-- Published: Sunday, 12 January 2020 | Print | Disqus

The Long Now

Not Worth the Risk

Unproductive and Non-Linear

The Great Reset

New York and the Most Optimistic Man in the Room

If living dangerously is your goal, just keep adding reasonable, manageable, prudent risks. Eventually theyll add up to serious danger.

Hyman Minsky showed how stability leads to instability. Humans have a way of reinterpreting stable periods that seemingly redefines words like reasonable, manageable, and prudent. Thats why we continue chasing yield and risk until we go too far.

To think that we have somehow eliminated recessions and risk, or that central banks and the government have somehow become adept at managing the business cycle, is simply foolish. Yet we keep doing it, every single time.

Debt seems harmless enough at first. You have reliable cash flow, repayment is no problem, and youre going to spend the borrowed money wisely. But human nature tends to make us overdo otherwise good things. And, with debt, you may also have lenders actively urging you to borrow even more. Everything is fine

until its not.

Personal debt, while sometimes excessive, isnt the main problem. Government and corporate debt are the bigger challenge and the reason we will spend the 2020s living dangerously. All that debt is ultimately personal debt, too, since most of us are either taxpayers, shareholders, or both.

In Part 1 of this forecast I described my relatively benign outlook for the next 12 months. The calm may last into 2021 and even beyond. But beneath the surface, pressure will still be increasing. It will grow slowly, almost imperceptibly, but eventually explode.

Or, to use another metaphor: We are frogs in the kettle and someone just turned on the heat. By the time we notice, our good options will be gone.

My friend Ben Hunt at Epsilon Theory has been writing a series called The Long Now. I wont try to summarize because you should read it yourself. Suffice it to say, it is both thought-provoking and disturbing. A quick snippet from his introduction:

The Long Now is everything we pull into the present from our future selves and our children.

The Long Now is the constant stimulus that Management applies to our economy and the constant fear that Management applies to our politics. (Ben has a rather broad view of what he calls capital M Management which includes government, central banks, and others.)

The Long Now is the Fiat World of reality by declaration, where we are TOLD that inflation does not exist, where we are TOLD that wealth inequality and meager productivity and negative savings rates just happen, where we are TOLD we must vote for ridiculous candidates to be a good Republican or a good Democrat, where we are TOLD that we must buy ridiculous securities to be a good investor, where we are TOLD we must borrow ridiculous sums to be a good parent or a good spouse or a good child.

Bens point goes way beyond debt, but thats where he starts. By definition, debt is spending that we pull into the present from our future selves and our children. Or as Ive said often, debt is future consumption brought forward in time.

Debt lets you consume more now, but to repay it you (or someone) must consume less in the future. Used properly, debt can enhance growth enough to cover the eventual repayment. Thats not what is happeningand its a big problem in a consumer-driven economy.

However, Ben Hunt observes that the problems can simmer much longer than we usually think. Humans have an amazing ability to postpone the inevitable andwhen the subject is debta financial incentive to do so. Thats true for both borrowers and lenders.

The Long Now is a good way to describe the extended simmering period. At any given moment, youll be able to say, accurately, the situation is stable (like right now). Since last December we have seen markets go gangbusters. If you were in US stocks, in a buy-and-hold index fund, you made money and lots of it. Even value and dividend players are scooping up big returns. Remember last week and last year I was worrying about corporate bonds? Silly me

A huge amount of money is clearly turning to corporate bonds as it reaches for yield. But then again, why not? The world seems stable. We seem to finally have some progress in the US/China trade wars. The market is telling us everything is okay

much like it did in 2007. Then came 2008.

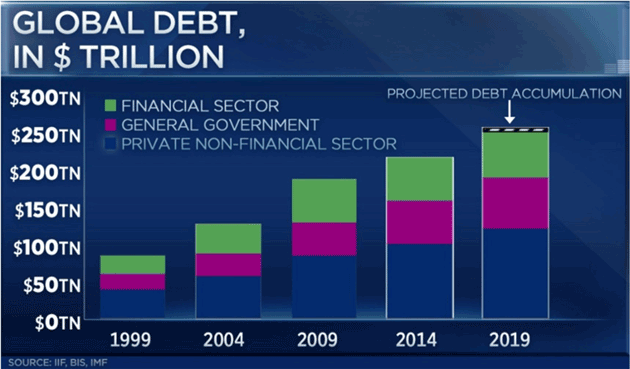

We are using this stability to justify turning up the heat by adding more debt. Theres no reason to think we will stop. The Institute of International Finance, whose Global Debt Monitor tracks the numbers, says worldwide debt climbed $7.5 trillion in the first half of 2019 to hit $250.9 trillion.

