-- Published: Monday, 30 September 2019 | Print | Disqus

Uncertainty Principle

(Dis) Equilibrium

Insane Ideas

A Tribute to Art Cashin and New York

I often say a writer is nothing without readers. I am blessed to have some of the worlds greatest. Your feedback never fails to inspire and enlighten me.

Last weeks That Time Keynes Had a Point letter brought many more comments than usual. Apparently Keynes is still provocative 73 years after his death, no matter what you say about him. But my real point was about the twisted economic thought that is having dangerous effects on us all. And we cant blame it just on Keynes.

Today I want to share some of the feedback I received, add a few thoughts, and then show you some real-world consequences that are only getting worse. But first, let me wax philosophic for a minute.

This economic dispute is, at its core, a very old argument about how we understand reality. The ancient Greek philosopher Aristotle might agree with some of todays economists. He taught deductive reasoning with the classic syllogism:

- Therefore, Socrates is mortal

In other words, Aristotle said to move from general principles to specific conclusions. Thats what the bulk of modern macroeconomics does, using their (much more elaborate) models to deduce the best policy choices.

Centuries later, Sir Francis Bacon turned Aristotle upside down when he advocated inductive reasoning. Rather than start with broad principles and apply them everywhere, he said to presuppose nothing, observe events and move from specific to general as you gather more observations

what we now call the scientific method.

Todays economists may think thats what they are doing, but they often arent. They begin with models that purport to include all the important variables, then fit facts into the model. When the facts dont fit, they look for new ones, never considering that the model itself may be flawed.

Furthermore, as I have shown time and time again, they assume away reality in order to construct models that are in equilibrium with themselves. This is supposed to give us insight into the reality that has been assumed away.

That process isnt necessarily wrong, but its not science. It is the opposite of science. Bacon would be horrified to see this. He tried to show the world a better way and now, centuries later, some of our most learned professors still dont get it.

This is sadly not just a philosophical argument. It has real consequences for real people, including you and me.

Speaking of science, I received this note from an actual scientist (i.e., not an economist).

Dear John, having been an avid reader of your articles for many years now I wanted to write to say how much I tend to agree with your commentary, and in particular how much I enjoyed this week's article. I'd like to make a couple of comments about this week's material.

Firstly, reference was made to comparing economics with physics, and how economists suffer from "physics envy" (I should say that I have a PhD in physics from Oxford and subsequently worked as a physicist at the European Center for Nuclear Physics Research (CERN) in Geneva, Switzerland, although I left behind my career as a physicist a long time ago.)

Economies and financial markets are much more like the world of quantum mechanics than the world of classical physics. In classical physics there is complete independence between the observer and the system under observation. However, in the realms of quantum mechanics, the systems under observation are so small that the act of observation disturbs the system itself, described by Heisenberg's Uncertainty Principle.

This situation is similar to that of financial markets, where the actions of market players is not separate from market outcomes; rather the actions of market players PRODUCE the market outcomes.

Betting on financial markets is different from betting on the outcome of an independent event, such as the outcome of a horse race or a football match. The latter are akin to classical physics where there is independence between observer and observed. Whilst actions in the betting market change the odds on which horse/team is favored to win, they don't impact the outcome of the event, which is rather determined by the best horse/team on the day. Paul Shotton

Thank you, Paul, for pointing out this important distinction. I cant pretend to understand quantum mechanics but your point about independent observation is profound. Economists dont just build models; they (and all of us) are parts of the model. We are the economy and the economy is us. While discussing it, we also affect it.

George Soros calls this the principle of reflexivity, the idea that a two-way feedback loop exists in which investors' perceptions affect that environment, which in turn changes investor perceptions. (Heres his essay explaining more.)

That means these macroeconomic models, which with their Greek letters and complex equations look very scientific to a layperson, are often at odds with the scientific method. You cant conduct independent observations and experiments on an entire economy. That doesnt render the models completely useless, but greatly limits them.

Borrowing from Clint Eastwood, this might be fine if those who use these models would respect the limitations. All too often, they dont. And this is where it gets a little complicated. I confess that I use models. I build them and work with others who build even better ones. Models can help inform us of potential outcomes and better understand risk and reward, but there are clearly inherent limitations on using historical or theoretical observations to predict future results.

Here are a couple more letters, taking issue with my comments on equilibrium.

Just to clarify

Even if the economy can be modeled in some sense by a sand pile that will ultimately collapse, that does not mean that the economy is, at any point in time, not in equilibrium. In fact, it must be in equilibrium in order to form the sand pile! You could argue that the equilibrium is unstable, perhaps, but it is certainly a (possibly unstable) equilibrium. John Bruch

***

John, Ive been a reader for years and love your letter. But your comment today is over the top; The entire premise of equilibrium economics is false. Efficient market hypothesis is over the top but the premise of equilibrium is perfectly modeled in your sand pile letter. Cycles have always existed and always will exist.

