-- Published: Monday, 10 February 2020 | Print | Disqus

Viral Threat

Not Good Enough

Overwhelming Stimulus

But What About Government Deficits?

And Then There Is the Fed

Dallas and New York

Economists and investors are rightly obsessed with growth. We always want more of it. We worry it wont come or, worse, might turn into contraction. Economists of all stripes, from Paul Krugman to Lacy Hunt, recognize economic growth cures all manner of ills.

Yet, exactly what is growth? We think we know, but in reality, it is a sticky question. We usually measure it with Gross Domestic Product. But thats a statistic which, like the inflation numbers I questioned last month, is both hypothetical and subjective. Like inflation, there is a great deal of disagreement and discussion among those who specialize in it. We cant be sure the GDP numbers mean what they say. We look at them because we need some kind of benchmark and we dont have a better one. As Dwight Eisenhower said he learned in the Army, Plans are worthless, but planning is everything.

Today I want to look at some aspects of GDP we rarely consider, thinking about how they affect our analysis and choices. But first, lets talk about where GDP is now and where it may go in the near future.

According to the Commerce Departments initial estimate (which will be revised), US real GDP grew at a 2.1% annualized rate last quarter. For calendar 2019, real GDP rose 2.3%, down from the 2.9% it posted in 2018.

So, without even digging into the details, we see growth decelerating but still positive. You can view that as a cup half empty or half full. In either case, its consistent with the slow but persistent recovery from the last recession. I think the base case has to be more of the same, barring surprises. But surprises happen.

As an example, theres Boeing. The largest US exporter has stopped production on the 737 MAX and seems to keep finding more problems to fix. The damage is already trickling through its supply chain. Ive seen estimates that Boeing alone could shave 2030 basis points off GDP growth this year. Treasury Secretary Steven Mnuchin said this week it could be 50 basis points.

Many GDP forecasts presume the latest US-China deal takes trade-related risks off the table. However, that deals text says that if some disaster happens, either side can ask to renegotiate.

Does the Chinese coronavirus rise to that level? Here I have good news and bad news. The good news is that scientists will probably have an effective vaccine within a few months. I talked this week to Joseph Kim, CEO of Inovio, which has been leading research on infectious diseases like Ebola, MERS, and Zika. He said the Chinese are not at all overreacting. It is serious and far too easily transmittable. But within hours of getting the coronavirus DNA on January 10, Inovio already had a potential target vaccine that is now in animal trials. While the US process will go slower, my personal speculation is that China will speed approval if the tests look positive.

That being said, Chinas travel restrictions and business closures will still have a serious and global economic impact. The disease will probably keep spreading until a vaccine is ready, as some reports suggest even asymptomatic patients can infect others. That would mean even those who show no symptoms can still spread the virus. It is not the most deadly virus we have come across, but it does spread.

We must remember that there is a reason we are encouraged to get flu vaccines every year. Five to 20% of the US population gets some kind of flu every year, with about 31 million outpatient visits every year. In 201718 it killed 80,000. Any flu can be serious. One that spreads faster and is more deadly than normal flu? Theres a reason authorities are concerned.

Similarly, the economic virus is already in motion. The many manufacturers around the world who depend on Chinese components may find their pipelines running dry in a few weeks. Then what? Lost sales, layoffs, and it gets worse from there.

We know intuitively that events like these depress growth, at least in the short term. GDP is an attempt to quantify this intuition. But now lets look at how the concept of GDP came about and try to figure out what it actually measures.

The conclusion upfront: GDP (and its government statistical cousins CPI/PCE) are attempts to measure very important data. The conceit is that we can measure it close enough to have numbers two places to the right of the decimal. When was the last time you saw a GDP or CPI number released with the margin of error noted at the same time? I am confident, without having to go back and check, that the margin of error is almost always larger than the numbers to the right of the decimal point. Yet we use these numbers for all sorts of government programs, but perhaps most important, to guide monetary policy.

Back in 2014 I wrote a long letter reviewing Diane Coyles excellent book, GDP: A Brief But Affectionate History. It is still the best book on GDP Ive ever read. She digs into the history that made economists want such a measure and the bureaucratic battles over how to construct it. From the book:

There is no such entity out there as GDP in the real world, waiting to be measured by economists. It is an abstract idea

I also ask whether GDP alone is still a good enough measure of economic performanceand conclude not. It is a measure designed for the twentieth-century economy of physical mass production, not for the modern economy of rapid innovation and intangible, increasingly digital, services. How well the economy is doing is always going to be an important part of everyday politics, and were going to need a better measure of the economy than todays GDP.

You can argue GDP as originally constructed had flaws but was still, as Coyle calls it, a good enough measure of economic performance. At least in my mind, it is clearly not good enough anymore. Like inflations problem with quality (that leads to absurd hedonic adjustments), GDP doesnt capture intangible goods production, or the services that form a large part of todays economy. It was designed for the agricultural and industrial economy its Depression-era designers knew.