Source: CNBC

In November, IIF estimated global debt would surpass $255 trillion by year end. If so, it was a 4.8% increase for the calendar year. Thats faster than GDP growth for either the entire world or most developed countries. Its also faster than population growth in most places.

Lets think about that number for a second. That growth rate, which theres every reason to think will accelerate further, means we can expect $400 trillion in global debt by 2030. Thats not counting the $120 trillion in US government unfunded liabilities. My friend Larry Kotlikoff thinks its closer to $200 trillion and I think it is reasonable to assume Europe is in that ballpark. They too have made pension and healthcare promises that their budgets cant deliver without significant deficits (thus more debt) and in general, their tax systems are already stretched to the max.

While longtime readers know Im against higher taxes, I can do the math here in the US. We are going to have to raise taxes if we want to stay anywhere within shouting distance of fiscal sanity.

That which cant continue, wont. It is simply not possible for per capita debt to keep growing faster than the economy in which the debtors live. There are limits. Recent experience suggests they are more distant than many of us thought, but theyre out there.

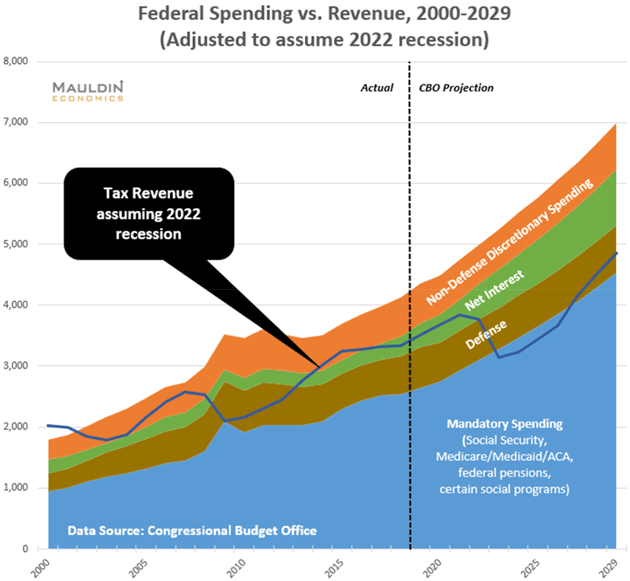

One last thought. When we do have a recession, which again I point out is likely to be after the election (the only meaningful data point between now and the end of next year), the deficit will explode to over $2 trillion per year and, without meaningful reform, never look back. That puts US debt at $35 trillion+ by the end of 2029.

Heres a chart Patrick Watson and I made a few months back, projecting deficits at the end of the next recession. We assume CBO spending projections (which are likely low) and that tax revenue falls by the same percentage it did in the last recession.

We worry about US government debt, and rightly so, but its only the beginning. Corporations have leveraged themselves to the teeth, and much of that debt could easily turn into government debt.

The last financial crisis revolved around mortgages and related derivatives. Millions learned a hard lesson and spent the next decade deleveraging. Yes, people still get in over their heads but its far less common now.

However, that missing mortgage debt has been replaced with additional government debt. The overall debt picture continues to worsen. For the moment, it is sustainable because the economy is growing (albeit slowly, but at least it isnt contracting).

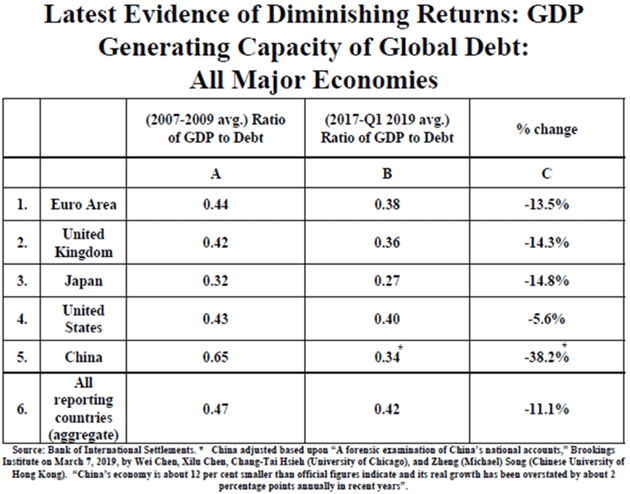

Lacy Hunt of Hoisington Investment Management tracks a number that ought to give us all cold chills. Debt Productivity is the amount of new debt associated with a given amount of GDP growth. Last quarter he found that each dollar of global debt generated only $0.42 of global GDP growth. That was down 11.1% from ten years earlier.