Natural market forces will always move markets towards equilibrium but government interference slows the process making the sand pile grow in size and magnitude. To say that the principle of equilibrium is false is just ignoring reality.

The economy is like our forests. When a fire starts in the forest you let it burn so that natures cycle can run its course. If you keep putting out the fire you build excess fuel and then at some point you have a catastrophic fire that no humans can control. Mother Nature eventually steps in and puts out the fire and puts life back into equilibrium.

I agree that we need to rethink economics. But the principle of equilibrium, however short lived that moment in time is, is a sure reality. Dennis Carver

John and Dennis raise an interesting question. The mere fact that the sand pile exists intact for some period of time means that equilibrium exists for that interval. Fair enough. The grains of sand do, in fact, line up so that they dont collapse.

But we are constantly adding more sand and each additional grain changes the equilibrium. The previous equilibrium ends at that point, having been so brief as to be meaningless.

Eventually a grain of sand will create an unstable equilibrium, causing the pile to partially or completely collapse (and then be in equilibrium once again). So if no single state of equilibrium can exist for more than an instant, I would argue its not really equilibrium for any practical purpose. We cant rely on it to continue. Every moment brings a new, unknown situation.

Lets look at it another way. The sandpile model assumes there will be moments of instability. In economic terms, we are experiencing transitory equilibrium. The sandpile model is inherently unstable, a perfect example of Minskys Financial Instability Hypothesis: Stability leads to instability and the longer the period of stability, the greater the instability will be at the end.

(Nassim Talebs Antifragility Principle is important to understand when we think about equilibrium, or rather the lack of it. His book Antifragile is important and you should at least read the first half.)

My old friend and early economics mentor Dr. Gary North sees this idea of equilibrium as not just wrong, but downright evil.

In his 1963 textbook for upper division economics students, [Israel] Kirzner wrote about the assumptions of economists regarding the use of equilibrium as an explanatory model. They use it to describe the system of feedback that the price system provides the market place. The state of equilibrium should be looked upon as an imaginary situation where there is a complete dovetailing of the decisions made by all the participating individuals.

This means not only perfect knowledge of available economic opportunities, but also mens universal willingness to cooperate with each other. In short, it conceives of men as angels in heaven, with fallen angels having conveniently departed for hell and its constant disequilibrium, where totalitarian central power is needed to co-ordinate their efforts. A market that is not in equilibrium should be looked upon as reflecting a discordancy between the various decisions being made.

The heart of free market economic analysis is the concept of monetary profits and losses as feedback devices that persuade people to cooperate with each other in order to increase their wealth. But the theorist knows that the very fact of disequilibrium itself sets into motion forces that tend to bring about equilibrium (with respect to current market attitudes) (Market Theory and the Price System, p. 23). Presumably, even devils cooperate on this basis. They, too, prefer profits to losses.

Biblically speaking, this theory of equilibrium is wrong. It is not just wrong; it is evil. It adopts the idea of man as God as its foremost conceptual tool to explain peoples economic behavior. It explains the market process as mans move in the direction of divinity. Economists are not content to explain the price system as a useful arrangement that rewards people with accurate knowledge who voluntary cooperate with each other. They explain the economic progress of man and the improvement of mans knowledge as a pathway to divinity, however hypothetical. The science of economics in its humanist framework rests on the divinization of man as a conceptual ideal.

Setting aside the theology, the point here is that economists assume human beings are perfectly rational and consistent, or at least wish to be. Thats what makes equilibrium possible. But we know humans arent perfect or consistent. So how can we have equilibrium? We cant, unless we assume markets are in equilibrium because they act in a manner we deem appropriate or ideal.

Again, this isnt an academic argument. People who believe these ideas either hold seats of power or have influence on those who do. They truly think they can twist some knobs on their models and make everything better. If we just had better monetary or fiscal policy, if the government could tax the right people and distribute the money correctly, everyone would be so much better off. And of course, their highly complex models and theories will conveniently lead to their desired political conclusions.

It is increasingly obvious that conventional monetary policy is useless now that rates have been so low for so long, and everyone believes they will remain low. Nothing the central banks do incentivizes anyone to make immediate growth-generating decisions. If you need to borrow money, you likely did it long ago.