The result is a measure that doesnt reflect much of the production we think it does. From my review:

GDP is a huge undertaking, full of rules, with almost as many exceptions to the rules, changes, fixes, and qualifications, so that, as one Amazon reviewer noted, GDP is in reality so complex there are only a handful of people in the world who fully understand it, and that does not include the commentators and politicians who pontificate about it almost daily. The quarterly release of GDP statistics is more akin to a religious service than anything resembling a scientific study. The awe and breathlessness with which the number is discussed is somewhat amusing to those who understand the sausage-making process that goes into producing the number. Whether the GDP reading is positive or negative, it often changes less in a given quarter than the margin of error in the figure itself, and it can be and generally is revised significantlyoften many years later when almost no one is paying attention. Whens the last time the mainstream media reported a five-year-old revision?

If you pay someone to mow your lawn and report wages paid, that adds to GDP. If you pay that person under the table, it doesnt. If you pay your maid to clean your house, it adds to GDP. Except if you marry her, then it doesnt. Unless of course she gets access to the credit card, in which case spending probably increases GDP dramatically. In England, sex with your wife does not add to GDP, but sex with a prostitute doeseven if it is unreported. Go figure. There are so many jokes and one-liners that I could add to this litany, but Im going to resist. Okay, just one. Can you imagine the reception if you came home with a blonde hair on your dark suit and your excuse was, Honey, I was just doing my bit for the national economy. We all have to make sacrifices.

Housekeeping, cleaning, cooking, and other such duties do not get counted in GDP, although without them GDP would suffer significantly. Perhaps that is because when the original discussions about what constituted GDP were underway, womans work was significantly undervalued.

All that is still true, but we have a new development in the almost six years since I wrote the above.

One of GDPs big problems is the way it treats government spending. This was controversial when Simon Kuznets and others designed it back in the 1930s. Kuznets (who would later get a Nobel Prize for his foundational work on GDP) himself wanted to exclude defense spending. Other influential economists wanted to exclude government spending altogether, based on the fact that government spending came from taxes which should already be included in GDP, so adding government spending back into GDP is double counting.

Supposedly when Franklin Roosevelt saw the difference, like any politician, he chose the larger number that made his administration looked better. He wanted to avoid a scenario where the economy looked like it was shrinking even as they expanded government spending. So now we classify government spending as production. (Note thats not a personal criticism of Roosevelt. I think any Republican president would have made the same decision.)

We are still basically using that same methodology in a radically different world. Manufacturing is now under 12% of GDP. Government spending (local, state, and national) is about 40% of GDP as we measure it today, but it consumes almost 2/3 of private production.

But we still use the same basic methodology for measuring GDP. Kuznets himself said that, The welfare of a nation can scarcely be inferred from a measurement of national income as defined by the GDP

Goals for more growth should specify of what and for what. It is critical to note that, as Jeremy Rifkin said:

The problem with the [GDP] index is that it counts negative as well as positive economic activity. If a country invests large sums of money in armaments, builds prisons, expands police security, and has to clean up polluted environments and the like, its included in the GDP.

If a company pollutes the environment then sells a product, that is seen as a positive contribution to GDP. So is cleaning up the mess. Just saying

A different problem emerges when government runs a deficit. That money theoretically comes from future tax revenue, assuming that the bonds the government sells to cover that debt will be paid back.

Deficits are no longer if or when, of course. They have become a fact of life and the only question is whether they are huge or gargantuan. This creates multiple problems, among which is GDP distortion. It overweights government spending and underweights private production.

This is a problem because GDP is key to the Keynesian macroeconomic theory on which most governments rely. If GDP is lagging, the answer is to dial up government spending, which is a direct input to GDP. Presto, growth appears.

The original idea, at least according to Keynes, was for government to run deficits during recessionary periods, thereby creating demand that would boost GDP back into growth again. Thenand this is the part we now ignorerun surpluses during the boom times in order to be ready for the next downturn. Keynes didnt envision the permanent deficits we now have.

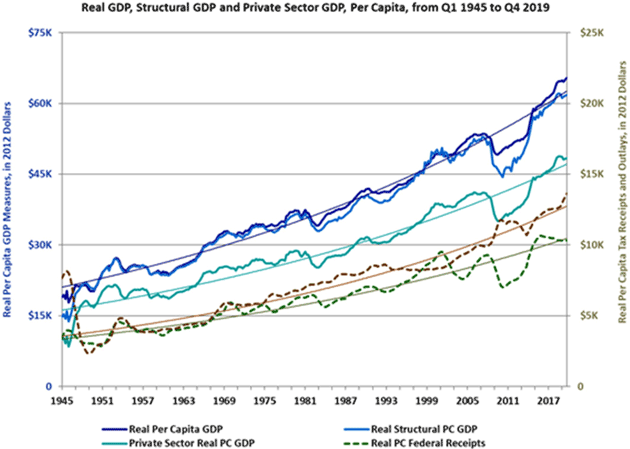

I recently had a fascinating email exchange with Rob Arnott on the implications of all this. He produced this chart for me. What Rob calls Structural PCGDP is GDP less government deficit spending (or plus surplus). Private Sector GDP is simply GDP less federal, state, and local government outlays.

