the bottom lines in the chart below is not the top 20%, but the top 1%. And the top 1/10 of 1%? Dont make me giggle.

Source: cnbc.com

The point is that the 80% of households have less than $100,000 in savings. That is not enough for even a minimal retirement. Lets make the very aggressive assumption that you can take 5% a year from your savings plan. If you have $100,000, thats $5,000 yearly or about $417 a monthon top of your Social Security. And if you dont have your house paid off? Or car?

Nearly every article I read on this topic talks about the fourth quarters losses, but something else leapt out at me.

Back-of-the-napkin math (and a rough napkin at that) says these retirement accounts are at least 50% invested in equity index funds. Some of you are now asking, Whats the problem? All those index funds have come back. Everybody is back to where they started.

Not so fast, Jack. As I have said until readers are probably tired of it, bear markets (which the last little bump in December barely qualifies for) that are not accompanied by a recession have V shaped recoveries. Which is exactly what we got.

Bear markets that are accompanied by recession take a very long time to recover and will likely be in the 40 to 50% loss range. A 50% loss requires a 100% gain to breakeven. That took about five years from the bottom of the last bear market.

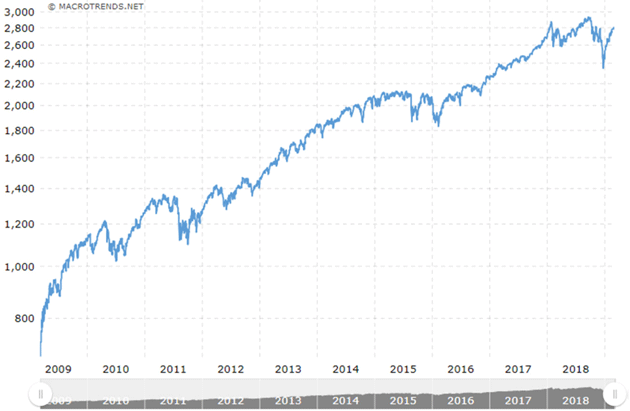

Now, lets look at the chart from the S&P 500 for the last 10 years courtesy of Macrotrends. Note that the S&P is up well over 3.5x (give or take) in the last 10 years. But the 401(k)s and IRAs did not even double. Some of that is due to investors getting out at the bottom and back in later. Some is maybe due to high bond allocations in 2009 (bond funds had done very well, and we know people chase returns). But nonetheless, retirement funds have not performed as well as you might expect.

Source: Macrotrends

Further, when that next recession and bear market hit, it will take even longer to bounce back. The recovery will be even slower than this last one. As the research Ive shared in previous letters shows, large amounts of debt slows recoveries. Very large amounts create flat economies. We are approaching large amounts in the US.

(Think what that large debt and recession did to Japan. Whats that song? Turning Japanese by The Vapors. The official 1980 video is not politically correct by 2019 standards but has some interesting historical tidbits along with the WWII propaganda silliness.)

In any event, the next recession will shortly cause a $30 trillion debt for the US government, soon to be followed by $40 trillion. Will that much debt turn us Japanese? Thats not entirely clear, since we have the worlds reserve currency and a unique role in global commerce and finance, but I think the recovery will be much slower, at a minimum. A double dip recession is clearly possible, making those stock market index fund losses even worse.

You must have some kind of strategy for dealing with market volatility. I dont know how many times I can say that. But thats the case only if you have savings to lose. Millions dont, which means they have an even harder challenge.

I speak at a variety of investment events every year. Some are for high net worth investors, but others draw a broader crowd. Lack of retirement savings, both their own accounts and those of their neighbors and the rest of the country, is by far the most common worry I hear at those events. Sometimes it verges on panic, even among people who spent decades earning good incomes and saving all they could.

The Baby Boom generation that is now reaching retirement age has a double problem. First, many of its members didnt save enough cash to support a comfortable retirement. Second, those many who did save enough could see it evaporate when we get into another bear market, which we certainly will at some point.

What can you do? Some suggestions.