Source: Hoisington Investment Management

Worse, this isnt a linear trend. We can expect it to accelerate as debt grows faster than GDP. At some point, debt becomes completely about consumption and, as noted, bringing consumption forward means less consumption later.

Debt growth isnt linear, either. It has risen almost everywhere even without the negative events (recession, war, etc.) that historically drive it higher. We might be in better shape if corporations had, like homeowners, used the last decade to deleverage. They didnt, in part because central banks made borrowing all but irresistible. Companies borrowed vast sums not because they needed to, but because they could. Often they used it to repurchase their own equity and further leverage their balance sheets.

My friend Peter Boockvar says we no longer have a business cycle, but a credit cycle. Central bank rate cuts encourage us to borrow, which is fun, but they cant cut forever. Then they stop cutting, liquidity dries up, and we panic. Then we get things like the present repo crisis.

This isnt lost on the powers that be. There is actually something of a debate going on in monetary policy circles. Some at the Federal Reserve think we are in a Goldilocks era, with everything being just about right, and thus more rate cuts and QE are fine. Others have serious concerns and more than likely really wish to pound on the podium. But decorum says they cant.

Whatever happens, the visible result is that each recovery phase is smaller than the last. Eventually they will stop being recoveries at all until we rationalize the aggregate debt. Thats economist-speak for default/monetization/restructuring or whatever term you want to use. Until that happens, the word recovery will be meaningless. We cant repay debt without growth. Well have to liquidate it in some fashion.

How do we do that? Inflation is the historically tried-and-true method. Right now central banks are struggling to generate the kind of inflation that would do this. Maybe theyll figure it out, but I think default is the more likely outcome.

However, it wont be the kind of default any of us have ever seen before, or even imagined.

I said all the above to set up my 2020s outlook. In short, I expect we will rock along sideways in this Long Now period. At any given time, well look at the data and think we avoided the worst. We will get some recessions and financial crises, but theyll look manageable after we get through them. Indeed, we will manage them.

What we wont see is sustained expansion of the strength necessary to finance our debt, which will continue growing as The Long Now progresses. So the debt burden will get heavier, and eventually be unbearable. Then the proverbial stuff will hit the fan.

A couple of years ago in my Train Wreck series, I described a multi-step process.

- The Beginning of Woes: Something, possibly high-yield bonds, will set off a liquidity scramble. It will spread through the already-unstable financial system and trigger a broader credit crisis.

- Lending Drought: Rising defaults will force banks to reduce lending, depriving previously stable businesses of working capital. This will reduce earnings and economic growth. The lower growth will turn into negative growth and we will enter recession.

- Political Backlash: Concurrent with the above, employers will be automating jobs as they grow desperate to cut costs. Suffering workerswho are also voterswill force higher safety net spending and government debt will skyrocket. A populist backlash could lead to tax increases that prolong the recession.

I still expect something like that sequence, though it may be more of a drawn-out, rinse-and-repeat process. I think we could see multiple sequences before a final, market-clearing Great Reset, which I expect in the latter half of the 2020s.

After each recession/crisis, and especially as technology begins to eat into middle-class jobs, expect complete political upheaval every four years at a minimum. The politicians will make promises and they will simply not be able to deliver, and a new group will make different promises that dont work, either.

The deepening political divide isnt just left and right. Its also both sides being frustrated with what they consider to be elites. If youre reading this letter, most of the population would probably put you in that category. Yet you probably dont feel elite. I sure dont. I am one of the luckiest and most blessed men in the world, but I certainly dont think, at least from my very humble beginnings, of myself as anything approaching elite. This disconnect is a big part of the problem.

Philippa Dunne recently said in The Liscio Report that we no longer have a shared sense of reality in this country. We observe the same circumstances with our own interpretation of reality, then wonder why other people dont see it the way we do.

I look at these problems every day and I have trouble understanding the complexities. The average person? A man hears what he wants to hear and disregards the rest. We have retreated into our social media and personal echo chambers and made them our reality, completely different than that of other groups/tribes.

In online gaming worlds, players grind through dungeons and zombies to gain points to move on. In my version of The Long Now, we are now entering the grinding phase. We just simply push forward, taking on whatever challenge comes next (whether zombies or central bank policy, which may be the same thing). Meanwhile the debt will keep accumulating, slowing growth but buying yet more grinding time.