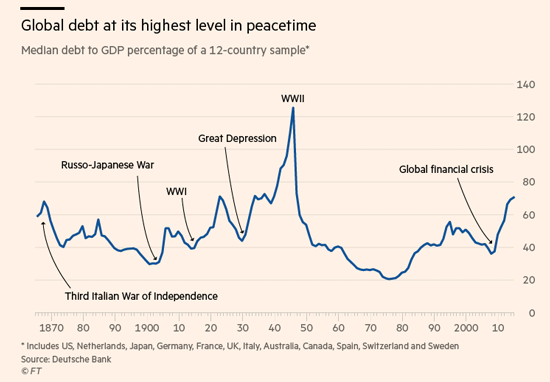

A new Deutsche Bank analysis says the major world economies now have government debt, on average, exceeding 70% of GDP, the highest peacetime level of the past 150 years.

Source: Financial Times

This is obviously unsustainable but the economics profession (and the bankers) desperately want to sustain it. With monetary tools no longer useful, they are turning to fiscal policy. Serious people are mapping strategies like helicopter money, debt monetization, MMT, and worse.

These all, in various ways, essentially say that government debt doesnt matter, and in some cases we actually need more of it. Historically, the only way that can be right is if we are on the cusp of another WW2-like crisis.

This horrifying but well-researched Bloomberg article is chock full of links to insane ideas. Some look superficially attractive, especially to those unfamiliar with even basic economics. Many have familiar, heavyweight names attached to them. All have, to me at least, a whiff of desperation. They are frantic attempts to make the world stop spinning.

I dont think these ideas will work. I think we are beyond the black holes event horizon. Bad things are going to happen, culminating in some kind of globally coordinated debt liquidation I have dubbed the Great Reset. I really see no other way out.

Every day brings more signs of the impending crisis. Duke Universitys latest quarterly CFO survey found more than half of finance chiefs foresee a US recession before the 2020 election. Possibly worse, they project only a 1% increase in capital spending over the next 12 months.

An economy in which near-zero interest rates cant spur more investment than that is an economy with serious problems. And I expect them to get worse, not better.

Furthermore, an increasing body of evidence says that increasing sovereign debt is a slow but inexorable drag on GDP. It is like the frog being boiled in water, but so slowly that we as citizens dont really understand what is happening to us. We do sense something is wrong, though. Hence todays worldwide populist movements.

The driver for 1930s populism was the Great Depression and unemployment. Now the impetus is rising debt and underemployment, with people unable to improve their lives as past generations did. Millions no longer expect to be better off economically than their parents. That frustration is sparking unproductive political partisanship and has the potential to bring political chaos as governments try to protect their own technology and businesses.

The world in general has clearly benefited from globalization and automation, but that is a hard argument to make as jobs disappear. And more jobs will disappear as technology increasingly lets businesses replace expensive humans with cheap robotics and algorithms. Sigh

I wish I had answers. Well, I do, but I dont think theyll going to get a great deal of traction.

This wont be the end of the world. I really do think there are ways that you can properly position your portfolio and your personal life to not just survive but to thrive. We will get through it and be better on the other side. But its going to be a bumpy ride.

One thing that might help you is Jared Dillians Bond Masterclass, which I mentioned last week. I wanted to remind you again before the price goes up. Jared is offering this course at a friends rate to Mauldin Economics readers only. Once its launched publicly, its going to cost twice what it does now.

If you already know bonds inside out (and if you do, kudos to you), then take a look and maybe consider enrolling your kids in the Masterclass. It really is that goodand a heck of a lot cheaper than a university education.

Last week The Washington Post published a wonderful piece about my friend Art Cashin, who is now approaching his 60th year on the floor of the New York Stock Exchange. He is the face of the exchange on CNBC and in many of our hearts. I have spent hours upon hours listening to Arts stories about his life and happenings on the exchange. He is one of the greatest raconteurs of our times.

The physical exchange floor is now just a shadow of what it used to be. I was privileged to be introduced to the floor of the exchange by Art in the early 2000s when it was at its peak. Some of my fondest memories are walking around with Art, watching him settle disputes always with an eye for what was best for the customer. For all intents and purposes, Art was the sheriff of the NYSE.

Those days are gone now as most trades occur elsewhere and the exchanges influence is limited. Now disputes are settled by lawyers and in back rooms, and somehow I think Arts laser focus on what was right for the customer is not front and center in the process. I would like to think Im wrong but

I will be back in New York in mid-October, but for the next three or four weeks I am happily at home in Puerto Rico. I will admit that the initial drive to move here was largely because of the favorable tax treatment. Shane and I now realize that we shouldve moved here sooner because of the lifestyle we have both grown to love. The tax benefits are nice too.

And with that, let me wish you a great week.

Your more calm and optimistic than you might think analyst,

John Mauldin

| John Mauldin

Co-Founder, Mauldin Economics |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.

READ IMPORTANT DISCLOSURES HERE.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

| Digg This Article

-- Published: Monday, 30 September 2019 | E-Mail | Print | Source: GoldSeek.com