First, whatever your age, save as much as you can. Stash it in your IRA, 401k, defined benefit plan, or whatever other tax-advantaged vehicles are available to you. Then save more outside them. If you look at your income and expenses and think I just cant do this, think again. Start saving something, even if its $20 or $50 a month. Get in the habit and it will become easier.

(A personal note: If you have a small business, you should at a minimum have 401(k)s and business employment retirement plans. If youre making a relatively good income, you should think about getting your own defined benefit plan. DB plans are not just for monster corporations. They can work extremely well for small, very closely held businesses. You can put away over $2 million of total contribution over your lifetime. If you start your plan and your age is 60, those can be some hefty annual contributions. Just another reason a good financial advisor can be useful.)

Second, invest in programs that give you at least a chance to dodge bear markets. Buy and hold works in theory, but not for most people because we are humans with emotions. We should recognize that and take steps to control it. As I continually say, we should invest in trading strategies and not buy-and-hold index funds in this environment. And of course, fixed income strategies like actual bonds, real estate, private credit, and so on.

Third, forget about retiring at 65 unless you are in truly dismal health (in which case, financing a long retirement is probably not your top worry). Keep working a few more years, even if you have to find a new career that better fits your circumstances. This will let your capital accumulate longer and youll get a higher Social Security benefit by waiting until 70 to start collecting.

Fourth, take care of your health. It will both reduce your medical expenses and keep you in shape so you can work and produce income longer. Further, staying physically active will keep you healthier. If that physical activity is involved in a job, that counts. There are studies that actually associate retirement with lower life and health spans. But gym time and a healthy diet are still important.

Im personally doing all of the above, and Im still concerned it wont be enough. Laugh if you want to, but that concern for me is real. Relaxing is not in my personal makeup. I know a lot of people like me. I can only imagine the panic of those less fortunate and prepared. Their problems are yours and mine, too, because an economy with so many low-income elderly people has less opportunity for everyone.

While I think socialist and progressive policies are terrifying, they are spot-on when talking about wage and income disparity. Corporate profits are at their highest level ever percentage wise, yet labor is back to Great Depression levels. That is not healthy for our society. I am not going to start singing 1930s union songs, but this is a problem we must address. It is only going to get worse and the longer we wait, the more expensive the solution is going to be. Those of us with a libertarian bent may just have to suck it up and become part of the solution.

Shane and I fly to Cleveland on Monday. I will speak to the CFA Society for lunch and then rush to the Cleveland Clinic for a bunch of exams prior to having cataract surgery on my left eye on Wednesday. Friday, we fly to New York where mortgage guru Barry Habib is taking us to an afternoon Broadway show and then dinner. Shane and I will have brunch on Sunday with Suze Orman and K.T. Both meetings are big personal thrills for both of us. Then some business meetings Monday morning and back to Cleveland to do my right eye the next week.

I am told that cataract surgery is not that big a deal for the vast majority of people, and I am going to Cleveland simply because of the quality of the surgeon (Dr. Edward Rockwood). I expect the procedures to go well and to be able to write a letter next week. But of course, things dont always work according to plan. If you get no letter from me next week, it will be because the recovery is taking a little longer.

I finish this letter at home in Puerto Rico. For whatever reason, the electricity went off here and the generator didnt immediately kick on. It turned out to be out of diesel fuel. Problem quickly fixed. Candidly, I didnt pay as much attention to the generator process as I should have. I am glad the power went out on a beautiful day rather than in a hurricane. I am being trained tomorrow to deal with it, where I will pay very close attention and then will set up regular maintenance. Just one of the pleasures of living in paradise.

Well, that and an extra two hours of flight time to get anywhere as opposed to being in Dallas. But it is worth it. Shane and I are extremely happy to be living where we are. And now after a fabulous sushi dinner with friends, we are back at the house and the electricity is on.

Have a great week. I am looking forward to having at least one eye that isnt blurry as I write the next letter, which will make it much better than simply a great week!

Your wishing I knew how to solve the retirement crisis analyst,