Eventually we will reach The Great Reset, and it wont just be another recession or even a depression. It will be a true, world-shaking, generational crisis. My friend Neil Howe talks about the Fourth Turning, a societal calamity that happens every 80 years or so. The last one was World War II. My good friend George Friedman has a forthcoming book titled, The Storm before the Calm. He sees two cycles in the geopolitical world, one 80 years and one 50 years, that converge in the late 2020s. Coincidence? Maybe, but its just about when I think we will have The Great Reset.

We will see political and social upheaval. The capstone: All that debt will be brought to the market, rebalanced, and the market will clear at some new valuation. All asset prices (and every debt is someones asset) will reset.

There will be winners and losers. Because we dont know who will be in political control of any particular place when this happens, it is simply impossible to predict the winners and losers today. Plus technology could change the very nature of international currency markets.

But first we will endure The Long Now. It will look like it can go on forever, and maybe it will. I dont know the future. But my understanding of history, my perceived reality, says it cant continue. There will be a reckoning, after which we will see real growth and prosperity. Good times are coming. At least I think and hope so.

The Great Reset wont hurt everyone equally, or in the same ways. The pain will be unequally distributed. As I said, a lot depends on who controls the process. Politically, populists are gaining power in both left and right wings. Their concerns and priorities differ, but both are anti-elite and both want their favored groups to have more and push the costs on someone else.

That sounds like a formula for violence, and it is, but eventually people tire of fighting and become willing to compromise. Or the market forces them to compromise. That will be The Great Reseta kind of global do-over. No one will get everything they want, but everyone will get a fresh start. Then the cards will fall where they may.

The unknowable part is how much pain we will have to suffer first. It could be a lot

The good news is that the grind of The Long Now will let you prepare for whatever comes. And we have many examples of countries going through their own individual Great Resets. In the case of Argentina and/or Italy, many times. I have visited both countries and they are wonderful places when they are out of crisis.

Thats exactly what I think will happen all over the world after The Great Reset. It will be a wonderful place to be.

You dont have to be all alone in The Great Reset. Personally, I cant think of anything better in any crisis than being part of a tight-knit group of like-minded individuals, whether that is close family or my social and business circles.

Next week, we willfor a very short timereopen the Mauldin Economics Alpha Society to accept 100 new members. There have been some big changes since last year, so make sure to read your invitation when you receive it. As we only have a limited number of seats available this year, we are asking readers who are interested to fill out a membership application. I assure you, though, that it will be more than worth your time.

Im looking for an introduction to two people Andrew Yang and Ambrose Evans-Pritchard. If anyone can help me with this, please send me a note here. Thank you.

At some point in the next few weeks I anticipate going to New York, and several more times this year. I have no other plans to leave Puerto Rico until I finish this 1,200-pound gorilla on my back of a book.

Speaking of Puerto Rico, many friends heard about the recent earthquakes and asked if Shane and I are alright. Short answer, we are. The earthquake was on the other side of the island from us. But the southwest portion got hammered with the 6.4 magnitude earthquake early this week and many aftershocks. Quakes here have (knock on wood) been minor compared to California, but the entire Caribbean is along a slower-moving fault line, which means more small quakes and fewer large ones. Small comfort to those whose homes collapsed this week. And I vividly remember the Haiti quake which took one of my best friends.

Power is slowly coming back up. We have a large diesel generator in our garage that is keeping us going, although we have to be frugal with our electric usage. Internet service is down on much of the island, so I am using mobile phone hotspots. Restaurants and stores are generally open. Maintenance services are available.

All in all, its a minor price for living in paradise. Earthquakes, tornadoes, hurricanes, fires, and all sorts of disasters can strike anywhere. It just reminds you how we are not in control of everything in our lives.

I know that talking about The Long Now and The Great Reset sounds gloom and doom. But in my personal life, I am launching new businesses, making plans, investing in new ventures, and seriously contemplating an aging-focused venture capital fund. I see opportunity everywhere I look. Humanity has faced problems before. Our time will be different, but progress will continue.

I am the most optimistic man in the room, if a tad realistic about our economic landscape. I just want to make sure that I am on the other side of the island when that big future economic earthquake hits, and have backup power. Just saying

Next week we are going to look at why we should be more optimistic than at any time in human history. Seriously. But now its time to hit the send button, so let me wish you a great week and the best for 2020.

Your planning to optimistically grind analyst,

| John Mauldin

Co-Founder, Mauldin Economics |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.

READ IMPORTANT DISCLOSURES HERE.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

| Digg This Article

-- Published: Sunday, 12 January 2020 | E-Mail | Print | Source: GoldSeek.com