Source: Research Affiliates

Rob also made a series of scatterplots, which I wont reproduce, that show government surplus or deficit seems unrelated to GDP growth. But if you look only at private sector GDP, outlays soar when it is cratering. From this he makes an interesting conclusion.

The subsequent impact of deficit spending and of increased Government outlays is what Keynes predicted, but ironically not at all what neo-Keynesians would predict. Subsequent one- and two-year growth in Private Sector GDP is modestly better when the government is running deficits, as Keynes would have predicted, but rising outlays do material damage to Private Sector GDP.

So, when the deficit is because tax receipts are tumbling, the subsequent rebound is good, but when its because spending is soaring, subsequent private sector growth is lousy. This latter impact isnt noticed because the economics profession is content to see GDP growth due to growth in G,[G is the abbreviation for government spending in the equation] every bit as much as from any other source. Never mind that we cant *spend* (or invest) the G part of GDP.

Why cant we spend it? Because government spending is funded by either taxes or borrowing. Either is removed from the resources that the citizenry (including government employees) can spend. The citizenry can only spend money that the government is also spending, if the borrowing is from external sources, but that has its own consequences.

The current surge in outlays is not an auspicious data point for future private sector GDP growth. Nor is it going to turn around any time soon, given that Trump and the Dems are all committed to massive increases in spending, mainly fighting over who controls the purse strings and where theyll be spending the money.

In other words, we appear to be reaching the point at which government spending overwhelms any Keynesian stimulus benefit, in part because we failed to run surpluses that would have helped cover this spending. We instead expanded the debt, raising interest costs on top of the growing entitlement and defense spending.

Worst of all, there is no painless way out of this trap. I see approximately zero chance government spending will fall, no matter how this years elections turn out. Whether through deficits or borrowing, government is going to suck more and more of private GDP into the Treasury, from which it will be redistributed to favored groups. What we now call politics is really a battle to be one of those groups.

The on-budget deficit is already over $1 trillion. Combined with the off-budget spending, the national debt will probably grow $1.3 trillion or more this year. A recession would likely increase the deficit by another $1 trillion.

This isnt entirely GDPs fault, but GDPs design encourages it. Whether GDP rises or falls is important, but not as important as the policies it is used to justify.

The Federal Reserve is now having to inject $60 billion a month to provide repo liquidity and other activity. Why? The Fed is essentially using its current QE program (although they dont want to call it QE) to monetize over two-thirds of the deficit.

Furthermore, there is increasing talk about controlling the yield curveanother form of easingto help GDP growth. Does it need such a boost? We cant really know because GDP doesnt tell us what we think it does.

You can Google economic papers on GDP including new sources of growth and read a library of papers by famous names concluding GDP no longer effectively measures growth in the US. Theres just so much that we are not counting in a service and digital economy.

Yet the Fed sets monetary policy as if those things did not exist. They fix the most important price in the world, short-term interest rates, based on flawed understanding of inadequate data. And the longer we continue to operate in that manner, the more difficult it will be to extricate ourselves from the problems we are creating.

That sounds like an idea for another letter, and a good place to close this one.

Shane and I are in Dallas this morning and I will be in New York in about two weeks, days to be determined. We fly back to Puerto Rico tomorrow afternoon.

This afternoon will be the weekly planning call for the Strategic Investment Conference. We just had Sam Zell confirm he is coming, along with Leon Cooperman. We are having conversations with other well-known names but already this is clearly going to be the best SIC ever. You will soon get your invitation, if you havent already. We are reducing the numbers of seats 40% this year, at the request of long-time attendees. We expect to sell out quickly. Put May 1114 in Scottsdale, Arizona at The Phoenician in your calendar and be there.

The business meetings in Dallas have gone better than I could possibly hope for. In the not-too-distant future, I should be able to provide more services and opportunities to my readers and clients. Technology has completely reshuffled the deck of what we can do for the average client. I wish we couldve done this 20 years ago, but even one year ago the technology to band them together did not exist. I know that I am writing a book on how fast things are changing, but I am living it in my own life and business, and it amazes me.

And with that I will hit the send button. You have a great week!

Your making 1020-year plans at 70 analyst,

| John Mauldin

Co-Founder, Mauldin Economics |

P.S. Want even more great analysis from my worldwide network? With Over My Shoulder you'll see some of the exclusive economic research that goes into my letters. Click here to learn more.

READ IMPORTANT DISCLOSURES HERE.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

| Digg This Article

-- Published: Monday, 10 February 2020 | E-Mail | Print | Source: GoldSeek.com